BCHG Stock: Grayscale Bitcoin Cash Trust to ETF?

Here is the strange thing about BCHG stock. As of June 2, 2026, one share traded around $2.01, while the Bitcoin Cash sitting behind that share was worth about $2.29. You were buying roughly a dollar of BCH for about 88 cents. That sounds like free money. It isn't, and the reason it isn't tells you almost everything you need to know about the Grayscale Bitcoin Cash Trust. The gap between what BCHG holds and what BCHG sells for is not a bargain waiting to be collected. It is the predictable output of how this thing is built, and a 2.50% annual fee quietly eats away at it the whole time you wait.

What BCHG Stock Actually Represents

BCHG stock is not a company share. The trust has no product, no revenue, no management team building anything. The only thing it owns is Bitcoin Cash. Grayscale Investments, a digital assets manager, launched it on March 1, 2018, as a private placement, and it later began trading over the counter under the ticker BCHG. When you buy a share, you are buying a claim on a fixed pile of BCH held in cold storage, minus the fees. Nothing else.

One share, one sliver of Bitcoin Cash

The trust holds 384,991.96 BCH against 47,123,300 shares outstanding, according to its SEC Form 10-Q dated March 31, 2026. Do the division and each share represents about 0.00817 BCH. That is the whole investment. As BCH rises or falls, the value of the share's underlying asset rises or falls with it. Net assets came to roughly $181 million at the end of that quarter.

| BCHG fund fact | Value (as of Mar 31, 2026) |

|---|---|

| Ticker / market | BCHG / OTCQX |

| Inception | March 1, 2018 |

| Sponsor | Grayscale Investments |

| BCH held | 384,991.96 BCH |

| BCH per share | ~0.00817 |

| Shares outstanding | 47,123,300 |

| Net assets | ~$181 million |

| Sponsor fee | 2.50% per year |

Why it lives on OTCQX, not a real exchange

BCHG trades on the OTCQX marketplace run by OTC Markets Group, not on Nasdaq or the NYSE. That distinction matters. The trust was created through private placements to accredited investors, and those shares only reached the public market after a holding period. There is no everyday mechanism for ordinary buyers to create new shares or redeem old ones for the BCH inside. The security trades, but the door between the share and the coin is — for retail purposes — bolted shut. Hold that thought, because it explains the discount.

The 2.50% fee that compounds against you

You will see the fee quoted as 1.5% in some database listings. That figure is wrong. The trust's own filings put the sponsor fee at 2.50% of net assets per year, paid monthly in BCH. Read that again: the fee is paid by selling off a little of the trust's Bitcoin Cash every month. So the BCH backing each share slowly shrinks, regardless of what the market does. Over a year that is a real bite. Over five, it compounds into a meaningful chunk of your exposure, gone to expenses before the price ever moves.

Put a number on it. Start with that 0.00817 BCH per share. At 2.50% a year, after five years of flat BCH prices you would be left with roughly 0.0072 BCH per share, a bit over 12% of your coin exposure quietly drained into the sponsor fee. The price of Bitcoin Cash never had to drop for you to lose that. Most index and exchange-traded products in the crypto space now charge a fraction of this; a 2.50% expense ratio is high even by the loose standards of single-asset trusts, and it is the clearest cost of choosing the wrapper over the coin.

Why BCHG Stock Trades Below the BCH It Holds

A closed-end wrapper with no redemption valve does not track its underlying asset cleanly. It drifts. Sometimes it drifts above, sometimes well below, and BCHG has spent most of its recent life below.

NAV vs market price, in plain English

Net asset value, or NAV, is simply the value of the BCH the trust holds, divided by the shares outstanding. It is what each share is "really" worth based on the underlying index price of Bitcoin Cash. The market price is whatever buyers and sellers agree on that day in the open quote. When the two diverge, you get a premium (price above NAV) or a discount (price below NAV). As of early June 2026, BCHG sat at roughly a 12% discount. It has swung hard before, from a premium north of 40% in early 2025 to discounts in the low-to-mid twenties since.

No redemption means no arbitrage

In a healthy fund, big players close gaps like this for profit. If shares trade below the assets, an authorized participant buys cheap shares, redeems them for the underlying, and pockets the difference until the gap closes. That constant pressure is what keeps an ordinary exchange-traded fund glued to the value of what it owns. BCHG has no such mechanism open to the market. There is no redemption window for retail, so there is no arbitrage, and without arbitrage there is nothing pulling the price back toward NAV.

So the discount can sit there for months, even years, punishing anyone who assumed it would snap shut on its own. Worse, the direction is not stable. The same wrapper that trades at a discount today traded at a steep premium in early 2025, when demand outran the available shares. A buyer who paid that premium effectively overpaid for BCH and then watched the premium flip to a discount. The "buy a dollar for 88 cents" trade only pays off if something structural changes, and you cannot know in advance when, or whether, it will.

The GBTC precedent

We have seen what that structural change looks like. Grayscale's flagship Bitcoin product, GBTC, once traded at a discount near 49% in December 2022. Investors who bought the discount waited in pain. What finally closed it was a conversion. GBTC became a spot Bitcoin ETF, and the discount collapsed to roughly zero on January 11, 2024, according to CoinDesk. That is the template every BCHG discount-buyer is implicitly betting on.

Volatile BCHG Stock Price and 2026 Performance

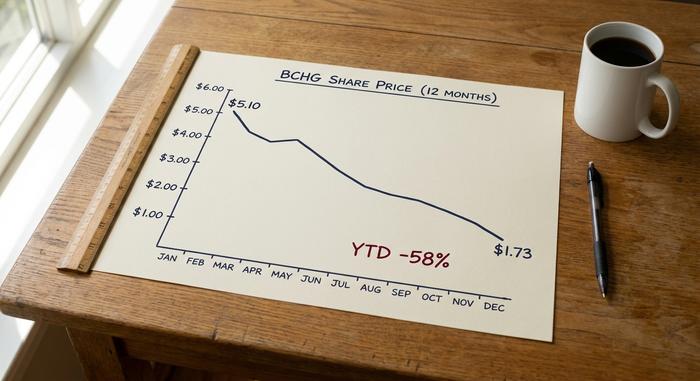

Look at the numbers before you read any marketing. BCHG has been a brutal holding. Its 52-week range runs from $1.73 to $5.10, and the stock is down roughly 58% year to date in 2026. The share price is volatile because the thing underneath it is volatile, and then the discount adds a second layer of pain on top.

The underlying asset is not helping. Bitcoin Cash traded around $243 with a market cap near $4.88 billion as of June 4, 2026, ranking around 23rd among cryptocurrencies, per CoinGecko. BCH had fallen close to 47% over the prior 30 days and sat more than 90% below its 2017 peak. Trading is thin, too: about 531,000 shares changed hands on June 3, worth under a million dollars. Thin volume means the quote you see and the price you actually get can be two different things.

Stack those layers and the math gets unforgiving. Bitcoin Cash itself is a high-beta asset whose volatility runs far above the broad crypto market. On top of that swing, BCHG adds a moving discount that can widen exactly when you want to sell, plus a fee that never stops. A holder who bought near the top of the 52-week range has watched all three forces pull in the same direction at once. That is why the year-to-date drop on the stock is steeper than the drop in BCH over the same stretch: the wrapper amplifies the bad days instead of cushioning them.

| Metric (early June 2026) | BCHG |

|---|---|

| Share price | ~$2.01 |

| NAV per share | ~$2.29 |

| Discount to NAV | ~−12% |

| 52-week range | $1.73 – $5.10 |

| Year-to-date return | ~−58% |

| Underlying BCH price | ~$243 |

How to Buy (or Avoid) BCHG Shares

Buying BCHG stock is mechanically simple, and that ease is part of the trap. The shares sit in any standard brokerage account, so you can add them next to your regular stocks without opening a crypto exchange account or touching a wallet. For an investor who wants Bitcoin Cash exposure inside a retirement or brokerage account, that convenience is the entire appeal.

But thin liquidity changes how you should trade it. With volume this low, the gap between the bid and the ask can be wide, and a market order can fill at a worse price than the last quote you saw. Use limit orders. Check the spread before you commit. There is no dividend here and no yield; the only return comes from price movement and, if you are lucky, a narrowing discount.

The one place the wrapper earns its keep is the tax-advantaged account. You generally cannot hold raw Bitcoin Cash inside a standard IRA or many employer plans, but you can usually hold a security like BCHG there. For an investor who wants BCH exposure specifically inside that kind of account, the trust may be the only practical route, and the fee becomes the price of admission. Outside such accounts, the case thins out fast. Treat the convenience as what it is, a wrapper you pay for, not a free upgrade over owning the coin.

BCHG vs Holding BCH vs a Future Spot ETF

There are three ways to get Bitcoin Cash exposure, and for most retail investors BCHG stock is the worst of them, with one important exception.

| Feature | BCHG | Direct BCH | Spot BCH ETF (if approved) |

|---|---|---|---|

| Annual fee | 2.50% | None | Likely lower |

| Trades below NAV? | Yes, often | N/A | No, closes to NAV |

| Redemption mechanism | None for retail | You hold the coin | Yes |

| Custody | Grayscale holds it | You self-custody | Fund custodian |

| Brokerage access | Yes | No | Yes |

The ETF conversion case

The one thing that would flip BCHG from trap to opportunity is conversion into a spot exchange-traded fund. Grayscale filed a Form S-3 on September 9, 2025, to convert the trust into a spot ETF listed on NYSE Arca, as reported by The Block. The Bitcoin Cash filing came alongside similar moves for other single-asset trusts, part of a broader Grayscale push to convert its closed wrappers into ETFs the way GBTC did. Conversion would open the redemption door, which is exactly what closes a discount, and it would likely come with a lower fee.

The catch is that approval depends on the SEC adopting generic listing standards for crypto products, a framework that would let exchanges list these funds without a bespoke rule change for each one. As of June 2026 those standards were not finalized, so there is no approval and no firm timeline. You are betting on a regulatory outcome, not a sure thing, and a delay can stretch from quarters into years while the fee keeps running.

Why owning BCH directly often wins

If all you want is Bitcoin Cash exposure, buying BCH on an exchange skips the 2.50% drag, skips the discount risk, and lets you actually move or spend the coin. The tradeoff is self-custody: you manage the keys, the security, and the tax record yourself. For a buy-and-hold investor comfortable with a wallet, direct ownership is usually cleaner. BCHG earns its place only when a brokerage wrapper is genuinely required, or when you specifically want to bet on the discount closing.

Is BCHG Stock a Good Investment? The Verdict

Here is my honest read. BCHG is not one bet, it is two stacked on top of each other. You are betting that Bitcoin Cash recovers, and separately that the discount closes through an ETF conversion that has been filed but not approved. If you only believe the first, buy BCH directly and stop paying 2.50% a year for the privilege of a worse price. If you are playing the second, the discount-closing trade, size it like the speculative position it is, not like a core holding. The question worth asking before you click buy is simple: are you here for Bitcoin Cash, or for the wrapper? Because with BCHG stock you are paying for the wrapper either way.