What are crypto loans and how do they work?

Crypto lending hit $73.6 billion in outstanding loans in Q3 2025, blowing past the previous record set during the 2021 bull run. That number comes from Galaxy Research, and it tells you something: despite Celsius going bankrupt, despite BlockFi collapsing, despite 4.3 million investors losing $46 billion in the 2022 meltdown, people keep borrowing against their crypto. The market not only survived. It grew back bigger.

The idea is dead simple. You own BTC. You need dollars. Instead of selling your BTC and paying capital gains tax on the profit, you hand it to a lender as collateral. They give you cash. You pay interest. When you pay back the loan, you get your BTC back. If you bail or the price tanks too hard, the lender takes your crypto. That is the deal.

This piece goes through how crypto loans actually work, CeFi versus DeFi lending, what you will pay in 2026, which platforms are still standing, and what we should all remember about the ones that are not.

How does a crypto-backed loan work?

You put crypto into a lending platform. The platform hands you a loan, usually stablecoins or actual dollars. You pay interest. When you pay it all back, your crypto comes home. Miss payments or let the value drop too far? They sell your coins.

The number that controls everything is the loan-to-value ratio. LTV. If a platform offers 50% LTV and you deposit $10,000 in BTC, you can borrow $5,000. The other $5,000 is the lender's cushion. If BTC drops and that cushion shrinks, you get a margin call. Keep dropping and the lender dumps your collateral to cover the debt.

Nobody asks for your credit score. Nobody wants to see your pay stubs. Nobody cares if you have a bank account. The crypto IS the collateral. That is it. A farmer in Kenya with 0.5 BTC has the same borrowing power as a Wall Street trader with 0.5 BTC. The math does not discriminate.

Traditional loans take weeks and reject half the applicants. Crypto backed loans take minutes and only ask one question: do you have the coins?

Here is what happens step by step:

1. You pick a lending platform (CeFi or DeFi)

2. You deposit crypto as collateral (BTC, ETH, or other accepted tokens)

3. The platform calculates your borrowing power based on the LTV ratio

4. You receive your loan in stablecoins, USD, or another currency

5. You pay interest on the loan amount (monthly, or it accrues)

6. When you repay the loan in full, your collateral unlocks

7. If your collateral value drops below the liquidation threshold, the platform sells it

CeFi vs DeFi lending: two different worlds

Two paths here. CeFi and DeFi. They solve the same problem in completely different ways.

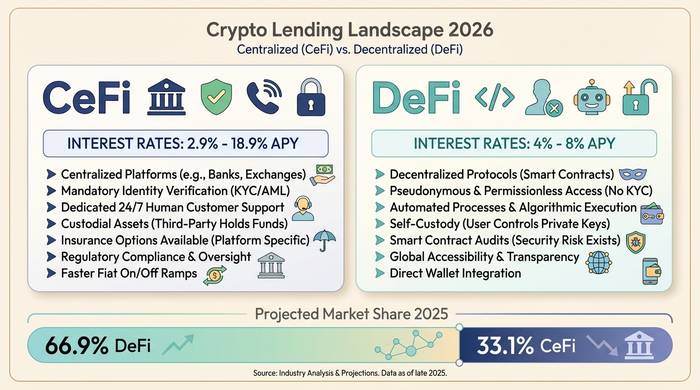

CeFi is a company that lends you money. Nexo, Ledn, Arch Lending, Coinbase. You sign up. You do KYC. You hand over your BTC. They give you dollars or stablecoins. It feels like a banking app. If your account gets weird, you email support. Rates go from 2.9% APR if you are a Nexo power user staking their token, all the way up to 18.9% for a regular account with no perks. Most people borrowing against BTC end up paying 9-12%.

DeFi is nobody. No company. No account. No KYC. Smart contracts on Ethereum or Arbitrum hold your collateral and manage the math. You connect a wallet, deposit tokens, and borrow from a pool that other users funded. Aave runs the show here. Over $1 trillion in cumulative loans. $27-40 billion sitting in the protocol right now. Compound and Morpho are the other big names. Stablecoin borrowing rates on DeFi hover around 4-8% APR. Cheaper than CeFi, but you are your own customer support.

| Feature | CeFi lending | DeFi lending |

|---|---|---|

| How it works | Company manages loans | Smart contracts, no middleman |

| KYC required | Yes | No |

| Interest rates (stablecoin borrowing) | 2.9-18.9% APR | 4-8% APR |

| Collateral custody | Platform holds it | Smart contract holds it |

| Liquidation | Margin call then liquidation | Automatic smart contract liquidation |

| Risk | Platform bankruptcy, mismanagement | Smart contract bugs, oracle failures |

| Example platforms | Nexo, Ledn, Coinbase, Arch | Aave, Compound, Morpho, Spark |

| Customer support | Yes | No (community forums only) |

| Accessible in US | Some platforms (Nexo returned April 2025) | Usually yes (permissionless) |

What the rates look like in 2026

Interest rates depend on four things: which platform you use, what you pledge as collateral, what LTV you pick, and whether you hold the platform's native token.

| Category | Rate range | Notes |

|---|---|---|

| CeFi, BTC collateral (regulated) | 9-12% APR | Ledn 10.4-12.4%, Arch from 9.5% |

| CeFi with loyalty perks | 2.9-6% APR | Nexo Platinum tier requires NEXO token staking |

| CeFi base rate (no perks) | 14-18.9% APR | Plus possible origination fees |

| DeFi variable (stablecoins) | 4-8% APR | Aave, Compound, Morpho |

| Binance (non-US) | ~1%+ | Cheapest option, geo-restricted |

BTC gets the best rates because lenders consider it the safest collateral. ETH comes next. Altcoins cost more to borrow against because they are more volatile and harder to liquidate quickly. Some platforms only accept BTC. Ledn dropped ETH entirely in 2025 and went BTC-only.

LTV works inversely with safety. A 25% LTV loan means your collateral can drop 75% before liquidation. A 90% LTV loan means a 10% drop wipes you out. Most people borrow at 40-60% LTV as a balance between access to liquidity and breathing room.

| LTV tier | Your buffer | Risk level | Who offers it |

|---|---|---|---|

| 25-40% | Collateral can drop 60-75% | Low | Kraken, conservative DeFi |

| 50% | Collateral can drop 50% | Medium | Ledn, Crypto.com |

| 60-70% | Collateral can drop 30-40% | Medium-high | Nexo, Salt Lending |

| 80-90% | Collateral can drop 10-20% | High | YouHodler, Aave e-Mode |

Why people take crypto loans instead of selling

Taxes. That is reason number one and it is not close. Say you bought BTC at $10,000. It is now $60,000. Sell it and you owe capital gains tax on $50,000 of profit. Borrow against it instead? No sale happened. No taxable events. You get the cash, you keep the BTC, and you pay interest instead of handing money to the government.

Reason two: you think prices are going up. Selling ETH today to pay rent means you miss the run. A crypto-backed loan lets you unlock liquidity right now and stay long.

Reason three: banks are slow and selective. Try getting a personal loan approved in a week with no credit history. Good luck. DeFi lending platforms do it in five minutes. No bank account needed. No one asking what the money is for.

Then there is leverage. Some people deposit ETH, borrow USDC, buy more ETH, deposit that too, borrow more. Round and round. In a bull market, it is a money printer. In a crash, it is a meat grinder. Aave liquidated $237 million in collateral in a single day during a 2025 sell-off. Leverage does not pick sides.

What went wrong: Celsius, BlockFi, and the 2022 crash

You want the cautionary tale? Here it is.

In 2022, three major CeFi lenders went bankrupt in the span of six months. 4.3 million people lost $46 billion combined. According to the Fed, large accounts (over $500K) pulled their money first. Regular depositors got stuck.

Celsius was the worst. "Earn up to 18% on your crypto." That was the pitch. What they actually did: took customer deposits and lent them to hedge funds with garbage collateral. Three Arrows Capital blew up, left a hole Celsius could not fill, and the whole thing collapsed in July 2022. Depositors eventually got back about 65 cents on the dollar across three painful rounds of payouts totaling $2.75 billion.

BlockFi died in November 2022 because it had too much money tied up with FTX and Alameda. Creditors actually got lucky. BlockFi's claims against FTX paid out well enough that people recovered roughly 100% in fiat terms.

Voyager went down the same summer. $650 million lent to Three Arrows. Gone. Creditors got back about 70%.

| Company | Bankruptcy | Root cause | Creditor recovery |

|---|---|---|---|

| Celsius | July 2022 | Illiquid investments, 3AC exposure | ~65% ($2.75B across 3 payouts) |

| BlockFi | November 2022 | FTX/Alameda exposure | ~100% (fiat terms, at bankruptcy prices) |

| Voyager | July 2022 | 3AC exposure ($650M) | ~70% (two rounds) |

| Genesis | January 2023 | 3AC + FTX contagion | Partial (settled with NY AG) |

Same story every time. Company takes deposits. Promises big yields. Lends the money out without enough collateral backing it. When one domino falls, the whole chain goes with it.

So are crypto loans dead? Obviously not. $73.6 billion says they are fine. But the lesson is burned into the industry now: if a company holds your crypto and you cannot see exactly what they are doing with it, you are trusting them not to be the next Celsius. DeFi protocols have their own risks, bugs and oracle failures mostly, but at least you can read the smart contract and see where your collateral sits at all times.

How to pick a lending platform

CeFi: proof of reserves or walk away. Any platform that does not publish regular attestations in 2026 has learned nothing from 2022. Look at the real rate at your LTV, not the marketing rate. Check the jurisdiction. Nexo came back to the US in April 2025. Ledn runs through CIMA in the Cayman Islands and publishes reserves. If someone is promising 18% returns on your deposits, remember the last time you heard that.

DeFi: audit history first. Aave and Compound have years of battle testing behind them. Newer protocols might offer better rates but carry more unknown risk. Pay attention to the oracle. One glitchy price feed can liquidate your position for no reason. It happened on Aave in March 2026: $27 million wiped out by a pricing error, not a market crash.

For either: do not borrow what you cannot repay if BTC drops 50% tomorrow. Keep your LTV at 50% or below. Set up price alerts. And have dry powder ready to top up collateral when things go sideways.