Spot Ethereum ETF: 2-Year Retrospective and Staking Era

For about ten months after the SEC approved them, US spot Ethereum ETFs looked like the small sibling of the Bitcoin ETFs that launched six months earlier. Inflows came in slower. Total assets stayed under $13 billion. Grayscale's legacy ETHE trust bled outflows in a near-perfect repeat of the GBTC pattern from 2024. Then 2025 happened. The SEC rescinded SAB 121, the GENIUS Act passed, ETH reached a new all-time high above $4,900, and the staking question got answered: first Grayscale, then BlackRock launched ETH ETFs that pass staking rewards through to shareholders. This guide explains what a spot Ethereum ETF is, who the issuers are, what the two-year flow data actually shows, and how the staking unlock reshaped the product class.

What is a spot Ethereum ETF in plain terms?

A spot Ethereum ETF is an exchange-traded fund, structured as a regulated investment trust, that holds actual Ether and lists tradeable shares on a US stock exchange. Each share represents a small fractional claim on the trust's ETH holdings. The price tracks the ETH spot price minus fees, kept in line through a creation-and-redemption mechanism handled by authorized participants. This is the structural difference from earlier futures-based Ether ETFs like the ProShares Ether Strategy ETF (EETH, launched October 2023): a spot ETH ETF holds the underlying cryptocurrency on the Ethereum blockchain; a futures product holds CME contracts that approximate it.

Investors buy and sell ETH exposure through their brokerage account. Shares are registered under the Securities Act of 1933, and the trust falls under SEC security oversight via the exchange-listing rules — a meaningful contrast to holding ETH directly through a self-custody wallet.

How spot Ethereum ETFs work in practice

The basic mechanics are the same as any commodity-backed ETF. The issuer's chosen custodian holds the ETH; in practice, seven of the nine US issuers use Coinbase Custody. The issuer publishes a daily net asset value based on the value of those ETH holdings. Authorized participants — large broker-dealers — can create new ETF shares by delivering cash equal to a basket's NAV, or redeem shares for cash, on a daily basis. Arbitrage pressure keeps the share price tight to NAV.

At launch in July 2024, the SEC required cash creation rather than in-kind exchange, which the BTC ETF approvals had pioneered. That added a small step: the issuer takes the cash and buys ETH on the open market, rather than receiving ETH directly from the AP. The mechanism still works smoothly enough that share prices typically trade within a basis point or two of NAV during US market hours. Expense ratios are deducted from trust assets daily, which is why a 0.25% management fee shows up as a slow drag on share price relative to ETH spot, not as a separate charge to the investor.

The 9 spot Ethereum ETFs and their fees

Nine spot Ethereum ETFs began trading on July 23, 2024. The fee war that broke out before launch followed the BTC ETF playbook almost exactly: every new issuer offered a temporary fee waiver, and Grayscale's legacy trust got priced out by its own sibling.

The cheapest US product is the Grayscale Ethereum Mini Trust (ticker ETH) at 0.15%, designed to keep assets inside the Grayscale family that would otherwise flow out of the legacy 2.5% ETHE trust. Franklin's EZET sits just above at 0.19%. VanEck (ETHV), Bitwise (ETHW), and 21Shares (CETH, ticker later changed to TETH) cluster around 0.20–0.21%. BlackRock's ETHA, Fidelity's FETH, and Invesco-Galaxy's QETH share 0.25% as their headline rate. ETHA's twist is a 0.12% promotional fee waived for the first $2.5 billion in AUM or one year, whichever came first.

Then there is ETHE, the legacy Grayscale trust converted to ETF form. Its 2.5% fee has been the single largest source of structural outflows in the category — a near-identical replay of GBTC's role in the BTC ETF launch.

| Ticker | Issuer | Fee |

|---|---|---|

| ETH | Grayscale Ethereum Mini Trust | 0.15% |

| EZET | Franklin Ethereum Trust | 0.19% |

| ETHV | VanEck Ethereum Trust | 0.20% |

| ETHW | Bitwise Ethereum ETF | 0.20% |

| CETH/TETH | 21Shares Core Ethereum ETF | 0.21% |

| ETHA | iShares (BlackRock) Ethereum Trust | 0.25% |

| FETH | Fidelity Ethereum Fund | 0.25% |

| QETH | Invesco Galaxy Ethereum ETF | 0.25% |

| ETHE | Grayscale Ethereum Trust (legacy) | 2.50% |

2024–2026 retrospective: flows, AUM, and the Grayscale tax

The two-year arc reads cleanly with hindsight. Day-1 net inflows across all nine ETFs were $106.78 million on July 23, 2024, against $1.077 billion in trading volume — roughly 20% of what the spot Bitcoin ETFs printed on their own first day six months earlier. The newcomers ran a strong first day on the gross numbers: ETHA brought in $266.5 million and ETHW $204 million. The net figure came in light because ETHE bled almost half a billion dollars in outflows that same session, the start of a year-long migration into cheaper sister funds.

Year one closed with about $2.6 billion in cumulative net inflows and AUM near $12 billion — far behind the BTC ETF trajectory at the same point. Then 2025 went vertical. Farside Investors recorded $9.6863 billion in net inflows across the year, with August 2025 alone accounting for roughly $3.87 billion. ETH set a new all-time high of $4,953.73 on August 24, 2025, and that month became the only one in which spot Ether ETF flows actually exceeded spot Bitcoin ETF flows ($3.87 billion ETH vs −$750 million BTC). BlackRock's ETHA peaked above $13 billion in AUM in November 2025 and ran roughly 50% of the US ETH ETF market through March 2026.

Then came the hangover. Five consecutive months of net outflows from November 2025 through March 2026 pulled cumulative inflows back near $11.7 billion before April 2026 broke the streak with about $356 million in fresh inflows. As of May 2026, CoinGlass shows roughly $12.08 billion in cumulative net inflows and combined NAV near $13.6 billion across the nine US spot products. Grayscale's ETHE has accounted for approximately $4.8 billion of cumulative outflows since converting in July 2024 — the "Grayscale tax" that absorbed nearly half of what the new entrants pulled in.

Spot Ethereum ETF vs spot Bitcoin ETF

The size gap is the comparison every institutional buyer notices first. BTC spot ETF cumulative inflows stand around $58.5 billion as of April 2026, with AUM near $102 billion. Spot Ethereum ETFs sit at roughly $12.08 billion in cumulative inflows and $13.6 billion in AUM. BTC ETF flows are nearly five times ahead of ETH ETF flows after the same calendar exposure.

The gap is not just narrative. Three structural factors explain it. First, BTC has a cleaner institutional pitch as a non-correlated store of value, while ETH carries the additional weight of being a protocol, a yield asset, and a smart-contract platform. Second, spot Ethereum ETFs at launch could not pass through ETH staking rewards, leaving roughly 3% of annualized yield on the table compared to direct ETH ownership. Third, holding patterns show that ETH ETFs are usually the second allocation, not the first: 92% of institutional holders of ETH ETFs also hold BTC ETFs, while only 24% of BTC ETF holders have added ETH ETF exposure.

| Metric | BTC spot ETFs | ETH spot ETFs |

|---|---|---|

| Trading launch | January 11, 2024 | July 23, 2024 |

| Day-1 net inflows | ≈$655M | $106.78M |

| Cumulative inflows (May 2026) | ≈$58.5B | $12.08B |

| Combined AUM | ≈$102B | $13.6B |

| Top issuer share | BlackRock IBIT ≈65% | BlackRock ETHA ≈50% |

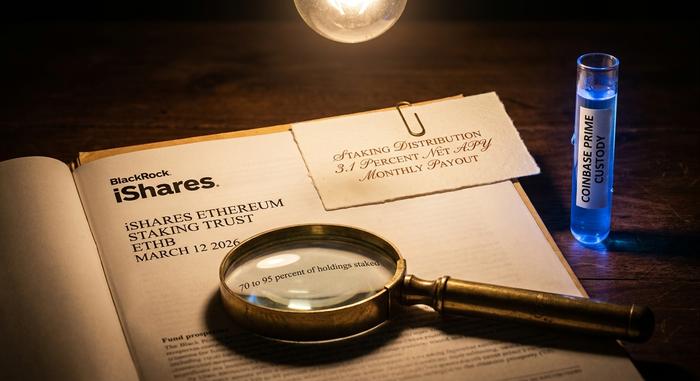

The staking-ETF era: SAB 121 repeal to ETHB launch

The most consequential change to the product class since launch happened in 13 months. The first step was SAB 121's repeal on January 23, 2025, when the SEC issued Staff Accounting Bulletin 122 and removed the rule that had forced custodial banks to record customer crypto assets as on-balance-sheet liabilities. The GENIUS Act, signed on July 18, 2025, then established a federal framework for payment stablecoins and removed several adjacent regulatory uncertainties around ETH-based settlement.

The staking unlock followed. Grayscale enabled staking on ETHE in October 2025 and distributed the first US ETH ETP staking payout — a quasi-dividend, in regulatory shorthand — on January 5, 2026, paying $0.083178 per share for the October–December 2025 reward period. BlackRock launched ETHB, the iShares Ethereum Staking Trust, on Nasdaq on March 12, 2026. ETHB stakes 70% to 95% of its underlying ETH via Coinbase Prime and passes through roughly 82% of gross staking rewards to shareholders, working out to a net yield of about 3.1% annualized, distributed monthly. The fee structure mirrors ETHA at 0.25% headline with a 0.12% promotional waiver for the first $2.5 billion or one year. ETHB drew roughly $100 million in initial assets and $15.5 million in day-1 trading volume.

For institutional buyers, that single change closed the yield gap that had argued against ETH ETF allocation. Holders no longer have to choose between regulated exposure and ETH's native return.

Who is buying spot Ethereum ETFs

Institutional adoption of ETH ETFs is real but concentrated in market-makers and multi-strategy hedge funds rather than pension funds or insurers. CoinShares analyzed Q2 2025 13F filings and counted 518 institutional filers in ETHA alone, with investment advisor holdings up 67% quarter-on-quarter to roughly 541,000 ETH and hedge fund positions nearly doubling to 296,000 ETH. The top filer list reads like a who's-who of Wall Street market makers: Goldman Sachs, Millennium Management, Susquehanna, Jane Street, Capula, and Citadel.

That last detail is worth noticing. About 93% of institutional ETH ETF filers also hold spot Bitcoin ETFs, which means the marginal demand for ETH ETFs is coming from buyers who already understood the BTC ETF wrapper. Net-new institutional capital — pension funds with first-time crypto allocations, for example — has been a much smaller share of the flow. That is partly why ETH ETFs caught up to BTC's flow trajectory only briefly in August 2025: the existing institutional buyer base added ETH, but the broader investor base did not.

Spot Ethereum ETF: pros, cons, and how to choose

The pros for most US investors are practical. ETH ETFs hold in tax-advantaged retirement accounts that cannot hold spot ETH directly, settle through standard brokerage rails, and remove wallet and key-management risk. The cons are equally practical. Spot Ethereum ETFs may charge management fees that direct ETH holding does not. They trade only during US stock-market hours rather than around the clock. And until 2025–2026, they paid no staking yield.

The choice between products comes down to fee and yield. For pure non-staking exposure, the cheapest option is the Grayscale Ethereum Mini Trust at 0.15%. For staking exposure with a tier-one issuer, BlackRock's ETHB or Grayscale's staking-enabled ETHE are the two clearest options. ETHA remains the most liquid non-staking ETF; ETHE retains the highest fee and the heaviest outflow history.

Conclusion: where spot Ethereum ETFs stand in 2026

The two-year arc of spot Ethereum ETFs traces a maturing product class. Approval to first staking payout in 18 months is fast by traditional asset-management standards. The fee war hit its expected equilibrium, the Grayscale tax played out predictably, and the staking unlock closed the most important gap with direct ETH ownership. BTC ETFs are still five times larger by inflows. The product class no longer carries the structural disadvantage it shipped with in 2024, and the next leg of the story will likely be driven less by ETF structure and more by whatever ETH itself does in 2026.