Coinbase Stock (COIN): Is Coinbase Global a Buy?

A stock that loses more than 90% of its value usually disappears from the conversation. COIN stock did the opposite. After Coinbase Global Inc cratered from its 2021 debut into the 2022 bear market, it clawed its way back and, in 2025, walked into the S&P 500 as the first crypto-native company ever added to the index. That round trip is the whole story in one line. When you buy a share of Coinbase, you are not buying a calm financial-services business. You are buying the crypto cycle with the volume turned all the way up.

This guide explains what the stock actually is, how it has behaved, where the money comes from, how it differs from simply owning Bitcoin, how to buy it, and whether the current price makes sense.

What COIN Stock Is and What Coinbase Does

Start with the mix-up that trips up almost everyone. Buying COIN is not buying a coin. COIN stock is equity, plain company shares of Coinbase Global Inc, traded on the Nasdaq under that ticker the way AAPL means Apple. It is a security that sits in your brokerage account. Not a token. Not something you stash in a wallet.

So what does the company actually do? Coinbase runs the biggest cryptocurrency exchange in the United States. Brian Armstrong and Fred Ehrsam founded it back in 2012, and these days it lets everyday investors and institutions buy and sell cryptocurrencies and other digital assets, with the kind of deep liquidity only the largest US venue has. It went public on April 14, 2021, though not through a normal IPO. It used a direct listing instead. Buy a share and you are betting on the platform sitting under all that trading, not on any single crypto asset.

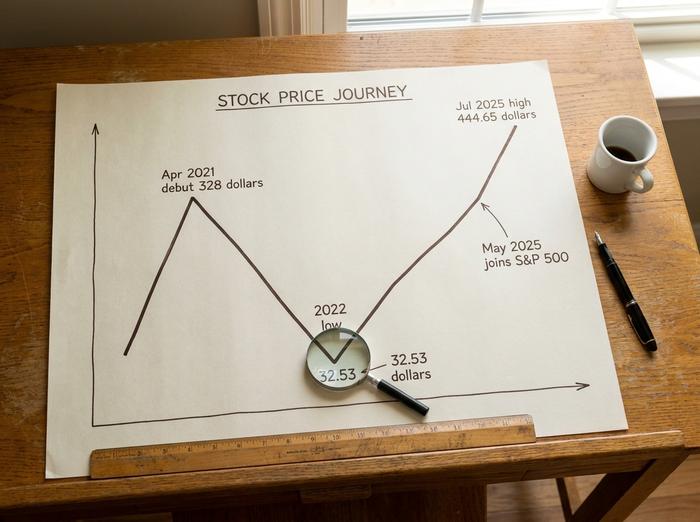

COIN Stock Price History: Boom, Crash, S&P 500

The price chart is the most honest thing about this company. It reads like a lie detector for crypto hype, and it splits cleanly into three acts.

The 2021 debut at the top

Coinbase listed at the worst possible moment, which also happened to be the most exciting one. The reference price was set at $250. Shares opened around $381 and closed near $328, valuing the company at roughly $85.8 billion on a fully diluted basis. That week, Bitcoin was printing record highs near $64,000. Everyone wanted exposure to crypto through a regular brokerage account, and COIN was the cleanest way to get it.

The 2022 wipeout

Then the cycle turned. The stock price went from a closing high of $357.39 in November 2021 to a closing low of $32.53 by the end of December 2022. That is roughly a 91% drawdown in about a year. Nothing was wrong with Coinbase the business in any unusual way. Rates were rising, trading volumes dried up, the FTX implosion poisoned sentiment, and a looming regulatory fight hung over the whole sector. The share price simply did what crypto did, only harder.

Recovery and the S&P 500 milestone

The third act surprised almost everyone. Part of the recovery had a concrete cause: when US spot Bitcoin ETFs were approved in January 2024, Coinbase became the custodian for most of them, which tied a steady institutional revenue stream to the same crypto boom that drives its trading fees. The stock reached an intraday all-time high of $444.65 in July 2025. Two months earlier, according to S&P Global, Coinbase was added to the S&P 500 on May 19, 2025, becoming the first crypto-native firm in the index, replacing Discover Financial. As of mid-2025 the share price had cooled back to around $152, putting the market cap near $40 billion. For a holding company that briefly looked like a failed bet, getting into the S&P 500 was a genuine institutional stamp of approval.

| Date | Event | Price / level |

|---|---|---|

| Apr 14, 2021 | Direct listing | Opened $381, closed $328 |

| Nov 9, 2021 | 2021 closing high | $357.39 |

| Dec 28, 2022 | Bear-market low | $32.53 |

| May 19, 2025 | Added to S&P 500 | First crypto-native member |

| Jul 18, 2025 | All-time intraday high | $444.65 |

How Coinbase Makes Money: Inside the Financials

Here is the single most important thing to understand before you buy COIN stock. On paper Coinbase is a financial services company, but most of its money still comes from trading fees, which means the income statement breathes in and out with Bitcoin's mood.

Transaction fees: the engine and the weakness

In fiscal 2025 Coinbase reported $7.18 billion in revenue, up about 9% year over year, per its annual report filed with the SEC. Transaction fees made up roughly $4.1 billion of that, or 57% of the total. Retail trading carries the fattest margins, but it is also the part that vanishes when markets go quiet. When traders get bored, this engine stalls.

Subscription and services: the steadier half

The other side of the business is the part management wants you to watch. Subscription and services brought in about $2.8 billion, or 39% of revenue. That bucket includes interest income from USDC, staking rewards, custody fees, and Coinbase One, the paid membership that has passed a million subscribers. These are the steadier, less crypto-sensitive financials, and growing them is the company's main de-risking story.

Why profit swings so hard

The diversification is real, but it is not finished. FY2025 net income came in at $1.26 billion, down 51% from the prior year. The first quarter of 2026 made the point even more sharply: revenue of $1.41 billion fell 21% from the previous quarter and the company posted a $394 million net loss, even though its share of crypto trading hit a record 8.6%. The net loss is worth a second look, because adjusted EBITDA still came in positive at $303 million in the same quarter. The gap between a reported loss and positive adjusted earnings often comes from the mark-to-market value of the crypto assets Coinbase holds on its own balance sheet, which swings with prices. Assets on the platform stood at $294 billion and the balance sheet held $10.2 billion in cash. Beyond the core exchange, Coinbase is pushing into newer lines like a prime brokerage for institutions, derivatives, prediction markets, and data analytics, all aimed at the wider onchain economy. A company can grow its market position and still report a loss in a single quarter when fee revenue drops. That is the nature of this stock.

| Segment | FY2025 revenue | Share of total |

|---|---|---|

| Transaction fees | ~$4.1B | 57% |

| Subscription & services | ~$2.8B | 39% |

| Other | ~$0.3B | 4% |

| Total | $7.18B | 100% |

COIN Stock vs Buying Bitcoin and Crypto Directly

This is the comparison most beginners actually want, and it is worth being blunt about. Treating COIN as a simple Bitcoin proxy is the mistake most newcomers make. The stock behaves like a geared, equity-wrapped version of crypto, with extra company risk bolted on.

The stock has a beta around 3.32, meaning it tends to swing roughly three times as hard as the broad market. It is correlated with Bitcoin, but it adds layers BTC does not have: business execution, regulation, share dilution, and competition. The trade-off cuts both ways. You get to hold crypto exposure inside a normal brokerage or retirement account, with no wallet, no seed phrase, and no private keys to lose. That also means you can hold it in a tax-advantaged account like an IRA, which is awkward to do with a coin directly. In exchange, you accept stock-market hours, a corporate balance sheet, no native token, and no dividend. And there is now a third option in the middle: a spot Bitcoin ETF gives you direct price exposure without the company risk, so COIN only makes sense if you specifically want to own the exchange, not just the asset.

| Dimension | COIN shares | Holding BTC directly |

|---|---|---|

| Where it lives | Brokerage / retirement account | Crypto wallet or exchange |

| Custody | Broker holds it | You hold keys, or an exchange does |

| Trading hours | Nasdaq hours only | 24/7 |

| Volatility | Higher, beta around 3.3 | High |

| Extra risks | Company, regulation, dilution | Mostly price and custody |

How to Buy COIN Stock on the Nasdaq

Buying the stock is simple, and you do not need a crypto account to do it. Three steps cover it.

First, open a brokerage account that lists US equities. Almost any mainstream broker qualifies. Second, fund the account by transferring cash. Third, search the ticker COIN, decide between a market order, which fills immediately at the current price, and a limit order, which only fills at a price you set, then place the trade during Nasdaq hours of 9:30 a.m. to 4:00 p.m. Eastern.

Two things to know before you invest. Coinbase has a dual-class share structure, and the shares the public can buy and sell are Class A. Most apps now offer fractional shares, so you can put in $50 without buying a whole share. And because the company pays no dividend, your entire return depends on the price moving up.

Is COIN a Good Stock to Buy? Analyst Insight

There is no clean yes or no here, so let me lay out both sides honestly and tell you where I land.

The bull case

The bull argument is that Coinbase is winning its market and slowly fixing its biggest weakness. Trading market share is at record highs. The revenue mix is diversifying, with USDC income and derivatives, the latter up 169% year over year, scaling fast. The regulatory cloud lifted when the SEC dropped its lawsuit against the company with prejudice in February 2025, removing an overhang that had weighed on the stock for two years. Wall Street is broadly optimistic: across roughly 34 analysts the consensus price target sits near $230 as of mid-2025, implying about 50% upside from the price at the time, with a Buy rating overall.

The bear case

The bear argument is just as grounded. At roughly 50 times earnings, the stock already prices in a healthy crypto recovery, so a flat market could leave it looking expensive. Revenue is still hostage to Bitcoin's swings. Monthly transacting users came in around 8.2 million, down 15% from a year earlier, and that single loss-making quarter in early 2026 showed how fast the operating leverage works in reverse. The same forces that triple the gains in a bull run will triple the pain in a downturn.

Where do I land? I think the business is genuinely better than its 2022 reputation, and the lawsuit being gone matters more than the market gave it credit for. But I am not convinced the multiple survives a year of boring crypto prices, and a lot of investors buying COIN stock have never actually lived through one.

Risks Every COIN Investor Should Weigh

Keep the warnings in one place rather than scattered through the optimism. For any COIN stock investor, the volatility is structural, not a phase: a beta above 3 means stomach-churning moves are the baseline. Revenue is concentrated in transaction fees, so a quiet market hits the top line directly. Competition is real and growing, from Robinhood to global exchanges to spot crypto ETFs that quietly compress fees. Regulatory tone can flip with a change of administration, and even institutions that custody assets with Coinbase can move. With no dividend, there is no income cushion to soften a bad year.

The Bottom Line: Should You Buy COIN Stock?

Coinbase is two things at once, and you have to hold both ideas in your head. It is a legitimate, profitable, now-S&P-500 business with a widening moat. It is also a high-octane proxy for an asset class that routinely falls by half. Both are true at the same time, two views of the same fact. If a 50% crypto drawdown would keep you up at night, owning COIN through one will feel worse. So the real question is not whether COIN stock is worth owning. It is whether you have the conviction in crypto itself to ride the geared version of it. Decide that first, then size the position like the volatile bet it actually is.