MARA Stock: Marathon Digital Holdings Bets on AI Compute

The largest Bitcoin miner on the planet spent early 2026 doing something its own shareholders found hard to explain. It sold roughly $1.5 billion of Bitcoin. Not because it had to cover a margin call, but to buy a power plant in Ohio. For years MARA stock traded as a leveraged way to own Bitcoin without touching a wallet. That story is changing fast, and anyone typing "mara stock" into a brokerage app in 2026 is buying a different company than the one that existed two years ago.

So what are you actually buying when you buy MARA? The rest of this piece works through the company itself, what moves its share price, the pivot remaking the business, how it stacks up against rival miners, and whether it earns a place in a portfolio.

What MARA Holdings actually does

Here is the thing most quote pages get wrong by omission: MARA is not a fund that holds Bitcoin. It is an industrial company that turns cheap electricity into Bitcoin, and increasingly into raw computing power. That distinction is the whole reason MARA stock moves the way it does.

MARA Holdings, Inc., headquartered in Fort Lauderdale, Florida, runs one of the biggest Bitcoin mining operations in the world. As of the first quarter of 2026 its energized hashrate reached about 72.2 exahashes per second, the highest of any publicly traded miner. Hashrate is just a measure of how much computing muscle a miner points at the Bitcoin network, and more of it means a bigger share of the new coins issued every day.

The company used to be called Marathon Digital Holdings, Inc., a blockchain and digital asset technology company that mined cryptocurrencies long before the rebrand. It became MARA Holdings in August 2024, dropping "Digital" to signal it wants to be seen as an energy and compute business, not a crypto novelty. It trades on the Nasdaq under the ticker MARA, is run by chief executive Fred Thiel, and sits among the largest corporate holders of Bitcoin anywhere. Before it began selling coins in 2026, MARA ranked as the second-largest corporate Bitcoin holder, behind only Strategy, the firm formerly known as MicroStrategy. It also mines Kaspa, a smaller proof-of-work coin, as a side bet. Owning the stock means owning a slice of power contracts, warehouses full of mining rigs, and a growing pile of digital assets. It is closer to an oil-and-gas wildcatter than to an exchange-traded fund.

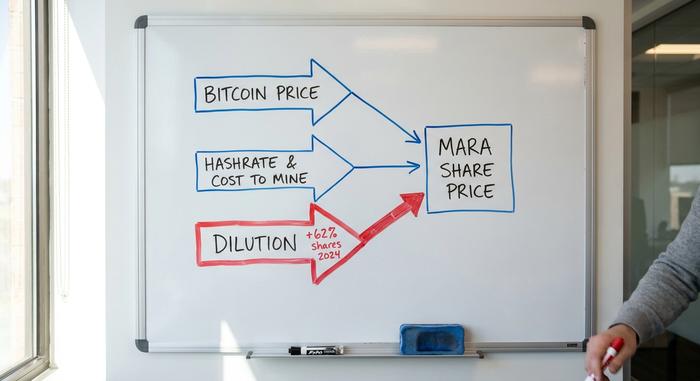

What actually drives MARA stock price

Three forces push the MARA stock price around, and the trap for new investors is assuming they move together. They do not. Understand these three and the wild price chart starts to make sense.

Bitcoin's price and the beta

Bitcoin is the engine. When BTC rises, MARA's mined coins are worth more and its treasury swells, so the stock tends to climb harder than Bitcoin itself. When BTC falls, the same leverage works in reverse and the stock gets punished. The numbers are blunt about this: MARA carries a beta above 5, meaning it has historically swung several times more violently than the broad market. A year-to-date gain of around 37 percent against the S&P 500's 8 percent sounds great until you remember the same multiplier applies on the way down.

Hashrate and the cost to mine

The second lever is operational. Mining a Bitcoin costs money, mostly electricity, and MARA's edge is power priced near $0.04 per kilowatt-hour. At that rate its direct electricity cost to mine one Bitcoin ran near $40,000 in early 2026. That cushion matters more than ever because the April 2024 halving cut the block reward in half, and "hash price" — what miners earn per unit of computing — collapsed to post-halving lows of roughly $28 to $30 per petahash per day. According to the CoinShares Q1 2026 mining report, at those levels 15 to 20 percent of the global mining fleet is running cash-negative. Scale and cheap power are what keep MARA on the right side of that line.

Dilution, the silent tax

The third lever is the one retail investors keep ignoring, and it is the bear case in a single word. To fund expansion and pay bills, MARA issues new shares, a lot of them. Share count grew roughly 62 percent in 2024 and another 59 percent through the third quarter of 2025, reaching about 371 million basic shares by early 2026. Every new share is a smaller claim on the same Bitcoin and the same machines. You can be right about Bitcoin going up and still watch your per-share value get diluted away. That is not a footnote. It is the central risk.

The 2026 pivot: from Bitcoin miner to AI infrastructure

The most important thing MARA did in 2026 had nothing to do with mining a single coin. It started selling Bitcoin to pour concrete for data centers. That is a genuine change of identity, and it is why MARA stock now behaves nothing like the simple Bitcoin proxy it once was.

The Long Ridge deal

In late April 2026 MARA agreed to buy Long Ridge Energy for about $1.5 billion, as CoinDesk reported. The deal brings a 505-megawatt combined-cycle gas plant in Ohio and more than 1,600 acres of land. The plan is to build a 200-megawatt AI data center on the site, with first capacity targeted for around mid-2028. In plain terms, MARA is buying the one thing AI companies are desperate for: power, and the land to put it on.

Why does that matter so much? Training and running large AI models eats electricity at a scale that has overwhelmed the grid in several US states, and getting a new connection approved can take years. Bitcoin miners already solved that problem for themselves. They spent the past decade locking up cheap power and building the high-voltage infrastructure to use it. A miner that owns a 505-megawatt plant can lease that capacity to an AI tenant at far higher margins than mining pays today. That is the bet in one sentence.

Selling Bitcoin to fund it

To pay for this shift, MARA sold 15,133 Bitcoin for roughly $1.5 billion during the first quarter and used part of the proceeds to repurchase convertible notes and cut debt, the company announced. Its Bitcoin treasury fell from 53,822 coins at the end of 2025 to 35,303 by the end of March 2026. For a company long defined by hoarding Bitcoin, selling a third of the stack was a loud statement. The era of "stack and hold at all costs" is over.

Partnerships and the new model

MARA is not pivoting alone. It signed a strategic partnership with Starwood and works with the compute provider Exaion, framing the whole business around a simple idea: monetize excess and stranded energy by running both Bitcoin mining and AI compute on the same digital infrastructure. When AI margins look better, point the power at AI. When Bitcoin runs hot, mine. The flexibility is the pitch.

MARA vs RIOT and CleanSpark: miner stocks compared

If you are weighing MARA stock against its rivals, the 2026 market is sending a strange message: it rewards an AI story more than raw mining scale. MARA has by far the most hashrate, yet trades at a smaller market capitalization than peers with a fraction of its mining power. Cipher Mining is the clearest example. It has nearly emptied its Bitcoin treasury to chase AI, and the market hands it a far larger price tag.

| Miner (Nasdaq) | Market cap | Energized hashrate | Bitcoin held |

|---|---|---|---|

| MARA Holdings (MARA) | ~$4.7B | 72.2 EH/s | 35,303 BTC |

| Riot Platforms (RIOT) | ~$10.25B | 36.4 EH/s | 18,005 BTC |

| CleanSpark (CLSK) | ~$4.25B | 46.2 EH/s | large holder |

| Cipher Mining (CIFR) | ~$9.18B | minimal mining | near zero |

The takeaway for an investor is uncomfortable. RIOT trades at more than double MARA's market value with roughly half the hashrate. Cipher commands over $9 billion on an AI thesis with almost no Bitcoin left to show. If you believe mining scale is what matters, MARA looks cheap. If you believe the market has already decided AI credibility is the prize, MARA looks like a miner that is late to the trade it most needs to win.

MARA is not the only one making this move. Cipher and IREN pivoted earlier and harder, and Core Scientific signed multi-year deals to host AI compute for a hyperscaler. The market has been paying up for whoever can credibly say "we are an AI infrastructure company" rather than "we mine Bitcoin." That is the gap MARA is trying to close with the Long Ridge deal. The risk is timing: if investors decide MARA arrived late, the same hashrate lead that should be an asset gets treated as yesterday's business. What could close the gap is simple and slow, namely a signed AI tenant and revenue that shows up on an earnings line, not in a slide deck.

MARA earnings and financials: the red ink

MARA's earnings reports are not for the faint of heart, and the headline numbers can mislead. A net loss in the billions sounds like a company on fire. Most of it is not what it looks like.

| MARA Q1 2026 | Figure |

|---|---|

| Revenue | $174.6M (down ~18% YoY) |

| Net loss | -$1.26B |

| Bitcoin mined | 2,247 BTC |

| Total debt | $2.2B+ |

| Cash on hand | $513.65M |

The giant loss is dominated by non-cash accounting: under fair-value rules, when Bitcoin's price drops, MARA must mark its treasury down and book the paper loss, even though it sold nothing. Revenue falling about 18 percent year over year to $174.6 million despite record hashrate, per MARA's Q1 2026 filing with the SEC, is the real story. Bitcoin's price slid and hash prices hit lows, so more machines earned less money. The debt and the cash burn, by contrast, are entirely real, and they are why the dilution keeps coming. Free cash flow ran deeply negative in the quarter, in the range of negative $300 million to negative $465 million depending on how you count the Bitcoin purchases and sales. The single number worth tracking each quarter is not the headline loss but the cost to mine one Bitcoin against the price MARA can sell it for. When that spread is positive and widening, the machine works. When it inverts, the company leans on shareholders again and the share count climbs.

The bull and bear case: what analysts forecast

Both of these descriptions are true at the same time, which is what makes MARA so hard to call.

The bull case is straightforward. MARA owns the largest hashrate among public miners, sources power near four cents, holds a substantial Bitcoin treasury, and now carries a free option on the AI data center boom. If Bitcoin runs and the Ohio buildout lands, the stock has two engines instead of one.

The bear case is just as clean. The company dilutes shareholders relentlessly, carries more than $2 billion in debt, burns cash, and remains hostage to a Bitcoin price it cannot control. The AI pivot will not produce meaningful revenue until 2028, which is a long time to wait while shares keep multiplying.

Wall Street splits the difference. As of mid-2026, the analyst consensus tracked by StockAnalysis sits at a cautious "buy," with an average 12-month target around $18, but the range is enormous, from roughly $7 at the bearish end to $30 at the bullish end. After the weak first-quarter report, Bernstein cut its target from $23 to $17. When the smart money disagrees by more than four times, that spread is telling you something: nobody actually knows.

Is MARA stock a buy or sell in 2026?

MARA only makes sense if you have a strong view on two separate questions at once. First, where does Bitcoin go over the next year? Second, is the AI pivot real or just a press release? Get both right and the leverage cuts in your favor. Get either wrong and the dilution and debt do the damage. If all you want is Bitcoin exposure, the honest answer is that you can just buy Bitcoin, with none of the share-count erosion. MARA is a bet on management execution, not only on the coin.

Conclusion

MARA stopped being a clean Bitcoin proxy the moment it started selling coins to build data centers. What you are buying in 2026 is a wager that a Bitcoin miner can reinvent itself as an energy and AI infrastructure company before relentless dilution and the next halving grind it down. The hashrate lead is real, the cheap power is real, and so is the cash burn. The question every investor has to answer is simple enough to fit on a sticky note: do you trust this team to spend your diluted dollars well? If you do, MARA stock is a leveraged bet on two booms at once. If you do not, it is an expensive way to own Bitcoin badly.