CIFR Stock: Cipher Digital’s $11B AI Data Center Bet

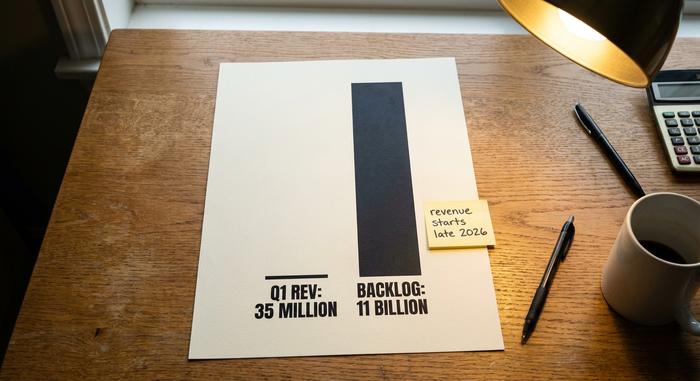

Here is a Bitcoin miner that stopped mining Bitcoin. Over the past year, the company once called Cipher Mining signed more than $11 billion in data-center leases with some of the biggest names in artificial intelligence, started pulling its mining machines out of the ground, and renamed itself Cipher Digital. The stock followed the story up, several hundred percent in twelve months. The catch is that almost none of that $11 billion has actually been paid yet. It starts landing in late 2026.

So what are you really buying when you buy CIFR stock today? Not a crypto company, not quite an AI company either, but a construction project with Amazon and Google signed at the bottom. This piece walks through what Cipher does now, how the pivot happened, what the numbers say, how it stacks up against rival IREN, and whether the bet is worth taking.

What Cipher Digital actually does now

Think of CIFR less as a crypto stock and more as a landlord. The product is not Bitcoin. The product is a building full of power and cooling, leased to companies that need somewhere to run AI computers. That single reframing is the whole reason the stock re-rated.

Cipher Mining became Cipher Digital, Inc. in February 2026, a rebrand confirmed in an SEC filing, though the ticker stayed CIFR. The company develops, owns, and operates industrial-scale data centers in the United States, with its headquarters in New York and its main sites in Texas and Ohio. It grew out of Bitfury, a veteran of the Bitcoin hardware world, and is led by chief executive Tyler Page.

For most of its life, Cipher did one thing: convert cheap electricity into Bitcoin. What changed is the customer. Instead of selling the electricity to itself in the form of mined coins, Cipher now rents its power and buildings to hyperscalers, the handful of giant cloud companies racing to build high-performance computing capacity for AI faster than the grid can support them. The mining didn't make Cipher special. The power contracts and the land did, and in 2026 those became worth far more pointed at AI than at a block reward.

The scarce resource in the AI build-out is not chips. It is power, and a place to plug it in. Getting a large new connection approved by a US grid operator can take years, and Cipher already holds interconnection rights and energized sites that would take a newcomer the better part of a decade to assemble. That head start, more than any mining hardware, is what the hyperscalers are paying for.

Cipher Digital's pivot from miner to AI host

The most striking thing about Cipher is how complete the turn has been. This is not a miner dabbling in AI on the side. Mining has been decommissioned at two of the company's three major sites, and what replaced it is a stack of fifteen-year leases with tenants most landlords would never reach.

The hyperscaler deals

Three contracts carry the story. Amazon Web Services took 300 megawatts at Cipher's Black Pearl site in Texas on a 15-year lease worth about $5.5 billion, according to Data Center Dynamics. A second 300-megawatt block at Barber Lake went to Fluidstack, an AI cloud provider, on a 10-year deal worth roughly $3.8 billion, with Google backstopping $1.73 billion of it and taking warrants in return. A third, unnamed hyperscale tenant signed for 100 megawatts at the Stingray site on another 15-year lease, a deal that sent the stock up roughly 9 percent when CoinDesk reported it in March 2026. Add it up and Cipher has put roughly 700 megawatts under contract for about $11.4 billion in total future revenue. For a company this size, those are enormous numbers tied to some of the most creditworthy names in technology.

Why do these leases matter so much more than a mining business? Because they are long, large, and signed with counterparties that pay. A 15-year contract with Amazon is a different kind of asset than a stream of Bitcoin whose value swings 20 percent in a week. Lenders treat it that way too, which is the only reason a company losing money each quarter can borrow billions at single-digit rates. The leases turn an unpredictable miner into something closer to a utility with a fixed customer list.

What is left of mining

Mining hasn't vanished entirely. Cipher still runs Bitcoin machines at its Odessa site, around 11.6 exahashes per second of capacity, and holds a small treasury of roughly 1,500 BTC, worth on the order of $95 million in mid-2026. But the direction is clear: mining is the legacy business now, expected to wind down over the next couple of years as the AI leases ramp. The Bitcoin on the balance sheet is pocket change next to the contracts.

Where Cipher came from

Cipher reached the public market as a Bitfury spin-off, which is why it had real power-infrastructure expertise from day one rather than just a warehouse of rented rigs. Bitfury had spent years building and running large-scale data centers, so Cipher inherited the engineering muscle to develop sites, not merely fill them with machines. In January 2025, SoftBank put $50 million into the company, an early signal that deeper-pocketed investors saw CIFR as more than a miner. Over the following year, management leaned fully into the pivot, signing tenant after tenant until, by 2026, the AI hosting business had become the entire company and the old name no longer fit.

CIFR financials: huge contracts, tiny revenue

Here is where new investors get tripped up. If you pull Cipher's income statement, it looks alarming. The reason is simple: the $11.4 billion has not started yet, so today's numbers reflect a shrinking mining business, not the data-center company being built behind it.

| Cipher Digital (CIFR) | Figure |

|---|---|

| Q1 2026 revenue | $34.8M (down ~42% QoQ) |

| Q1 2026 net loss | -$114.3M |

| FY2025 revenue | $223.9M |

| FY2025 net loss | -$822M |

| Cash | ~$4.2B |

| Total debt | ~$5.2B |

That $34.8 million first quarter, reported in Cipher's May 2026 business update, set against an $11 billion contracted backlog, tells you everything about the shape of this bet. You are not buying current earnings. You are buying the promise that buildings finishing in late 2026 and beyond will generate something like $669 million in annual net operating income once the leases are fully live. To get there, Cipher is raising capital and borrowing heavily. A $2 billion bond at 6.125 percent, due 2031, funds the Black Pearl build, and a further note offering of around $810 million was floated in mid-2026 to complete Stingray. The company sits on roughly $4.2 billion in cash but carries about $5.2 billion in debt. That is the trade: spend and borrow now, collect later. Every quarter of delay makes the math worse.

It helps to know why the reported losses are so large. A chunk of them is non-cash, the depreciation of expensive equipment and the write-downs tied to the shrinking mining operation, rather than money walking out the door. That does not make the losses harmless, but it does mean the headline net loss overstates the cash burn. The cleaner way to judge Cipher is to track its contracted backlog against the cost and timing of finishing the buildings. The backlog is the asset. The build schedule is the risk. Bond investors, for their part, were willing to lend at a rating just below investment grade, high-yield but only by a notch, a vote of cautious confidence rather than alarm.

CIFR vs IREN: the AI data center showdown

Search for CIFR and you will quickly run into the same question other investors are asking: is Cipher or IREN the better AI data-center stock? It is a fair fight, because both started as Bitcoin miners and both pivoted toward AI hosting. The difference is timing and proof.

| Stock | Market cap (mid-2026) | AI/HPC status | Bitcoin held |

|---|---|---|---|

| Cipher Digital (CIFR) | ~$9.2B | ~700MW contracted, leases start H2 2026 | ~1,500 BTC |

| IREN (IREN) | ~$18B | AI cloud revenue already flowing | modest |

| MARA Holdings (MARA) | ~$4.7B | early AI pivot, still mostly mining | ~35,000 BTC |

| Core Scientific (CORZ) | ~$11B | CoreWeave hosting deals signed | minimal |

IREN took a slightly different road to the same place. It built out its own AI cloud, renting graphics-processing power directly to customers, so its AI revenue already flows through the income statement quarter by quarter. Cipher chose the landlord model instead, signing long leases and letting the tenant operate the computers. MARA, by contrast, is still mostly a Bitcoin miner testing the AI waters, and Core Scientific went the hosting route earlier with deals tied to the cloud provider CoreWeave. Four former miners, four speeds, one destination.

The market's verdict is written in those market capitalizations. IREN trades at roughly twice Cipher's value because its AI revenue growth is already showing up in results, not just in contracts. Cipher's $11.4 billion is real and signed, but it is a forward number, and forward numbers carry timeline risk that flowing revenue does not. If you think Cipher will execute as cleanly as IREN has, CIFR looks like the cheaper way to own the same trend. If you think building 700 megawatts on schedule is harder than it sounds, IREN's premium is the price of certainty.

What analysts say and what could go wrong

The CIFR stock price has swung from about $3 to nearly $29 over the past year, on heavy trading volume and some of the highest implied volatility in the sector. Wall Street likes the story anyway. Cipher draws a broadly bullish consensus, with something close to a Moderate-to-Strong Buy rating across the analysts covering it and an average CIFR stock price target near $28 in mid-2026, per MarketBeat. The bulls run hot: Morgan Stanley has carried a target as high as $48.50, and Bernstein rates it Outperform around $32. But read those targets for what they are. They are not valuations in the usual sense, because there is no normal earnings stream to value. They are bets on execution.

The risks are real, and worth being blunt about. Build delays are the obvious one. Data centers slip, and every month a site sits unfinished is a month of debt service against no lease revenue. Tenant concentration is another: a huge share of the backlog rests on a few customers, and the Stingray tenant still has not been publicly named. The balance sheet is the third worry, with about $5.2 billion in debt and a share count near 409 million that has grown as the company raised money. Dilution is part of the deal here, too. The Google arrangement came with warrants, and outside investments have added shares along the way, so even a successful buildout gets split across a wider base than it started with. None of these are reasons the bet fails. They are the reasons it is a bet at all, and why the stock can drop double digits in a single session when one data point disappoints.

Is CIFR stock a buy or sell in 2026?

Any honest analysis of CIFR stock starts from one fact: it is a leveraged wager on data centers getting built on time and on budget. If you believe Amazon, Google, and the third tenant will pay as their leases promise, the stock is a discounted claim on a very large, very contracted future. If you doubt the timeline, the debt turns from fuel into a threat. There is no dividend to wait around for, so the whole return depends on the buildout landing. Know which of those two views you hold before you buy, because the stock has already priced in the optimistic one.

Conclusion

Cipher already stopped being a Bitcoin stock. What is left is a construction company with Amazon and Google as anchor tenants and a pile of debt funding the concrete. The coins are mostly sold, the buildings are not finished, and the share price moves as if they already are. That gap — between signed contracts and poured foundations — is the entire investment case. The only question that matters for CIFR stock is whether 2026 and 2027 deliver the buildings the market has already paid for. Watch the construction updates more closely than the Bitcoin price.