Crypto hedge funds: what they are, how they work, and who runs the money

Su Zhu tweeted about "supercycles" and "generational longs." Kyle Davies told podcasters that crypto was going to $10 trillion. Their fund, Three Arrows Capital, had $3.5 billion under management. Then came June 2022. A leveraged bet on Terra/Luna went sideways, the margin calls came, and $3.5 billion turned into a bankruptcy filing. Su Zhu got arrested in Singapore trying to leave the country. Kyle Davies disappeared for months.

Two months after that, Sam Bankman-Fried's Alameda Research collapsed alongside FTX. Another multi-billion dollar fund. Another set of criminal charges. Another wave of retail investors and lending platforms left holding bags of nothing.

You would think that would kill the crypto hedge fund industry. It did not. The money came back. Pantera kept raising. Galaxy kept trading. New funds launched with fancier compliance and "we are not like those guys" pitch decks. By 2025 the assets under management in crypto hedge funds had climbed past pre-crash levels. The industry learned some lessons. Whether it learned enough is the question this article tries to answer.

What a crypto hedge fund is (and what it is not)

Strip away the jargon and a crypto hedge fund is this: rich people pool their money, a manager invests it in cryptocurrency and blockchain assets, and everyone hopes the manager is smarter than the market. The "hedge" in the name is mostly historical. True hedging means reducing risk through offsetting positions. Most crypto funds are making directional bets, they think prices go up.

The manager makes all the calls. Which tokens to buy. When to sell. Whether to go long or short. How much leverage to use. Investors wire in their capital and wait for quarterly statements. If the fund makes money, everyone is happy. If it loses money, the investor still pays management fees on whatever is left.

So why would anyone pay a crypto hedge fund when they could just buy BTC on Coinbase? Two reasons.

First, access. Crypto fund managers get deal flow that regular people never see. Seed-round token allocations at 90% discounts to public listing price. OTC desk pricing for moving millions without moving the market. Direct lines to project founders and exchange operators. If you are writing a $5 million check into a pre-launch DeFi protocol, you need relationships that take years to build.

Second, strategies. A retail trader can go long on Binance. A hedge fund runs cross-exchange arbitrage at microsecond speed, harvests DeFi yield across 30 protocols simultaneously, shorts overvalued tokens while going long on undervalued ones, and does all of this with institutional risk management frameworks. Whether that skill is worth the fees is the real debate.

Getting in is not easy. Most crypto hedge funds want $100,000 to $1 million minimum. Many only accept accredited investors: net worth over $1 million or income over $200,000 per year. This world was built for institutional investors and wealthy individuals, not for someone with $5,000 looking to 10x.

| Crypto hedge fund basics | Details |

|---|---|

| Typical minimum investment | $100,000 - $1,000,000 |

| Management fee | 1-3% of AUM annually |

| Performance fee | 10-30% of profits |

| Lock-up period | 3-12 months typical |

| Investor requirements | Usually accredited investors only |

| Legal structure | Cayman Islands LP (most common) |

| Regulation | SEC/CFTC (US), varies by jurisdiction |

How crypto hedge funds make money: the strategies

The strategy a fund picks tells you almost everything about the risk you are taking with your money.

Long-only is the lazy version. Buy bitcoin, buy ethereum, sit on them. When the market rips, the fund looks brilliant. When it crashes, you crash with it. Pantera's Bitcoin Fund ran this playbook and posted absurd lifetime returns because they started in 2013 when BTC was under $100. The manager adds value by timing entries and managing position sizes. But the bet is simple: crypto goes up over the long run.

Long/short funds try to make money in both directions. They go long on tokens they think will rise and short the ones they think will drop. A manager might buy ETH and short a competing L1 that they consider overvalued. Sounds great on paper. In practice, crypto correlations spike during crashes. Everything drops at once. The "short" leg does not save you when BTC falls 30% and drags the entire altcoin market down with it.

Quant and algo funds run math instead of opinions. Their computers watch dozens of crypto exchanges at once, looking for tiny price differences. BTC is $60,000 on Binance and $60,050 on Kraken? The bot buys on Binance and sells on Kraken before a human could finish reading this sentence. Funding rate arbitrage on perps, statistical order book patterns, and mean-reversion signals all fall into this bucket. The opportunities exist because crypto is messier and less efficient than stock markets.

Crypto venture funds write big checks into blockchain projects before tokens launch. a16z Crypto put money into Uniswap, Optimism, and dozens of other protocols at seed-stage prices. When those tokens launched publicly at 10-50x the seed price, the returns were staggering. Of course, for every Uniswap there are ten projects that shipped nothing and the tokens went to zero. Venture is the highest-upside, highest-failure-rate strategy in the crypto fund world.

DeFi yield funds farm returns from protocols. Provide liquidity on Curve and Uniswap. Stake governance tokens. Run basis trades between spot and futures. The income flows regardless of price direction, which sounds safe until a smart contract exploit drains the pool your fund was farming.

Pure arbitrage exploits price gaps across exchanges. Tiny margins per trade, massive volume. The edge comes from speed, capital efficiency, and infrastructure. If your servers are 3 milliseconds closer to the exchange than the next guy's, you win the trade.

The biggest crypto hedge funds in 2026

The landscape changed dramatically after 2022. The collapse of Three Arrows Capital, Alameda Research, and several smaller funds wiped out billions. What remains in 2026 are the survivors and the new entrants who built on the wreckage.

| Fund | AUM (approx.) | Primary strategy | Founded | Notable |

|---|---|---|---|---|

| Pantera Capital | $4.5B+ | Multi-strategy (venture + liquid) | 2013 | First US crypto fund, 210+ investments |

| a16z Crypto | $7.6B raised | Venture | 2018 | Largest crypto VC, backed Coinbase/Uniswap |

| Paradigm | $8.5B+ raised | Venture + research | 2018 | Led investments in dYdX, Optimism, Blur |

| Galaxy Digital | $3B+ | Multi-strategy | 2018 | Mike Novogratz, public company (GLXY) |

| Polychain Capital | $1B+ | Liquid tokens + venture | 2016 | Olaf Carlson-Wee (first Coinbase employee) |

| Multicoin Capital | $1B+ | Long-biased liquid | 2017 | Solana thesis, research-driven |

| Bitwise | $10B+ | Index funds + ETFs | 2017 | Largest crypto index fund manager |

| Hashdex | $3B+ | ETFs + index | 2018 | Nasdaq Crypto Index partnership |

| Brevan Howard Digital | $2B+ | Macro + quant | 2022 | TradFi pedigree, institutional grade |

| Grayscale | $25B+ | Trust/ETF products | 2013 | GBTC, largest crypto fund by AUM |

A few observations. The biggest names are not pure hedge funds in the traditional sense. Grayscale runs trust products and ETFs. Bitwise runs index funds. a16z and Paradigm are venture capital firms that happen to operate in crypto. The lines between hedge funds, venture capital, and asset managers have blurred in crypto because the market rewards flexibility.

Pure trading hedge funds, the ones that actually run long/short and quant strategies, tend to be smaller and more secretive. Many do not disclose AUM or performance publicly. The ones that consistently perform well attract capital through word of mouth in institutional circles, not through marketing.

The fee problem: what crypto hedge funds charge

Wall Street runs on "2 and 20." Two percent of your money every year whether the fund makes money or not, plus twenty percent of whatever profits they generate. Crypto funds said "cute" and made it worse.

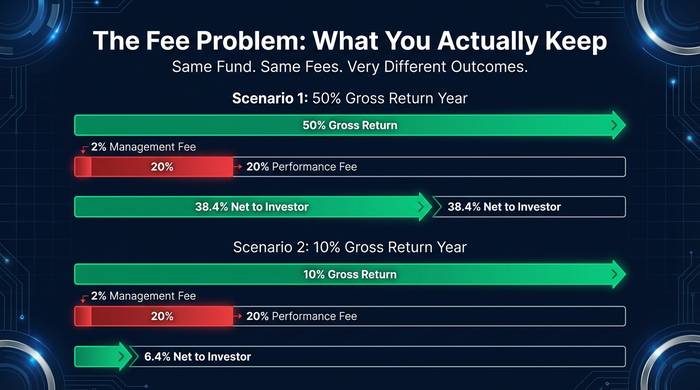

Management fees in the crypto fund world run 1-3% annually. Performance fees sit between 10-40%. I have heard of funds charging 50% of profits. Fifty percent! The pitch is always the same: "crypto is harder than stocks, we have unique alpha, trust us." Maybe. But a 3% management fee on a $1 million investment means $30,000 per year leaves your pocket before the fund earns you a single dollar.

Let me do the math that fund marketing decks never show you. Your fund returns 50% this year. Great year. With 2% management and 20% performance fees, you actually keep about 38.4%. Still good. Now imagine a mediocre year: 10% gross return. After fees? You keep 6.4%. The fund manager still got paid handsomely. And in a losing year? You pay the 2% management fee on top of your losses. The incentives are asymmetric by design. Fund managers get rich on management fees whether they perform or not. Performance fees are the bonus.

One protection worth demanding: a high-water mark. If the fund drops 30% and then recovers 25%, you should not pay performance fees during the recovery because the fund has not beaten its previous peak. Any fund that does not offer a high-water mark is telling you they care more about their fees than your returns. Walk away.

What went wrong: the 2022 crypto fund collapse

The 2022 wipeout killed more institutional capital than any single event in crypto history. Understanding what happened explains why the industry looks the way it does today.

Three Arrows Capital borrowed billions from crypto lending platforms, used the borrowed funds to make leveraged bets, and when those bets went wrong, the fund could not repay. The cascade: 3AC defaults triggered the collapse of Voyager Digital, Celsius, and BlockFi, each of which had lent money to 3AC or held similar positions. An estimated $40+ billion in value evaporated across the ecosystem.

Alameda Research, the trading firm run by Sam Bankman-Fried alongside the FTX exchange, turned out to be using FTX customer deposits to fund its trades. When this came to light in November 2022, both FTX and Alameda collapsed. Bankman-Fried was convicted of fraud and sentenced to 25 years in federal prison.

What do 3AC and Alameda have in common? Both used ridiculous leverage. Both had zero external oversight. Both mixed roles that should never be mixed (3AC borrowed from platforms they invested in; Alameda traded on an exchange its boss owned). And both operated in jurisdictions where nobody checked the books until it was too late.

The survivors learned. Not out of virtue. Out of necessity. Institutional investors in 2026 demand third-party custodians, regular audits, and clear separation between fund management and exchange operations. The funds that cannot provide these assurances do not raise money. The regulatory environment shifted too. The SEC and CFTC pay attention to crypto funds now in ways they did not before SBF's trial made headlines for six months straight.

How to get exposure to crypto hedge fund strategies

If you do not meet the accredited investor threshold or do not want to commit six figures to a single fund, alternatives exist.

Bitcoin and crypto ETFs give institutional-grade exposure through a standard brokerage account. Grayscale, Bitwise, and BlackRock all offer crypto ETFs with management fees under 1%. You do not get active trading alpha, but you get professional custody and regulatory protection.

On-chain alternatives like Enzyme Finance and dHEDGE let you invest in crypto strategies managed by traders whose performance is fully transparent and verifiable on the blockchain. Minimum investments start from a few hundred dollars. The tradeoff: smart contract risk replaces counterparty risk.

Crypto fund-of-funds pool capital across multiple crypto hedge funds, providing diversification. The downside: an additional layer of fees on top of the underlying funds' fees.

I want to be straight about this: for most people reading this article, a crypto hedge fund is probably not the right move. If you have $10,000 or even $50,000 to invest in crypto, buying BTC and ETH through Coinbase or a BlackRock ETF captures most of the upside without the fees, the lock-ups, or the counterparty risk. The alpha a fund manager generates has to beat their fees, and most do not beat simple buy-and-hold over a full market cycle.

Crypto hedge funds make sense for people with seven figures looking for diversified crypto exposure managed by professionals, or for institutional investors who cannot hold tokens directly for regulatory or compliance reasons. For everyone else, the ETF route is cheaper, simpler, and you can sell any day you want.

The on-chain alternatives deserve a mention because they are genuinely interesting. Enzyme Finance and dHEDGE run on Ethereum and let anyone invest in strategies managed by traders whose performance is 100% verifiable on the blockchain. No hiding bad months. No lying about returns. Every trade, every fee, every withdrawal sits on chain for anyone to audit. Minimum investments start at a few hundred dollars. The tradeoff: you are trusting smart contracts instead of a fund administrator, and smart contracts can be exploited. But the transparency is something traditional crypto hedge funds still cannot match.

If you are deep enough in crypto to care about this space but not rich enough for the minimums, on-chain vaults might be the smartest entry point. Learn how hedge fund strategies work with a small allocation, see if the returns justify the risk, and decide later whether to commit serious capital.