CORZ Stock: Core Scientific Inc and Its AI Pivot

Most companies are thrilled when a buyer offers to take them out at a premium. Core Scientific's owners did the opposite. In 2025 their single biggest customer offered roughly nine billion dollars for the whole company, and 91.5% of voting shareholders said no. They turned down the cheque because they believe CORZ stock is worth more on its own, riding the AI buildout, than it would be folded into someone else. That bet is the whole story. Core Scientific is a Bitcoin miner that went bankrupt, came back, and is now reinventing itself as a landlord for artificial intelligence. The stock swings hard because the market still cannot agree what that reinvention is worth.

This guide explains what CORZ is, how it came back from bankruptcy, the AI pivot at the center of it, the buyout that fell apart, the messy financials, and whether the price makes sense.

What CORZ Stock Is and What Core Scientific Does

Start with the basic confusion. Despite the name, CORZ is not a coin but the Nasdaq ticker for shares of Core Scientific Inc, a real operating company you hold in a brokerage account.

Core Scientific was founded in 2017 and is based in Dover, Delaware. At heart it is a data-center business. It runs three segments: colocation, where it rents out powered and cooled space to other companies; digital asset mining for its own account, known as self-mining; and hosted mining, where it runs other miners' machines. Across roughly 1.9 gigawatts of gross power and ten data centers in seven states, the company's real product is electricity, cooling, and floor space at industrial scale. That detail matters more than it sounds, and the rest of this article explains why. At a recent quote near $29, the stock price puts the company's market capitalization at roughly $9 billion, and major index providers now classify it as a technology and infrastructure business rather than a pure crypto miner.

From Bankruptcy to Nasdaq: The CORZ Comeback

CORZ stock is jumpy for a reason. It has already round-tripped once, from near-zero to a multi-billion-dollar valuation, and anyone who held it through that ride knows how fast the story can flip.

Chapter 11 in 2022

In December 2022, Core Scientific filed for Chapter 11 bankruptcy protection in the Southern District of Texas. The timing could hardly have been worse. Bitcoin had collapsed. Power prices had spiked. And the company was on the hook to Celsius, the crypto lender that had just blown up. Mining margins flipped negative, debt came due, and the equity was all but wiped out. For months the stock traded like a lottery ticket on the company's survival.

Emergence and relisting

The turnaround came just as fast. Core Scientific emerged from bankruptcy in January 2024, and its shares were back trading on the Nasdaq within weeks, at a low single-digit price, around $3.44. Then the AI story caught fire. The stock ran several hundred percent off that relisting price, a gain north of 490%. A company left for dead became one of the hottest names in the data-center business.

The price round-trip

Today the shares change hands near $29, inside a 52-week band of roughly $10.93 to $30.46. The beta? About 5.48. That means CORZ tends to swing close to five times as hard as the broad market. Not a typo. It is one of the most volatile stocks you can buy on a major US exchange, and that bankruptcy-to-comeback history is exactly why.

| Date | Event | Price / level |

|---|---|---|

| Dec 21, 2022 | Files Chapter 11 | Equity near zero |

| Jan 23, 2024 | Emerges from bankruptcy | Restructured |

| Jan 24, 2024 | Relists on Nasdaq | About $3.44 |

| 2025-2026 | AI re-rating | 52-wk $10.93-$30.46 |

| Jun 2026 | Recent price | About $29 |

The CORZ AI Pivot: From Mining to HPC Hosting

Here is the most important idea in the entire CORZ stock story. Core Scientific's real product is no longer Bitcoin. It is megawatts of powered, cooled, grid-connected space, and AI companies will pay a large premium for exactly that.

The CoreWeave deal

The pivot has a name, and that name is CoreWeave. Core Scientific signed a series of contracts to host CoreWeave's high-performance computing, eventually covering roughly 590 megawatts of critical IT load across six sites. The contracts run for twelve years on take-or-pay terms, meaning CoreWeave pays whether or not it uses the capacity, and CoreWeave funds the capital build. Management has put the cumulative contracted revenue at about $10.2 billion. For a company that used to live and die on the Bitcoin price, that is a different kind of business entirely.

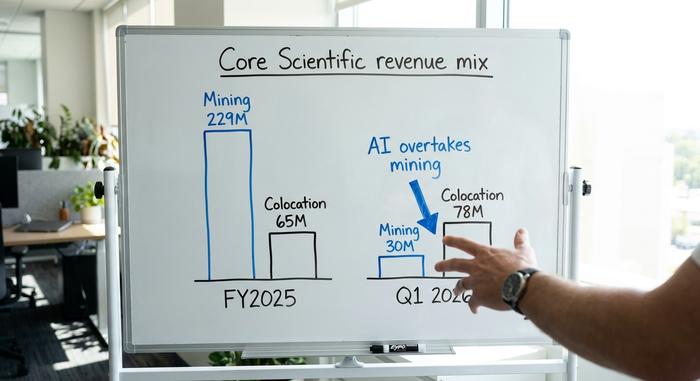

The revenue crossover

The numbers show the shift in real time. Full-year 2025 revenue came in at $319.0 million, down 38% year over year as the mining side shrank. Then the first quarter of 2026 told the new story: revenue of $115.2 million, up 45% from a year earlier, with colocation revenue of $77.5 million overtaking self-mining's $30.1 million for the first time. The data-center business is now the bigger half.

Why mining gets repurposed

The logic is simple once you see it. The grid interconnects, the land, and the power contracts that took Core Scientific years to assemble are worth far more hosting AI workloads than they are hashing Bitcoin. Colocation revenue grew roughly 801% year over year as that capacity was redirected. Each colocation customer is essentially renting Core Scientific's power and cooling to run racks of AI chips, and management wants to grow that footprint toward 4.5 gigawatts over time. The same site that once earned a few cents per kilowatt-hour mining Bitcoin can earn far more hosting a GPU cluster that runs around the clock. Bitcoin mining built the infrastructure; AI is what finally pays for it.

| Segment | FY2025 | Q1 2026 |

|---|---|---|

| Colocation (AI/HPC) | $65.4M | $77.5M |

| Digital asset self-mining | $229.2M | $30.1M |

| Hosted mining | $24.4M | smaller |

| Total revenue | $319.0M | $115.2M |

The $9B CORZ Buyout Shareholders Rejected

Now the most revealing moment in the whole saga. In July 2025, CoreWeave, already Core Scientific's dominant customer, offered to buy the entire company in an all-stock deal worth about $20.40 per share, or roughly nine billion dollars. On paper, an acquisition by your biggest client at a premium sounds like a clean exit. CoreWeave is an AI cloud provider that rents out Nvidia GPUs to companies training and running large models, and it had leaned on Core Scientific for the physical space to put them in. Buying its landlord outright would have locked in that capacity for good.

Shareholders did not see it that way. When the vote came, 91.5% of those voting rejected the deal, and the merger agreement was terminated in October 2025 with no termination fee. The objection was straightforward. An all-stock offer tied the payout to CoreWeave's own share price, the headline number looked low against the optionality of the AI buildout, and accepting it would have handed most of the future upside to the buyer. Owners decided the standalone company, AI contracts and all, was worth more than the cheque. Whether they were right is the open question hanging over CORZ stock today.

CORZ Financials: Losses, Debt, and Cash

The headline financials look frightening until you read the footnotes. The real concern is not the loss line; it is the balance sheet.

On a GAAP basis, Core Scientific reported a net loss of about $288.6 million for full-year 2025 and a striking $347.2 million loss in the first quarter of 2026. But most of that is non-cash. A large chunk comes from mark-to-market accounting on warrants and contingent value rights, paper swings that move with the share price rather than the operating business. Strip those out and adjusted EBITDA actually turned slightly positive at around $4.4 million in the first quarter of 2026, with gross margin near 26%. The operating company is closer to breakeven than the loss suggests. The harder facts are the financing ones: roughly $3.3 billion of 7.75% senior secured notes due 2031, about $1.04 billion of liquidity, and negative shareholders' equity of around -$1.1 billion. Core Scientific is funding a massive buildout, and it is doing it with debt. The table below puts the key financial information in one place.

| Metric | Figure |

|---|---|

| FY2025 revenue | $319.0M (-38% YoY) |

| Q1 2026 revenue | $115.2M (+45% YoY) |

| Q1 2026 adjusted EBITDA | +$4.4M |

| Senior secured notes (7.75%, due 2031) | $3.3B |

| Liquidity (Q1 2026) | ~$1.04B |

| Shareholders' equity | about -$1.1B |

Is CORZ Stock a Good Buy? Analyst View

There is no clean answer here, so let me lay out both sides and where I land.

The bull case

Wall Street is unusually bullish, and the analyst ratings lean firmly to one side. The consensus rating sits at Strong Buy across roughly sixteen to eighteen analysts, with a twelve-month price target near $32 as of mid-2026, implying meaningful upside from the high-$20s. The case rests on the backlog: about $10.2 billion of contracted revenue on long take-or-pay terms, colocation revenue up some 801% year over year, and a power roadmap that management hopes to push toward 4.5 gigawatts. If AI demand for data-center capacity stays hot, Core Scientific has the land, power, and contracts to ride it. Several analyst houses, including Bernstein, have framed the company as one of the cleaner public ways to own the AI data-center buildout rather than the chips themselves.

The bear case

The bear case is just as concrete. The stock's beta of 5.48 means it can halve in a bad month. Nearly all of the high-performance computing revenue depends on a single customer, CoreWeave, which is itself burning cash and only went public in 2025. Layer on negative equity, $3.3 billion of debt, and a disclosed accounting restatement, and the risk profile is steep. Bitcoin mining still contributes real revenue, so the old crypto-cycle exposure has not fully gone away either. And funding the data-center expansion may require issuing more shares, which would dilute existing investors just as the growth arrives.

Where do I land? The pivot is genuine, and the shareholder rejection tells me insiders believe the standalone numbers. But a business this leveraged, riding on one cash-burning customer, is not something I would size large. The upside is real; so is the chance of a brutal drawdown.

Key Risks Every CORZ Investor Faces

Keep the warnings together rather than scattered through the optimism. The biggest is customer concentration: lose CoreWeave and the AI thesis cracks. The volatility is structural, with a beta above 5. The balance sheet carries heavy debt and the risk of further share dilution to fund the buildout. Execution risk is real, since delivering multiple gigawatts of data centers on schedule is hard. Bitcoin's price still moves a chunk of revenue. And there is no dividend, so the entire return depends on the share price climbing.

The Bottom Line: Is CORZ Stock Worth It?

Core Scientific is a leveraged bet that two things hold up at once: AI compute demand and the financial health of a single customer. Wrap that around a company that was bankrupt two years ago, and you get a stock that can move 5% before lunch. The 91.5% rejection of the buyout tells you the people closest to it believe the standalone story. The 5.48 beta tells you the market has not settled the price. So the real question is not whether CORZ stock is cheap. It is whether you believe the AI buildout and CoreWeave's survival firmly enough to ride the volatility. Decide that first, then size the position like the high-risk bet it actually is.