MSTR Stock: Strategy Inc, Nasdaq’s Leveraged Bitcoin Bet

A stock can lose two-thirds of its value in twelve months and still wear a "strong buy" rating with a price target three times higher than where it trades. That is roughly where MSTR stock sits in 2026. Shares of Strategy Inc, the company most people still call MicroStrategy, change hands around $120 after touching $457 a year earlier. Wall Street analysts keep pinning targets above $350 on it. Both things are true at once, and the gap between them is the whole story.

MSTR is not a normal technology share. It is Bitcoin with the volume turned up, wrapped in a corporate balance sheet that can both amplify the gains and invent new ways to lose. This article skips the live ticker and explains the engine underneath: what the company actually is now, how it manufactures Bitcoin exposure, why the stock fell so hard, and whether it makes more sense than simply buying Bitcoin or a spot ETF.

What MSTR stock is now: Strategy Inc on Nasdaq

The name on the Nasdaq ticker changed in February 2025, when MicroStrategy Incorporated rebranded to "Strategy". The ticker stayed MSTR. But the thing the ticker represents had already changed years before the logo did.

From business intelligence to bitcoin treasury company

Strategy was founded in 1989 by Michael Saylor and Sanjeev Bansal, and for three decades it sold business intelligence and enterprise analytics software out of Tysons Corner, Virginia. That business still exists. It is now branded Strategy One, an AI-powered enterprise analytics software platform, and it brings in roughly $490 million a year. The problem is that almost nobody buys the stock for it. The software unit runs at an operating loss and shrinks most quarters, and it is a rounding error next to the company's real position.

In August 2020, Saylor started moving the corporate treasury into Bitcoin. What began as a hedge against cash sitting idle turned into the entire identity of the firm. Today Strategy is a bitcoin treasury company first and a software vendor a distant second.

Michael Saylor and the conviction bet

Saylor stepped back from the CEO role but remains executive chairman and the public face of the strategy. His pitch has been consistent to the point of stubbornness: Bitcoin is the best treasury asset on earth, fiat cash is a melting ice cube, and a public company should hold as much BTC as it can finance. He turned that conviction into a machine for raising money and converting it into coins.

The software business nobody prices anymore

Here is a useful test. Strip out the Bitcoin, and what is Strategy worth? A few billion dollars, maybe, for a slow-growing software business with thin margins. Yet MSTR's market cap has run into the tens of billions. The difference is the Bitcoin, the leverage on top of it, and the premium investors were once willing to pay for both.

How MSTR's leveraged Bitcoin engine works

This is the part every MSTR stock-quote page leaves out, and it is the only part that matters. Strategy does not just hold Bitcoin. It runs a financial engine designed to grow the amount of Bitcoin backing each share over time. Understand the engine and the stock stops being mysterious.

The mNAV flywheel

The core trick is selling stock for more than the Bitcoin it already owns is worth. When MSTR traded at, say, 1.5 times the value of its Bitcoin holdings, Saylor could issue new shares through an at-the-market program, take the cash, buy more BTC, and end up with more Bitcoin per existing share than before. Existing holders got diluted in share count but enriched in Bitcoin terms. That ratio, market value divided by the value of the Bitcoin held, is called mNAV. As long as it stays above 1, the flywheel spins in the company's favor.

The catch is brutal in reverse. When mNAV falls below 1, issuing shares destroys Bitcoin per share instead of creating it, and the flywheel stalls.

Convertible notes and the preferred stack

Equity is only one fuel source. Across 2025 the company raised tens of billions through a standing at-the-market share program, then added roughly $8.2 billion in convertible notes, many at very low or zero interest, betting share prices would climb enough to convert the debt into stock. On top of that sits a tower of preferred shares trading under tickers like STRK, STRF, and STRC, worth around $15 billion in notional value. Those preferreds pay a dividend — the common MSTR stock does not.

That detail matters more than it sounds. The dividend obligations on the preferred stack have to be paid in cash, which means the engine now has a fuel bill.

What economic exposure to bitcoin means per share

Strategy markets all of this as offering investors "economic exposure to bitcoin" in different risk flavors. The metric Saylor points to is BTC yield: the percentage growth in Bitcoin per share over time. It ran at about 9.6% in the first part of 2026 and 22.8% across all of 2025. When BTC yield outruns dilution, long-term holders win. When it doesn't, they are just paying for leverage.

MSTR stock price in 2026: near the lows

The MSTR stock price tells you when the premium died. MSTR trades near $120 in mid-2026, against a 52-week range of $104.17 to $457.22. That is down roughly 68% from a year earlier and about 20% on the year, with a beta near 3, meaning it swings about three times as hard as the broader market. Market cap sits around $42 billion, and short interest runs near 12% of the float. Over the same year Bitcoin itself fell far less than MSTR did, which is leverage working in reverse: the same machine that magnified the gains on the way up magnified the losses on the way down.

Then came the moment that broke the brand. In late May 2026, Strategy sold 32 Bitcoin for about $2.5 million, its first sale since 2022. The amount was trivial — the signal was not. After years of "never sell," the company parted with coins to help fund its preferred dividends, and traders noticed that the capital structure now creates its own quiet pressure to sell. With Bitcoin near $63,000 as of June 2026 against an average cost basis of $75,699, the treasury sat roughly 17% underwater on paper, an unrealized loss north of $10 billion.

MSTR key statistics and financials

For most companies you read the income statement first. For MSTR stock, the income statement is noise. New fair-value accounting rules force Strategy to mark its Bitcoin to market every quarter, which produced a reported GAAP net loss above $12 billion in the first quarter of 2026, almost entirely from a paper swing in BTC's price. The numbers that actually describe the business are the Bitcoin count, the cost basis, the share count, and the debt. By those measures Strategy is in a league of its own: it holds 843,706 BTC, the largest corporate Bitcoin position on earth, bought at an average price of $75,699 a coin for a total outlay near $63.9 billion.

| MSTR key statistics (as of June 2026) | Figure |

|---|---|

| Share price | ~$120 |

| 52-week range | $104.17 - $457.22 |

| Market capitalization | ~$42 billion |

| Diluted shares outstanding | ~334 million (up from 192.5M in 2024) |

| Bitcoin held | 843,706 BTC |

| Average cost per BTC | $75,699 (total ~$63.9B) |

| Convertible notes | ~$8.2 billion |

| Preferred equity (STRK/STRF/STRC) | ~$15 billion notional |

| Beta | ~3.0 |

| Average daily trading volume | ~18.5 million shares |

| Short interest | ~12% of float |

The share count is the line to watch. Diluted shares climbed from 192.5 million in 2024 to about 334 million by early 2026, a 73% jump in two years. That is the cost of the flywheel: every coin was partly bought with new stock.

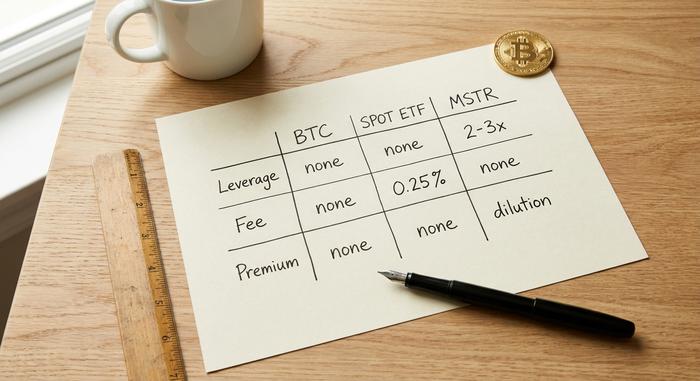

MSTR stock vs Bitcoin vs a spot Bitcoin ETF

If your goal is Bitcoin exposure, MSTR is one of three obvious routes, and they behave very differently. You can buy the coin and hold it yourself, buy a spot Bitcoin ETF such as BlackRock's IBIT or Fidelity's FBTC, or buy MSTR and ride the leveraged version.

| Route | Leverage | Premium/discount | Fee | Main risk |

|---|---|---|---|---|

| Self-custody BTC | None | None | Network fees only | You hold the keys |

| Spot ETF (IBIT/FBTC) | None | Tracks BTC closely | ~0.25%/year | Counterparty, no keys |

| MSTR stock | 2-3x effective | Can swing far above or below NAV | No fee, but dilution | Premium collapse plus debt |

When MSTR can beat holding BTC

In a strong Bitcoin bull market with MSTR trading at a premium, the stock can outrun the coin. Leverage works in your favor, the flywheel adds Bitcoin per share, and the convertible structure gives extra upside. From 2020 through 2024, that is exactly what happened, and MSTR crushed Bitcoin's own return.

When a spot ETF is the cleaner bet

If you just want Bitcoin's price without the corporate machinery, spot Bitcoin ETFs are hard to beat. No premium to overpay, no dilution eating your stake, a fee around a quarter of a percent, and a price that tracks BTC tightly. IBIT alone holds tens of billions in assets for a reason. For most investors who want crypto exposure inside a brokerage account, it is the boring, correct answer.

The premium you pay, and the discount that traps you

The danger sits in that premium. Buyers in 2024 paid well above the value of Strategy's Bitcoin on the belief the premium would hold. By June 2026 mNAV had fallen to roughly 0.7, meaning MSTR traded below the value of the Bitcoin it owns, against a historical average closer to 1.5. Anyone who bought the premium watched it evaporate, a loss layered on top of Bitcoin's own decline. I keep coming back to that asymmetry: you can be right about Bitcoin and still lose money on MSTR.

The risks of investing in MSTR's Bitcoin bet

MSTR stock, as a treasury company built on leverage, has more failure modes than the asset it holds. The biggest is the premium-to-discount flip already underway: once the stock trades below its Bitcoin value, the engine that created shareholder value runs in reverse, and every new share sold erodes the rest.

Dilution is permanent. Those 334 million shares will not shrink, and funding more Bitcoin means issuing more. Debt adds another layer. The convertible notes have to be refinanced or converted, and the preferred dividends are now a real cash outflow, which is why the company sold coins in May. There is also index risk: Strategy was passed over for the S&P 500 in late 2025, kept its Nasdaq-100 seat, and saw MSCI freeze its index weight in January 2026, removing a steady source of passive buying. If a later review forces crypto-treasury companies out of major benchmarks, the index funds that track them would have to sell MSTR mechanically, no matter the price.

One myth deserves killing. People assume a Bitcoin crash triggers a forced fire sale of the treasury. The convertible debt is largely unsecured, so there is no margin call dumping coins onto the market overnight. The pressure is slower and subtler: dividend bills, refinancing windows, and a share price that no longer supports cheap fundraising.

What analysts say about the MSTR forecast

The analyst picture on MSTR stock is the strangest part. Consensus targets cluster between $324 and $351, with multiple firms rating MSTR a strong buy, implying something like 190% upside from current levels. Read that gap carefully. These targets are mostly Bitcoin-bull models that assume BTC climbs and the premium returns. Roughly fourteen analysts cover MSTR, and the wide spread between their high and low targets is itself a sign of how little real consensus exists. The numbers lag the live price and tell you more about crypto forecasts than about the stock. I'd read them as a bet on Bitcoin's direction, not a promise about MSTR.

Is MSTR stock worth buying in 2026?

MSTR stock is a leveraged, premium-bearing, corporate-wrapped bet on Bitcoin. In a bull run it can beat the coin handily. In a downturn it gives you Bitcoin's fall plus a collapsing premium plus debt and dilution risk the coin never had. If you want clean Bitcoin exposure, a spot ETF does it cheaper and simpler. If you want a high-conviction, high-volatility leverage play and you understand the engine, MSTR is the most aggressive way to express it on a stock exchange. The real question is not where the price goes next week. It is whether you are buying Bitcoin, or buying Michael Saylor's machine for financing it. Those are not the same trade.