HUT Stock: Hut 8 Corp’s Mining-to-AI Pivot Bet

Two years ago, HUT was a Bitcoin miner. Today the market values Hut 8 stock at about 2.7 times the size of Marathon Digital, a company that mines almost three times more Bitcoin. The stock is up roughly 560% over the past year. Nothing about Hut 8's mining business explains that gap. Something else does, and it is the reason HUT now trades like a technology infrastructure company rather than a crypto miner.

That something is artificial intelligence, or more precisely the data centers that power it. This article skips the live quote and explains what actually changed: how a Bitcoin miner rebuilt itself into an energy and compute platform, why the stock re-rated so violently, how it stacks up against other miners, and what could still break the thesis.

What HUT stock is now: Hut 8 Corp

The label "Bitcoin miner" no longer fits Hut 8 Corp, even though that is still how most screeners and financial sites classify hut stock. The company now describes itself as an energy infrastructure platform that integrates power, digital infrastructure, and compute at scale. Bitcoin is still on the balance sheet, but it is no longer the headline act.

From Bitcoin miner to energy infrastructure platform

Hut 8 spent its early years doing what every miner does: running rooms full of machines to earn Bitcoin. The pivot was a recognition that the hard, valuable asset it had been building was never really the Bitcoin. It was the thing underneath the mining: secured power, land, substations, and the operational skill to run enormous energy loads. Those same ingredients are exactly what AI data centers need, the kind of energy-intensive facilities that demand secured power above all else, and the buyers for AI capacity pay far more reliably than a volatile coin does. So management, led by CEO Asher Genoot from the company's Miami base, started pointing the energy at compute instead of hashing.

The four segments: Power, Digital Infrastructure, Compute

Today Hut 8 reports across four segments: Power, Digital Infrastructure, Compute, and a catch-all Other. Power is the energy portfolio that feeds everything. Digital Infrastructure is the physical build: the data centers themselves. Compute is the revenue from running AI and high-performance computing workloads, spanning GPU-as-a-service, cloud infrastructure, and colocation for tenants, plus the legacy ASIC compute that mining now sits inside. The structure tells you where management's attention has gone. Mining used to be the whole company; now it is one line inside one segment. The Power segment is the real engine. Hut 8 has assembled a development pipeline of more than 2.5 gigawatts of energy capacity across new and existing sites, and secured power at that scale is the scarce resource every AI tenant is chasing. The company is effectively a landlord for electricity, and electricity is what the AI boom is short of.

Where Bitcoin fits now

Hut 8 still holds about 10,278 BTC, worth roughly $647 million, all of it self-mined and held long term. That treasury matters, and it still moves with the Bitcoin price. But the company has quietly stopped calling mining its long-term strategic focus. The coins are a legacy asset now, not the plan. Still, holding that Bitcoin gives Hut 8 something most pure data-center operators lack: a multi-hundred-million-dollar reserve that rises with crypto bull markets and can be borrowed against. The company has used the stack as collateral, refinancing a Bitcoin-backed credit facility to free up cash for the AI buildout.

The AI pivot: $16.8B in data center backlog

Here is the number that re-rated the stock. Hut 8 has signed roughly $16.8 billion in contracted AI data center leases, spread across 597 megawatts of capacity. For a company that was hashing Bitcoin two years ago, that figure is extraordinary, and it is the single best explanation for where HUT stock went.

Beacon Point and River Bend

The backlog comes from two campuses. Beacon Point in Texas carries a roughly $9.8 billion lease across 352 megawatts. River Bend in Louisiana adds about $7.0 billion across 245 megawatts. These are not vague memorandums of understanding. They are long-term contracts with creditworthy, hyperscaler-adjacent tenants, the kind of agreements that throw off predictable cash for years rather than betting on a coin price. River Bend's tenant is FluidStack, an AI cloud provider backed by Google and Anthropic, which tells you who ultimately sits behind the payments. Beacon Point's tenant has not been named beyond its investment-grade rating, so some of that certainty rests on disclosures investors cannot yet fully inspect.

Investment-grade bonds for a crypto-rooted company

The financing is the part that should make you sit up. Hut 8 funded River Bend with $3.25 billion in BBB- rated bonds carrying a 6.192% coupon. That was, by industry accounts, the first investment-grade single-sponsor data center construction bond ever sold. Read that again. A company born in Bitcoin mining, an industry Wall Street treated as junk-tier, borrowed billions at investment-grade rates against AI infrastructure backed by names like Google and Anthropic through its tenant FluidStack. The bond market does not hand out that label lightly, and access to the capital markets at that cost is itself a competitive moat.

Why compute margins dwarf mining

The economics show up fast in the financials. In the first quarter of 2026, Hut 8 generated $71 million in revenue, up 226% year over year. Compute drove $66 million of that, about 93% of the total, at a 67% gross margin. Mining margins, post-halving, are a fraction of that and swing with every move in Bitcoin. When a business can earn 67 cents of gross profit on a dollar of contracted compute revenue, it is no surprise the market repriced the whole company. There is a deeper reason the contracts matter. Mining revenue arrives in Bitcoin, unpredictable and taxable the moment it lands. Compute revenue arrives as multi-year payments from creditworthy tenants, the kind of cash flow a bank will lend against.

HUT stock price and the 560% run

A stock with a beta above 6 and a near-tenfold range in a single year is not a quiet investment. It is a position you have to watch. HUT trades near $112 on Nasdaq in mid-2026, against a 52-week range of $15.26 to $140.80. It hit that all-time high of $140.80 on June 2, 2026, then dropped about 12% in a single session days later. Over the past year the stock is up roughly 560%; year to date it is up around 144%.

| HUT stock key statistics (as of June 2026) | Figure |

|---|---|

| Share price | ~$112 |

| 52-week range | $15.26 - $140.80 |

| Market capitalization | ~$12.6 billion |

| Shares outstanding | ~112.6 million |

| 1-year return | ~+560% |

| Beta | 6.04 |

| Bitcoin held | 10,278 BTC (~$647M) |

| AI lease backlog | ~$16.8 billion (597 MW) |

| Q1 2026 revenue | $71M (+226% YoY) |

| Dividend | None |

The numbers tell a clean story. This is a small share count, a large market cap, an enormous range, and a balance sheet now built around AI contracts rather than coins. With daily trading volume often above 5 million shares and a price-to-sales ratio north of 60, the hut stock valuation is plainly pricing in the future backlog rather than current revenue. The volatility is the price of admission.

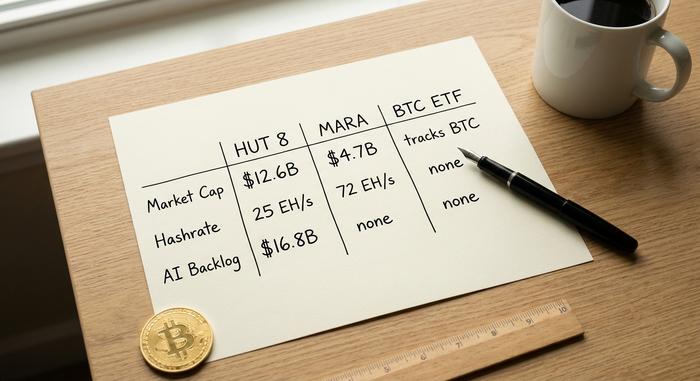

HUT vs other Bitcoin miners (and a Bitcoin ETF)

So why is Hut 8 worth more than its rivals while doing less actual mining? Compare it to Marathon Digital, the largest pure-play miner. Marathon runs about 72.2 exahash of mining power and holds 35,303 BTC, yet carries a market cap near $4.70 billion. Hut 8 mines roughly 25 exahash through its subsidiary and holds far less Bitcoin, yet the market values it at $12.64 billion. The entire 2.7x gap is the AI bet.

| What you are buying | Hut 8 (HUT) | Marathon (MARA) | Spot Bitcoin ETF |

|---|---|---|---|

| Market cap | ~$12.6B | ~$4.7B | Tracks fund size |

| Mining hashrate | ~25 EH/s (via ABTC) | ~72 EH/s | None |

| Bitcoin held | 10,278 BTC | 35,303 BTC | Holds BTC directly |

| AI/data-center upside | Large ($16.8B backlog) | Minimal | None |

| Core exposure | AI infrastructure + BTC | Bitcoin mining | Bitcoin price |

Why HUT commands a premium

Investors are not paying for hashrate; they are paying for contracted AI cash flow that miners simply do not have. Hut 8 is also a genuinely efficient miner where it still mines, with a cash cost near $50,332 per Bitcoin against an industry average around $79,995. The same AI rotation is lifting peers like Riot Platforms, CleanSpark, and Cipher Mining, all racing to convert mining sites into AI capacity. But the premium is not about mining efficiency. It is the data centers.

The ABTC spinoff: isolating the mining bet

In September 2025, Hut 8 carved its mining operations into a separately listed company, American Bitcoin Corp, of which it owns roughly 80%. The move was clever — it quarantines the volatile, post-halving mining economics inside one vehicle while letting the Hut 8 parent carry the cleaner AI valuation. American Bitcoin also brought political visibility, with Eric Trump involved, which cuts both ways: attention and headline risk in the same package. What strikes me about the structure is how deliberately it separates two investor audiences. Crypto traders who want mining exposure can buy American Bitcoin directly, while investors who want the AI infrastructure story can own the Hut 8 parent without the full drag of post-halving mining economics. One company, two very different bets, cleanly split.

HUT vs just buying Bitcoin

If all you want is Bitcoin exposure, none of this helps you. A spot Bitcoin ETF tracks the coin cleanly for a small fee. Buying HUT means buying an AI construction company with a Bitcoin side pocket, a very different bet with execution risk a coin does not carry.

The risks behind the HUT stock rally

The thesis is real, but the price already assumes a lot. The whole premium over other miners is the AI buildout, and that buildout is not finished. Construction across 597 megawatts takes years, and any delay, cost overrun, or tenant dispute would hit the stock hard. The market is paying today for cash that arrives later.

The balance sheet adds pressure. Hut 8 reported a net loss of about $311 million over the trailing twelve months — the earnings picture remains deep in the red — and its Altman Z-Score sits near 1.71, inside the range that signals financial stress. Funding the data centers means more capital, and an active billion-dollar at-the-market program means more shares; today's 112 million share count will likely grow. Bitcoin still matters too, because the company consolidates American Bitcoin, so a crypto crash still bleeds into results, and its all-in mining cost has been estimated near $160,000 per coin once every expense is counted, far above the headline cash cost. Cash on hand sits around $160 million against multi-billion-dollar construction budgets, which is exactly why the share count keeps climbing. And with a beta above 6, none of this happens gently. If the AI story stumbles, the re-rate that lifted HUT can reverse just as fast.

What analysts say about HUT stock

Wall Street likes the story but has mostly already paid for it. The consensus rating is a Strong Buy from around 16 to 17 analysts, with an average price target near $119 and a high of $156 from Jefferies. Notice how tight that is to the current price. Unlike some crypto-linked names where targets sit double or triple the quote, HUT's targets cluster just above it. The plain reading is that analysts think the big re-rating has already happened and the easy money is behind it.

Is HUT stock a buy, or a priced-in bubble?

HUT stock is an AI-infrastructure bet wearing a Bitcoin miner's history. The bull case is unusually concrete for a former crypto stock: $16.8 billion in contracted leases, investment-grade financing, and compute margins that mining could never touch. The bear case is just as clear: a stretched balance sheet, relentless dilution, a beta above 6, and a price that already bakes in years of flawless execution. The question is not whether the AI pivot is real — it plainly is. The question I keep returning to is whether you are buying a builder at the start of its run or paying full price for a story the market has already discovered.