PYPL Stock: Is PayPal Holdings a Value Buy?

Here is a number that should stop any investor cold. PYPL stock trades around $42, almost exactly where PayPal opened on its first day as an independent company back in 2015. A full decade. A run to $310 along the way. And a round trip right back to the starting line. PayPal Holdings was once a market darling worth more than $360 billion; today it is a $36 billion turnaround story trading at a single-digit earnings multiple. The bull case is simple: it has never been this cheap. The bear case is just as simple: cheap and stuck can last a long time. To make it more interesting, the company is now on its second chief executive in 30 months. This guide walks through what PayPal is, how the stock fell so far, the value math, and whether it is a buy or a trap.

What PYPL Stock Is and What PayPal Does

Let us get the basics out of the way. PYPL is the Nasdaq ticker for PayPal Holdings Inc. You have used it. The yellow checkout button, the app that splits a dinner bill, the thing your aunt uses to send birthday money. That is PayPal. The company traces back to 1998 and a founding crew so influential that people still call them the PayPal Mafia: Thiel, Musk, Levchin, and others who went on to build half of Silicon Valley. eBay bought PayPal in 2002, kept it for thirteen years, then finally cut it loose in 2015.

So what is the business today? Payments, at a staggering scale. PayPal moved about $1.79 trillion across its platform in 2025, serving roughly 434 million active accounts. It bought its way bigger along the way: Braintree and Venmo in 2013, Xoom in 2015, the coupon tool Honey for $4 billion in 2020. Run from San Jose, it lets you pay with a bank account, a card, or your stored balance almost anywhere online. None of that sounds like a stock down 85% from its high, does it? And yet here we are. PayPal is mature and cash-rich now, not the rocket it once was, and that single shift is what the whole PYPL stock debate turns on.

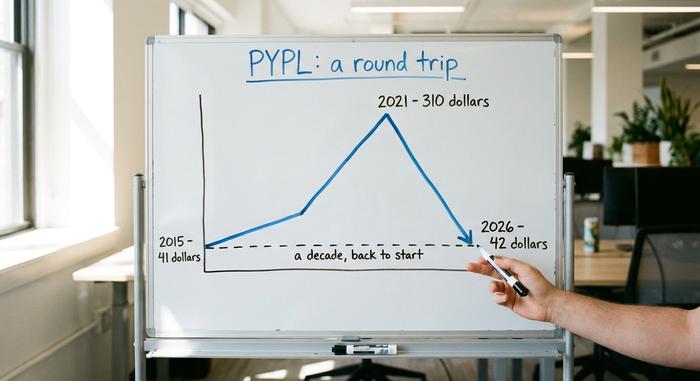

PYPL Stock Price: From $310 to a Lost Decade

The PayPal price chart is a cautionary tale about paying any price for the word "growth." It splits into three clear acts.

The eBay spinoff and the boom

PayPal started trading on its own in July 2015 at around $41.46 a share. For a few years it delivered. Online shopping boomed, the pandemic poured rocket fuel on e-commerce, and PYPL became a darling of growth funds. By July 2021 it touched an all-time high of $310.16. At the top, PayPal was worth more than most banks on the planet.

The collapse

Then the floor gave way. Pandemic spending cooled, interest rates climbed, and the market dumped expensive, slow-growing tech. User growth stalled. Margins wobbled. Rivals crowded in. The real gut-punch landed in early 2022, when PayPal scrapped a flashy goal of 750 million users and cut its guidance, sparking one of the worst single-day drops in its history. Investors finally saw the pandemic surge for what it was, a one-off rather than a new baseline. From peak to trough the stock shed roughly 85%, with one stretch down about 44% in a single year. Growth darling to broken fintech, almost overnight.

Back where it started

Today PYPL's stock quote sits near $42, a market capitalization around $36 billion, down from a peak above $360 billion. Put plainly, the stock has done a full decade-long round trip back to its 2015 debut price. That is a rare and painful thing for a large company, and it is exactly why value investors are now circling.

| Date | Event | Price / level |

|---|---|---|

| Jul 2015 | eBay spinoff debut | About $41.46 |

| Jul 26, 2021 | All-time high | $310.16 |

| 2024-2026 | 52-week range | $38.46 to $79.50 |

| Jun 2026 | Recent price | About $42 |

PayPal Financials and the Value Case

The bull thesis for PYPL stock is mostly arithmetic. A cheap multiple plus aggressive buybacks can compound earnings per share even when revenue barely moves.

Cheap on earnings

Start with the valuation. PayPal trades at roughly 7.7 to 8.7 times earnings, depending on whether you use trailing or forward figures. In its 2025 fiscal year the company reported about $33.2 billion in revenue, up around 4%, with earnings per share near $5.41 and net income around $5 billion. For context, payment peers Visa and Mastercard trade at several times that multiple. The market is pricing PayPal like a declining business, not a profitable one. It is also not a fragile one. PayPal holds roughly $4 billion in net cash, a balance sheet some analysts call bulletproof, and generates about $6 billion in free cash flow a year. In the first quarter of 2026 it earned $8.35 billion in revenue, up 7%, with non-GAAP earnings of $1.34 a share and a return on equity above 25%.

Buybacks and a new dividend

Here is where it gets interesting for a patient investor. PayPal is buying back roughly $6 billion of its own stock a year, retiring close to 8% of all shares in twelve months. Fewer shares means each remaining one owns more of the company. On top of that, management recently initiated a small quarterly dividend of about $0.14, a yield near 1.36%. Add the buybacks and the dividend together and the combined shareholder yield sits around 15% of the market cap. That is a lot of cash coming back to owners.

Transaction margin, the metric that matters

The number to watch is not revenue. It is transaction margin, what PayPal keeps after paying the costs of moving money. Transaction margin dollars reached $15.465 billion in 2025, up about 6%. The catch is that the transaction margin rate slipped to around 45.6% and operating margin fell to roughly 17.8%, a multi-year low. The whole investment case swings on whether those margins stabilize and grow again.

| Metric | Figure (FY2025) |

|---|---|

| Revenue | $33.2B (+4.3%) |

| Earnings per share | ~$5.41 |

| Net income | ~$5B |

| Transaction margin dollars | $15.465B (+6%) |

| Annual buybacks | ~$6B (~8% of shares) |

| P/E ratio | ~7.7-8.7x |

Where PYPL Growth Hides: Venmo and Checkout

The value case only works if growth eventually returns, and that growth has to come from the right place. PayPal's most profitable product is branded checkout, the yellow button you click at online stores. The problem is that branded checkout volume grew only about 1% to 2% recently. That is the soft spot in the entire story. Each active account now runs about 58 transactions a year, so existing users are leaning on PayPal more even as new-user growth has flattened.

Meanwhile PayPal has deliberately walked away from low-margin volume on Braintree, its unbranded processing arm, to protect profitability. Branded checkout earns far more per dollar than the unbranded processing that powers other companies' apps, which is why management cares more about quality of volume than raw size. The bright spot is Venmo, PayPal's mobile peer-to-peer app. It just posted its sixth straight quarter of double-digit payment volume growth, around 14%, and brought in roughly $1.7 billion in revenue, up about 20%. PayPal is also pushing its PYUSD stablecoin, which launched in 2023 and now reaches 70 markets with a supply near $2.85 billion. Venmo and stablecoins are real, but they are still small next to the branded checkout business that has to recover for PYPL stock to earn a higher multiple.

A New PYPL CEO and a $1.5B Cost Cut

Here is the most telling fact about PYPL stock right now. Two CEOs in 30 months. Enrique Lores, who used to run HP, took the job on March 1, 2026. He replaced Alex Chriss, who had only arrived in September 2023. Boards do not reshuffle the corner office that fast when they are happy with how a turnaround is going.

Lores moved quickly. He split the company into three focused units: checkout and PayPal, consumer financial services and Venmo, and merchant payment services and crypto. Then came a $1.5 billion cost-cut, roughly a fifth of the workforce over two to three years, with about 40% of the savings coming from AI automation. Read it one way, it restores operating leverage and profits jump. Read it another, it is churn dressed up as strategy. Both can be true. The optimistic read is that lower costs restore operating leverage and profits jump. The skeptical read is that constant churn at the top is a warning sign, not a fix. Both can be true at once.

Is PYPL Stock a Buy or a Value Trap?

There is no clean answer, so let me lay out both sides and tell you where I land.

The bull case

PayPal is arguably the cheapest large payments company in the world, throwing off around 15% of its market cap a year to shareholders. Even with flat revenue, the buybacks alone can grow earnings per share at a healthy clip. Venmo is accelerating, the second half of 2026 brings easier year-over-year comparisons, and the cost cuts should start showing up in profits. Wall Street's consensus price target sits near $51 as of mid-2026, about 24% above the current price, and the more bullish base cases run to $60 or $66.

The value-trap case

Now the uncomfortable part. Analysts actually forecast earnings to decline slightly over the next few years. Branded checkout, the high-margin engine, is barely growing. Competition is fierce, from Apple Pay to Stripe to Block. The technology overhaul will take years. Management even guided second-quarter earnings down about 9%. That is why most of Wall Street rates PYPL a Hold, not a Buy. They want to see branded checkout reaccelerate before believing. The analyst ratings have barely budged in a year, and investor sentiment swings with every earnings headline in the news flow.

| Bull case | Bear case |

|---|---|

| ~8x earnings, ~15% shareholder yield | Earnings forecast to fall ~1.4% a year |

| Buybacks retire ~8% of shares yearly | Branded checkout growth stuck near 1% |

| Venmo +14% volume, easier 2026 comps | Apple Pay, Stripe, and Block competition |

| Target ~$51, base cases $60-66 | Q2 EPS guided down ~9%, mostly Holds |

Where do I land? The value and the cash returns are real, and I think the buybacks pay you to be patient. But I am not convinced the growth comes back quickly, and a cheap stock that stays cheap for years is the textbook definition of a value trap. This is a position to size carefully, not to bet the farm on.

Key Risks for PYPL Stock Investors

Keep the key risks for PYPL stock in one place. Competition is the big one, with Apple Pay, Stripe, Block, and Shopify all chipping at PayPal's checkout. Branded checkout growth has stalled near 1%. Margins are at multi-year lows and may keep compressing. Execution risk is elevated with a brand-new CEO and a multi-year tech migration. Earnings are forecast to be flat or even fall. European macro softness adds pressure. And because the dividend is tiny, the whole thesis rides on buybacks plus a re-rating that the market has refused to give for years.

The Bottom Line: Is PYPL Stock Cheap?

PYPL stock is genuinely cheap, and it is handing back roughly 15% of its value a year to the people who own it. But cheap and stuck can coexist for a long time, and that is exactly what a value trap feels like from the inside. The buybacks pay you to wait. The open question is whether branded checkout reaccelerates before your patience runs out. So the real decision is less about whether PayPal is cheap, which it clearly is, and more about whether you are buying a genuine turnaround or catching a falling knife. Answer that honestly, then size the position like the bet on management execution that it really is.