How to Transfer Money Between Banks: Fees, Speed & Methods

Last year, US bank customers moved more than $86 trillion through the Automated Clearing House network and another $1.18 quadrillion through Fedwire, in transfers ranging from a $20 birthday gift on Zelle to a six-figure house-closing wire heading to a title company. The numbers are absurd at the top and trivial at the bottom. That is the point. There is no single best way to transfer money between banks. There are six or seven realistic rails, each with its own fees, speed, and risk profile, and the right pick depends on this transfer, not the next one.

This guide covers every realistic method to move money between bank accounts in the United States in 2026, with current fees and timing pulled from primary sources. The deep section explains wires, the rail people understand worst and pay for the most. There is a one-page decision framework so you can pick a method in under a minute. And the last section is the one most articles skip: how to avoid the scams that target this exact category, drawn from the FBI's 2024 fraud report.

Ways to transfer money between banks: methods at a glance

The table below summarises the realistic options. Fees vary by bank and by amount; the figures shown are the 2025 averages from Bankrate's annual survey and the published fee schedules of major US institutions.

| Method | Typical fee | Speed | Best for |

|---|---|---|---|

| Standard ACH (external transfer) | $0 at most banks | 1–3 business days | Recurring, no rush |

| Same-day ACH | $0–10 | Same business day by cutoff | Mid-size, time-sensitive |

| Domestic wire | ~$26 outgoing / $15 incoming | Hours | Large amounts, real estate |

| International wire | ~$44 outgoing average | 1–5 business days | Cross-border, large amount |

| Zelle | $0 | Minutes | P2P up to bank limits |

| RTP / FedNow | $0 for most consumers | Seconds, 24/7/365 | Instant bank-to-bank |

| Venmo / Cash App / PayPal (standard) | $0 | 1–3 business days | Friend payments |

| Venmo / Cash App (instant) | 1.5–1.75% | Minutes | Same-day need, willing to pay |

| Mailed check | Free | 1–5 days plus mail | Vendors, paper trail |

The surprises in this table are real. Free is not always slow: Zelle is free and finishes in minutes. Expensive is not always fast: an international wire takes longer than a Zelle payment and costs $44. The rails newer than 2020 (RTP, FedNow, instant Zelle) have quietly made the 1-3 business days ACH wait feel old, even though ACH still moves more money than anything else. The right way to transfer money from one bank to another depends on which trade-off you can stomach.

ACH external transfer: the workhorse of US bank-to-bank payments

The ACH network processed 33.6 billion on-network payments worth $86.2 trillion in 2024, per Nacha's March 2025 release. Same-Day ACH alone moved $3.23 trillion across 1.2 billion transactions. These are the boring rails that pay your salary, drain your rent, and quietly move money between accounts at different institutions.

The ACH network batches transactions and settles them in cycles throughout the business day. The sender's bank groups outbound credits and debits, sends the batch to Nacha, the receiving bank pulls its share, and the funds appear in the recipient account on the next or same business day depending on the cycle. You need the recipient's routing and account number. No phone, no email.

Setting up an external transfer to another bank is a one-time exercise. Add the routing and account numbers in your primary bank's online banking. Most banks verify the link with two micro-deposits of a few cents that you confirm in 1-3 business days, or instantly via Plaid if your second bank is supported. After verification, every transfer is two taps. Most major banks charge nothing.

Standard timing takes 1-3 business days. Same-Day ACH speeds this up to the same business day by hitting one of three daily windows; many banks charge $0 to $10. The per-transaction limit for Same-Day ACH rose from $1 million to $10 million on March 21, 2025.

Bill Pay through your online banking is mostly ACH under the hood. Electronic payees receive an ACH credit; paper payees get a printed cashier's check mailed by your bank. Direct deposit, the rail your employer uses to pay you, is also ACH. Recurring transfers schedule weekly or monthly automatic transfers between accounts and cost nothing at almost every consumer bank; you can set up recurring transfers in the mobile app or via mobile banking on the web. Bank-to-bank transfers are free at most institutions, which makes ACH the easy way to transfer money from one bank to another.

Reversibility matters here. ACH transfers can be reversed within roughly 24 hours for clear errors under Regulation E, which is one reason banks prefer ACH for consumer rails. Wire transfers are not reversible once received, which is why fraud preys on them. Send money easily through ACH and you keep some recourse; send money through a wire and you do not.

I keep two checking accounts linked across two banks for liquidity and have not paid a fee for a single transfer in three years. The trade-off is the three-day wait, irrelevant if you plan the move 72 hours ahead.

Wire transfers: when paying for speed makes sense

The Fedwire system moved roughly 836,000 transfers per day in 2024 with average daily value of $4.51 trillion, per the Federal Reserve. Annualised that runs above $1 quadrillion. Wires are where the largest sums move, and a wire fee is the price of admission for any transfer that has to settle in hours.

Bankrate's 2025 survey put the average domestic wire fee at $26 outgoing and $15 incoming. Big-bank specifics: Chase charges around $40 for an international wire in US dollars, Bank of America $45, Wells Fargo $25, Citi $35. International wires average $44 outgoing across the industry. The wire fee is only half the story for cross-border transfers, because banks also embed an exchange-rate markup of roughly 3 to 5 percent above the mid-market rate, which on a $10,000 transfer is $300 to $500 of additional cost the bank does not surface as a "fee."

How a wire works: you give your bank the recipient's name, the recipient bank's name and address, a routing number for domestic wires or a SWIFT/BIC code for international, an account number or IBAN where applicable, and the dollar amount. The bank verifies your identity, debits your account, and sends the wire instruction through Fedwire for domestic transfers or SWIFT for international. The receiving institution credits the recipient account within hours. Cutoff times matter: Fedwire historically closes around 5 PM Eastern, with the Federal Reserve moving the system to expanded 22-hour weekday operation in October-November 2025.

Wires make sense when the cost of being late exceeds the fee. Real estate closings live here. So do brokerage funding, large vendor payments with tight deadlines, time-critical international transfers. The non-reversibility cuts both ways: a wire that lands cannot be clawed back, which is exactly why the scams in the final section weaponise wires.

For international transfers under roughly $50,000, services like Wise and Revolut use the mid-market exchange rate plus a transparent 0.4 to 1 percent fee, and clear in a similar timeframe to a traditional SWIFT wire. The savings on a $10,000 international transfer can be $200 to $400 versus a major US bank, money the bank's invisible FX markup keeps when you wire directly. The currency conversion sits where the real cost hides.

Instant bank-to-bank rails: Zelle, RTP and FedNow

The newer payment rails are quietly making 1–3 day ACH look old. Three names matter: Zelle, RTP, and FedNow.

Zelle moved more than $1 trillion in 2024 across 3.6 billion transactions and 151 million users at roughly 2,100 participating banks and credit unions. The Zelle standalone app shut down on April 1, 2025; Zelle now lives only inside participating bank apps, which is where the vast majority of usage was anyway. You send by phone number or email address, and money lands in minutes between enrolled users at participating institutions. Bank-set daily and monthly limits typically range from $500 to $2,500 per day and $5,000 to $20,000 per month, varying by bank and account type.

RTP, the Real-Time Payments network operated by The Clearing House, launched in November 2017 and now reaches approximately 71 percent of US deposit accounts via more than 950 participating financial institutions. The per-transaction limit rose to $10 million on February 9, 2025. Settlement is 24/7/365 in seconds, and transfers are irrevocable once they post: the same hard-to-reverse property as a wire.

FedNow, the Federal Reserve's instant-payment rail, launched July 20, 2023 and reached around 1,500-1,600 participating institutions by the end of 2025. The default per-transaction cap is $500,000, with an optional ceiling raised to $10 million in November 2025. FedNow is not a competitor to RTP; they are sister systems and a bank can integrate either. Most consumer customers reach instant rails through their own bank's app or through Zelle and never see the underlying rail label.

The CFPB v. Zelle saga is worth flagging. The bureau filed a lawsuit on December 20, 2024 alleging that fraud on Zelle had cost consumers more than $870 million across three large banks. The CFPB voluntarily dismissed the suit on March 5, 2025 under new leadership, but the underlying fraud problem did not go away. The fraud section below covers it specifically. To receive money this fast, you give up the cushion of a reversible transfer.

I have never used FedNow directly. My bank uses it under the hood for some Zelle transfers, which is why a payment that took five minutes two years ago now finishes before I close the app on my phone.

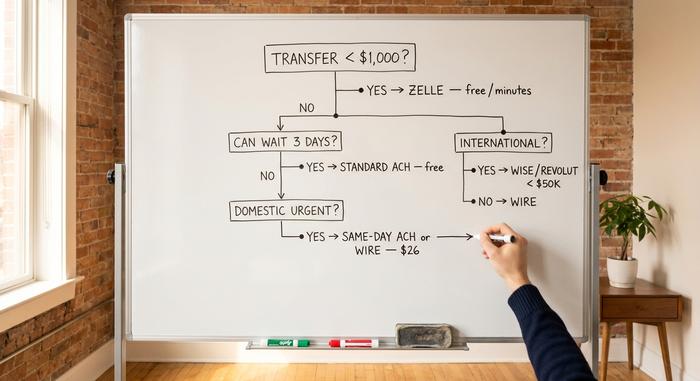

Speed vs cost: a one-page decision framework

Here is a working filter for the next time you are staring at a bank's transfer screen. Three questions and you have your answer.

| Question | If yes... | If no, continue |

|---|---|---|

| Under $1,000 to someone you already trust? | Zelle | — |

| Under $25,000 and you can wait 3 days? | Standard ACH external transfer | — |

| Time-critical AND domestic? | Same-day ACH or domestic wire | — |

| $25,000+ domestic, today? | Wire | — |

| International? | Wise / Revolut for under $50K; wire for larger | — |

Three rules of thumb cover the rest. Free and slow beats fast and expensive for most transfers between your own accounts; you can almost always wait three days when you are moving money around your own name. Wires are for transfers where the cost of being late exceeds the fee. Anything irrevocable, whether a wire, an RTP payment, a FedNow payment, or a Zelle past a few minutes, requires reading the recipient details twice, out loud, with the original instructions in front of you. Times vary by bank, transfers cost only as much as you choose to pay, and choosing right is the whole skill.

How to avoid bank transfer scams

The FBI's Internet Crime Complaint Center reported $16.6 billion in total fraud losses in 2024, up 33 percent year over year, across more than 859,000 complaints. Business email compromise alone accounted for $2.77 billion. Real-estate wire fraud cost victims $173.6 million, with a median individual loss above $70,000. Wires are the preferred vehicle for these losses because they cannot be reversed once delivered.

Real-estate closing fraud works like this. The attacker has compromised the title company's email or the realtor's, watched the closing approach, and on the morning of the wire sends an "updated" set of instructions from a near-identical email address. The instructions list an account number the attacker controls. The buyer wires hundreds of thousands of dollars. By the time the title company calls to ask where the funds are, the money has moved three banks. The defence: every wire instruction, every time, gets verified by voice to a phone number you looked up independently, not the number printed in the email. This rule alone would have prevented most of the $173.6 million.

Business email compromise targets companies the same way. A spoofed "CEO" email asks the CFO for an urgent vendor wire. The fix is a callback policy: any payment over a chosen threshold requires a phone confirmation to a number from the company directory.

Zelle imposter scams use a different script. Someone calls posing as your bank's fraud department, says fraud has been detected, and asks you to "verify" by sending a Zelle payment to a "safe account" they control. Banks are not legally required to reimburse customers for Zelle transfers the customer authorised, even under deception. CFPB guidance in January 2025 strengthened protections for stolen-credential cases, but authorised-but-tricked transfers remain a gray area.

Typo to the wrong account? ACH can sometimes be reversed within 24 hours for clear error. Wires almost never can. Zelle requires the recipient to agree to send the money back, so a typo recipient who refuses keeps the money.

Two practical defences cover most retail risk. Turn on bank alerts for any outgoing transfer above a threshold you choose, where $500 is reasonable. And use a secure email address you control, with a strong password and two-factor authentication, not a shared family inbox, for every banking communication. The closest I have come to losing money in twenty years of banking was a fake title-company update email at a 2022 closing. The phone number printed in the email rang through to an actor who knew the closing details by heart.

The verdict: how to choose a bank-to-bank transfer

Pick the rail before you start to transfer money. Standard ACH for almost everything between your own accounts. Wire when the cost of being late exceeds the fee. Zelle for under $1,000 to people you know. Instant rails when your bank exposes them. Wise or Revolut for international amounts under $50,000. Every wire, every time, voice-verified to a number you looked up yourself, not the one in the email. The mistakes that cost real money are not in picking the wrong rail. They are in skipping verification on the right one.