BlockFi: Crypto Lender Collapse and Distributions

For a few years BlockFi was everywhere. It paid you up to 9% on crypto just for parking it, ran ads on podcasts, and even handed out a Bitcoin rewards credit card. Then it was gone, dragged into bankruptcy in the same week FTX imploded. Here is the strange part most people missed: BlockFi's customers eventually got their money back. Not most of it. All of it, at least on allowed claims. This is the full arc of BlockFi, from the easy-yield boom to the SEC's $100 million slap, the collapse, and the unlikely happy ending that had almost nothing to do with BlockFi being a good business.

What BlockFi Was and How It Paid Crypto Yield

BlockFi was not a bank, though it was very good at looking like one. It offered the surface of banking — earn, borrow, spend — without the regulations that protect depositors. It was a crypto lender, and the difference is the whole story.

From startup to a $3 billion lender

Two founders, Zac Prince and Flori Marquez, started BlockFi in 2017 out of Jersey City. The pitch was simple and seductive. Hand over your Bitcoin or stablecoins, earn interest, borrow against your holdings if you wanted cash without selling. Money poured in. By March 2021 the company had raised a $350 million Series D that valued it at roughly $3 billion, and at its peak it held more than $15 billion in platform assets and served clients across the United States and beyond. The flagship product, the BlockFi Interest Account, had over half a million holders.

It was not only a savings app, either. It lent dollars against your crypto, so you could borrow cash without triggering a taxable sale, and it shipped a Bitcoin rewards credit card that paid cashback in BTC instead of points. The bundle made it feel like a full-service crypto bank, the kind of place where you could store, earn, borrow, and spend in one app. That impression, that it was basically a bank, is exactly what later went so badly wrong.

Where the 9% interest actually came from

So where did that yield come from? Not magic. When you deposited crypto into a BlockFi account, the platform lent it out, to trading firms, to institutions hungry for leverage, at rates higher than what it paid you. The company pocketed the spread. That works beautifully right up until a big borrower stops paying. Your "deposit" was never sitting in a vault with your name on it; it was a loan you made to BlockFi, which then re-lent it. No FDIC, no government backstop. Just counterparty risk dressed up as a savings account.

None of that was hidden, exactly. It lived in the fine print. But the marketing led with the number, and most depositors never asked the obvious follow-up. If the yield is this good, who is paying it, and what are they doing with my coins to afford it? The answer, it turned out, was lending them to some of the most reckless firms in the industry.

The SEC's $100 Million BlockFi Settlement

The first crack was regulatory, and it was loud. On February 14, 2022, BlockFi agreed to pay $100 million to settle charges over the Interest Account, $50 million to the SEC and another $50 million split across 32 US states.

The regulators' point was blunt. The BlockFi Interest Account, they said, was an unregistered security. People were lending BlockFi their crypto in exchange for a promised return, and that arrangement should have been registered and disclosed like any other investment product. It was the first action of its kind against a crypto lender, and it forced BlockFi to stop signing up new US customers for the product. At the time it read like a fine and a speed bump. In hindsight it was a warning label nobody took seriously enough.

The settlement rippled outward, too. It signaled that the SEC saw crypto interest products broadly as securities, and within a year that same logic hit other lenders, most visibly the Gemini Earn program. For existing BlockFi users the immediate effect felt mild, since their accounts kept running. But the legal foundation under the entire yield business had just been declared shaky, in public, by the country's top markets regulator.

How BlockFi Collapsed: 3AC and FTX

BlockFi did not die from one wound. It bled from three, in sequence, and each made the next one worse.

The Three Arrows and FTX dominoes

The first blow came in mid-2022, when the crypto hedge fund Three Arrows Capital blew up. BlockFi had lent it money, and although the firm liquidated the collateral it held, it still absorbed an estimated $80 million loss. That left it wobbling. Enter FTX. In late June, Sam Bankman-Fried's exchange offered a lifeline: first a $250 million term sheet, then a signed deal in early July for a $400 million revolving credit line plus an option to buy BlockFi outright for up to $240 million. For a few months BlockFi looked rescued. The rescue was an illusion. It had just lashed itself to the mast of a sinking ship.

Chapter 11 and the account freeze

When FTX collapsed in November 2022, it took BlockFi with it. BlockFi had deep exposure to FTX and its sister trading firm Alameda, later pegged at roughly $1.247 billion, about $415.9 million tied to FTX and $831.3 million to Alameda. The credit line that was supposed to save it had become a chain. BlockFi froze withdrawals, and on November 28, 2022, it filed for Chapter 11 bankruptcy, listing more than 100,000 creditors. Customers who had been earning 8% a week earlier suddenly could not touch their own coins.

The freeze is the moment the abstraction turned concrete for ordinary users. The balance on the screen had always looked like money in an account. Now it was exposed for what it legally was: an unsecured claim against an insolvent company, locked up until a court decided who got what, and when. People who thought they were saving discovered they had been lending all along.

| Date | Event |

|---|---|

| 2017 | BlockFi founded by Zac Prince and Flori Marquez |

| Mar 2021 | $350M Series D, ~$3B valuation |

| Feb 14, 2022 | $100M SEC and state settlement |

| Jul 2022 | FTX $400M credit line + buyout option |

| Nov 28, 2022 | Chapter 11 filing, withdrawals frozen |

BlockFi Inc Bankruptcy and the Kroll Portal

This is the part former customers actually search for: once the dust settled, how did anyone get paid? The answer ran through bankruptcy court and a claims administrator most people had never heard of.

The case, BlockFi Inc and its affiliated debtors, landed in the United States Bankruptcy Court for the District of New Jersey under case number 22-19361, before Judge Michael Kaplan. To handle the mountain of claims, the court used Kroll as the restructuring and claims administrator. If you had funds on the platform, your path back went through the Kroll distribution portal, where you filed and tracked a claim. The proceeding also drew a sharp line between two kinds of balances. Crypto sitting in a non-interest Wallet account was treated differently from crypto in an Interest Account, because the legal ownership was different. One detail worth burning into memory: the only legitimate contact for the case is through Kroll, at [email protected]. That matters for reasons the next section makes clear.

For most users the experience was bureaucratic and slow. You logged into the portal, confirmed your balances, chose how you wanted to be treated where the plan offered a choice, and then waited. The case ground through court well into 2023, with months stretching between filings and any actual payment, and legal notices arriving in language few non-lawyers could parse. It was nothing like the instant withdrawals the app once promised, and the distance between those two experiences, one tap versus a two-year court process, is the whole lesson in miniature.

Did BlockFi Customers Get Their Money Back?

Now the twist. In July 2024, BlockFi's plan administrator announced that customers would recover 100% of their allowed claims. Full recovery. For a crypto bankruptcy, that is almost unheard of.

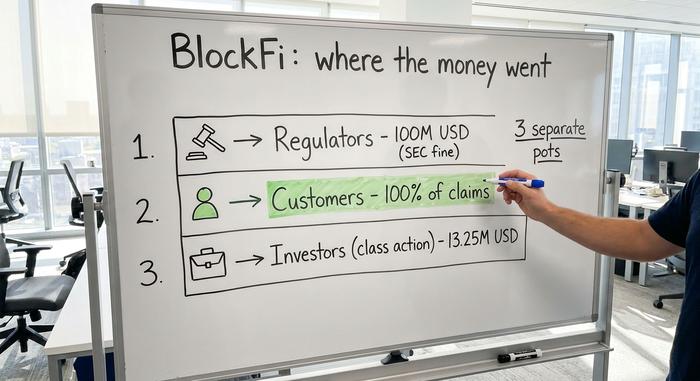

But read why, because the reason is the lesson. The company did not turn out to be secretly solvent. It got lucky on a side bet. As a creditor of FTX, BlockFi held claims against the FTX estate, and as FTX's own recovery improved, those claims became valuable. The administrator sold them on the secondary market at a premium and used the proceeds to make customers whole. A March 2024 settlement pegged BlockFi's claims against FTX and Alameda at $874.5 million. Separately, a dispute over roughly $605.7 million of Robinhood shares, once pledged by Bankman-Fried, was resolved by handing those shares to the FTX estates. There was even a distinct securities class-action settlement, $13.25 million, that won final approval in December 2025 for Interest Account investors. The money came back. It just came back through a maze.

It helps to keep the different pots of money straight, because they are easy to confuse.

| Money track | Amount | Who it was for |

|---|---|---|

| SEC and state settlement | $100 million | Regulators (penalty, Feb 2022) |

| Bankruptcy recovery | 100% of allowed claims | BlockFi customers (from 2024) |

| Securities class action | $13.25 million | Interest Account investors (2025) |

The $100 million fine went to regulators, not to customers. The class-action settlement is a small, separate payout for investors who sued. The big one, the actual return of customer balances, came out of the bankruptcy estate, and it only reached 100% because of that lucky FTX-claims windfall.

BlockFi Scam Warnings After Bankruptcy

A bankruptcy full of anxious people waiting on money is a phishing scammer's dream, and BlockFi's became exactly that. Fake emails and texts dressed up to look like BlockFi or Kroll have been circulating, telling former customers they must "verify" an account or pay a small fee or tax to release a pending distribution. Do not. No legitimate distribution requires you to pay money up front to receive your own funds. If a message creates urgency or asks for a payment, treat it as a scam until proven otherwise. Verify everything through the official Kroll portal, and remember the real contact email address for the case is [email protected]. When in doubt, do nothing and check the source.

Scammers also follow the news cycle. Every time a distribution headline appears, a fresh wave of fake "claim your BlockFi payout" messages tends to follow within days. The timing is deliberate. It is built to catch people right when they are expecting a real payment and most primed to click without thinking twice.

What BlockFi's Failure Teaches Crypto Users

BlockFi was not a freak accident. It was one of three big CeFi lenders to fall in 2022, alongside Celsius and Voyager, and they all broke the same way.

| Lender | Collapsed | Core problem | Customer outcome |

|---|---|---|---|

| BlockFi | Nov 2022 | FTX and Alameda exposure | ~100% of allowed claims |

| Celsius | Jul 2022 | Risky bets, liquidity hole | Partial recovery |

| Voyager | Jul 2022 | Three Arrows default exposure | Partial recovery |

BlockFi's near-full recovery was a rare exception. Celsius and Voyager customers got back only a fraction of what they put in. Same promise, same trap, worse ending.

The common thread is simple. When you earn yield on a centralized platform, you are lending your crypto to someone, and that someone is taking risk with it. The polished app hides a plain fact: a deposit that pays interest is a loan you made, and loans can go bad. There is no deposit insurance behind it. "Not your keys, not your coins" sounds like a slogan, but it is really a description of who legally owns the asset once it leaves your wallet. The practice that quietly amplified the danger was rehypothecation, where the same coins get lent and re-lent down a chain, so one default ripples through everyone. None of this means crypto yield is always a scam. It means the yield is a payment for risk you may not be able to see.

BlockFi's Legacy for Crypto Lending

BlockFi's customers got lucky, not safe, and the distinction is everything. Their near-total recovery hinged on a one-off windfall from selling FTX claims at a premium, not on the lending model working as advertised. Strip out that fluke and the story is a familiar one: a platform promised easy returns, re-lent customer money into a risky market, and could not survive when the market turned. Before you chase the next double-digit yield, on-chain or off, ask the only question that matters. Who is borrowing my coins, and what happens to me if they cannot pay it back?