Three Arrows Capital: How a Crypto Hedge Fund Collapsed

For a while, Three Arrows Capital was the smartest money in crypto. Lenders threw cash at it without asking many questions. Founders Su Zhu and Kyle Davies were treated as oracles, their tweets dissected like scripture. Then, in the space of a few weeks in 2022, the fund went from managing billions to owing about $3.5 billion, and its two founders vanished onto a yacht nobody could locate.

This is the story of how that happened, and why it mattered far beyond one blown-up fund. Three Arrows Capital did not just lose its own money. It took a chunk of the industry down with it, then spent the next three years in a liquidation that is still grinding on. Here is the post-mortem, including the parts the early write-ups could not cover yet.

What Was Three Arrows Capital?

Three Arrows Capital, usually shortened to 3AC, was a Singapore-based crypto hedge fund. Su Zhu and Kyle Davies founded it in 2012. The two had met as teenagers at Phillips Academy, studied at Columbia, and done short stints at Credit Suisse before deciding they could trade better on their own.

They could, for a while. The early 3AC was not a crypto fund at all. It made its money arbitraging emerging-market foreign-exchange derivatives, squeezing fractions of a cent out of mispriced contracts. That worked until around 2017, when banks cut off their access. So they turned to crypto, a market still messy enough to offer the kind of mispricings they liked.

The pivot made them rich on paper. By early 2022 the fund claimed to manage around $10 billion, and Zhu floated an $18 billion figure for its net asset value. A later court filing put assets "in excess of $9 billion" in 2021. The numbers were slippery because nobody really audited them, and that was part of the problem. As a Pte Ltd in Singapore, 3AC operated with the swagger of a giant and the oversight of a startup. The regulator, the Monetary Authority of Singapore, would later reprimand the firm for misleading it about exactly that, including how much money it actually ran. The gap between the swagger and the substance is where the trouble lived.

How Three Arrows Capital Made Its Name

The trade that built the legend was boring on paper. 3AC bought into the Grayscale Bitcoin Trust, or GBTC, back when its shares traded at a premium to the bitcoin they represented. Buy the shares, ride the premium, look brilliant. At one point the fund held close to 39 million GBTC units.

In a rising market, this kind of thing prints money, and 3AC layered leverage on top to print more. The catch is that the GBTC trade only works while the premium lasts. Once those shares flipped to trading at a discount to the bitcoin behind them, the position became a trap: 3AC could not easily redeem the units for the underlying coins, so it was stuck holding a depreciating, illiquid bag.

For a while none of that mattered. The founders went from clever arbitrageurs to loud, directional bulls who were long almost everything and happy to say so. Zhu's "supercycle" thesis, the idea that crypto would simply keep climbing, became a kind of brand. Their reputation became an asset in itself. Because everyone "knew" 3AC was good for it, lenders handed over crypto with little or no collateral. That trust was the real product. It was also the fuse.

The Bets That Broke Three Arrows Capital

Leverage is a wonderful thing right up until the moment it isn't. The same borrowed money that magnified 3AC's wins was waiting to magnify a loss, and in 2022 it got one.

The Luna bet

3AC went big on Terra, the ecosystem built around the LUNA token and its algorithmic stablecoin, UST. The draw was Anchor, a lending protocol dangling a roughly 20% yield on UST deposits, a number that should have read as a warning rather than an invitation. The fund put in somewhere between the $200 million Zhu later admitted to and the roughly $560 million that on-chain sleuths traced. In May 2022 UST lost its dollar peg, LUNA spiraled to near zero in days, and tens of billions in value evaporated across the market in less than a week. 3AC's stake went with it. The fund was also exposed to a depeg in staked ether, or stETH, around the same time, so the pain did not arrive alone. For a fund running on borrowed money, a hit that size was not a setback. It was the end.

Margin calls they couldn't meet

Here is where the borrowing turned lethal. 3AC had pledged assets all over the place to fund its bets, and crucially, it had borrowed from many lenders at once without any of them seeing the full picture. Each lender thought it was dealing with a healthy, diversified fund. None could see that the same collateral and the same story had been recycled across the whole market. As prices cratered in June 2022, lenders issued margin calls, demanding more collateral. 3AC did not have it. Its GBTC shares had flipped to a 34% discount, its Luna was worthless, and the rest was already spoken for. On June 16 the calls started failing, and once one lender realized the fund was insolvent, they all did.

From $18 billion to liquidation

Collapse came fast. On June 27 a court in the British Virgin Islands ordered the fund into liquidation. Days later, on July 2, 3AC filed for Chapter 15 bankruptcy in the United States. The firm Teneo was appointed to pick through the wreckage. A fund that had claimed an $18 billion net worth months earlier was now a legal estate, and its total losses across 2021 and 2022 would later be pegged at more than $4 billion.

The Contagion: Who 3AC Dragged Down

This is the part that turned a fund blowup into an industry crisis. Because 3AC had borrowed unsecured from nearly every major crypto lender, its default did not stay contained. It became their default too.

| Creditor | Exposure to 3AC | What happened next |

|---|---|---|

| Genesis | ~$2.36B (largely undercollateralized) | Froze withdrawals, bankrupt Jan 2023 |

| Voyager Digital | ~$665M (15,250 BTC + $350M USDC) | Bankrupt July 2022 |

| Celsius | Linked exposure | Bankrupt July 2022 |

| BlockFi | Undisclosed loan | Bankrupt Nov 2022 |

| Deribit | ~$51M | Survived, filed a claim |

Total creditor claims came to roughly $3.5 billion across 154 claimants. Voyager, which had lent 3AC about $665 million, collapsed within weeks and froze customer withdrawals, trapping retail users who had no idea their deposits were riding on one hedge fund. Celsius went down the same month. BlockFi limped to a bailout and then bankruptcy. Genesis, the biggest single creditor at roughly $2.36 billion, never recovered; its parent Digital Currency Group absorbed part of the hit, and Genesis filed for bankruptcy in January 2023. Each domino had its own problems, but 3AC is the one that tipped them. For a few months in 2022, the question on every crypto desk was simple and grim: who else lent to Three Arrows? The answer, far too often, was "we did."

Where Are Su Zhu and Kyle Davies Now?

While creditors burned, the founders went quiet, then went missing. They stopped cooperating with liquidators in July 2022 and surfaced only as rumors that Bloomberg and others kept chasing, in Dubai, in Bali, in Bangkok. The liquidators later catalogued what the money had been spent on, and it stung: a $50 million superyacht with the on-brand name "Much Wow," and an NFT-buying side fund called Starry Night that had dropped around $21 million on digital art.

The reckoning, such as it was, came slowly. In September 2023 the Monetary Authority of Singapore banned both men from regulated activity for nine years. That same month Su Zhu was arrested at Singapore's Changi Airport and handed a four-month prison sentence for failing to cooperate with the investigation. Kyle Davies largely stayed out of reach, and the manhunt was always more symbolic than practical: the money was gone, and a few months in a cell was never going to bring it back.

Neither founder exactly went away, and neither showed much contrition. In interviews, Zhu shrugged off the wreckage with lines like asking whether he was supposed to be sorry for a company going bankrupt. They launched OPNX, an exchange for trading the very bankruptcy claims their collapse had helped create, of all things, which shut down in early 2024. Then came an advisory role at a related exchange, OX.FUN, and later a memecoin trading on the 3AC name. The pattern was less redemption arc than rebrand, again and again, on the back of the same notoriety that sank everyone who had trusted them.

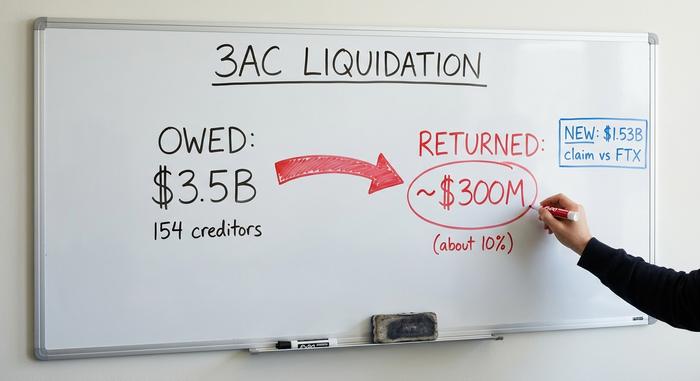

Inside the Three Arrows Capital Liquidation

Three years on, the cleanup is still running, and most of the money is still gone. Teneo's liquidators have been clawing assets back across multiple jurisdictions against that $3.5 billion mountain of claims, and the math remains brutal for anyone who was owed.

| Liquidation figure | Amount |

|---|---|

| Total creditor claims | ~$3.5B (154 creditors) |

| Estimated recovery rate | ~46% of $2.7B admitted claims |

| Actually returned so far (by early 2025) | ~$300M (around 10%) |

| 3AC's approved claim against FTX | ~$1.53B |

| Insolvent-trading claim vs founders | ~$1.08B |

The single biggest twist came from FTX. It turned out FTX had liquidated about $1.53 billion of 3AC's assets in the two weeks before 3AC itself imploded, and in March 2025 a US court approved 3AC's matching $1.53 billion claim against the FTX estate. That sets up a strange spectacle: the estate of one fallen crypto giant fighting for a payout from the estate of another, with ordinary creditors of both waiting at the back of the line. If the claim holds, it could meaningfully lift what 3AC's creditors eventually see. For now, recoveries sit near 10%, with a pool of illiquid tokens still vesting for years to come. Liquidators have also pursued the founders directly, with a roughly $1.08 billion claim over insolvent trading. Slow, partial, and far from over.

What the 3AC Collapse Teaches Crypto

Strip away the yacht and the memes and 3AC is a very old story in new clothes. A fund borrowed heavily against volatile cryptocurrencies, stacked leverage on leverage, and assumed prices only went up. The twist crypto added was trust without paperwork: lenders handed billions to 3AC unsecured because its founders seemed smart and everyone else was doing it. There was no real risk desk, no margin of safety, no one asking how exposed the fund actually was. When one big bet failed, the whole web of borrowing failed at once. The fixes that followed are the obvious ones in hindsight: lenders now lean toward overcollateralized loans, exchanges publish proof-of-reserves, and "trust me" is a harder sell than it was in 2021. TradFi has made these mistakes for centuries and built rules around them. Crypto made the same ones faster, larger, and without the safety nets, then had to relearn why those nets existed.

Why the Three Arrows Capital Story Matters

3AC was not really a fraud in the way FTX was. It was conviction with infinite leverage and no brakes, which in a downturn looks a lot like the same thing. Its real legacy is what it revealed: how tightly the lenders, funds, and exchanges of 2022 were wired together, and how little collateral was holding any of it up. One fund's bad week became a season of bankruptcies because the whole system had quietly agreed to treat 3AC's reputation as if it were money in the bank. The industry has tightened some of that since, mostly because it had to. The open question is whether the lesson sticks the next time a fund looks too smart to question, or whether the only thing that really changes is the name on the yacht.