GMX: The Decentralized Perpetual Exchange in DeFi

Most "decentralized exchanges" just copied the order book onto a blockchain and called it innovation. GMX did the opposite. It threw the order book out entirely and made every trader bet against one shared pool of liquidity, priced by an oracle instead of by buyers and sellers haggling. That single design choice built a perpetuals machine that has cleared more than $328 billion in trading volume. It also, in the summer of 2025, opened a $42 million hole. This piece walks through how GMX actually works, where its yield comes from, what happened in the hack, and how it stacks up now that the competition has caught fire.

What GMX Is and How It Trades Without an Order Book

GMX is a decentralized spot and perpetual exchange. In plain terms, it lets you swap crypto and place leveraged bets on price, directly from your own wallet, with no company holding your funds and no central matching engine deciding your fill.

From Gambit to a multichain perp DEX

The project went live in September 2021 on Arbitrum, an Ethereum layer 2, after rebranding from an earlier protocol called Gambit. It expanded to Avalanche in early 2022, then much later pushed onto Solana and Base in 2025 through a multichain setup built on LayerZero that spans both EVM chains and non-EVM networks. The home base, though, has always been Arbitrum, where most of its liquidity and volume still live.

Oracle pricing and zero price impact

Here is the part that makes GMX different. A normal exchange, centralized or not, matches your buy order against someone else's sell order, and big trades move the price against you. The exchange skips all of that. It pulls prices from Chainlink oracles and fills your trade at that quoted price, straight from the pool. No order book, no matching, and what the protocol calls zero price impact, meaning a large swap does not slip the way it would on a thin order book. The catch, which matters later, is that the pool itself has to absorb whatever position you take.

That trade-off is the whole bargain. You get clean, slippage-free fills, but the system is only ever as honest as its price feed. If the Chainlink oracle is wrong or laggy, the pool prices every trade wrong too, which is one reason GMX V2 later moved to a faster, dedicated low-latency feed.

Perpetual Futures and Leverage on GMX

The headline product is the perpetual future, or "perp." Perpetual futures are crypto derivatives: leveraged bets on price that, unlike a traditional futures contract, never expire. You can hold a long or a short for as long as you keep enough collateral to back it.

Leverage on GMX runs up to roughly 50x, which means $100 of collateral can control a $5,000 position — and that cuts both ways, hard. A small move in your favor is amplified, and so is a small move against you, right up to the point where your collateral is gone and the position is liquidated. To keep things balanced, traders pay a borrowing fee, charged roughly hourly based on how much of the pool their position is using, plus a small fee to open and close. None of this requires an account or a credit check. The pool is the counterparty, and the pool never sleeps.

Why bother with a perp instead of just buying the coin? Leverage and direction. A trader who thinks ETH will fall can short it without borrowing and returning actual ETH, and a trader who wants more exposure than their cash allows can size up. Funding and borrowing fees are the price of that flexibility, and over a long enough hold they add up quietly.

GLP and GM Pools: Being the House on GMX

This is the mechanism everything else hangs on, and most explainers gloss over it. On GMX you are not trading against another trader. You are trading against the liquidity pool. And whoever funds that pool is, quite literally, the house.

GLP: one basket backs every trade

In the original version, GMX V1, the pool is called GLP. It is a single multi-asset basket holding things like ETH, BTC, stablecoins, and a few others. Liquidity providers deposit assets, mint GLP tokens, and in return collect 70% of all the fees the platform generates. There is no impermanent loss in the usual sense, but there is something else: GLP takes the other side of every trader's bet. When traders as a group lose, GLP holders profit. When traders win, GLP holders pay for it. You are earning fees for standing behind the casino table.

In practice that makes GLP returns lumpy. In a quiet, choppy market where traders mostly lose, GLP holders do well. In a strong trending market where leveraged longs all win at once, GLP can bleed. The 70% fee share is the compensation for sitting on that risk, and whether it is worth it depends entirely on how the platform's traders perform against the pool.

GM pools: GMX V2's isolated markets

Version 2 reworked this. Instead of one giant shared basket, it uses GM pools, which are isolated per-market pools, so risk in one market does not bleed into another. V2 also leans on a Chainlink low-latency oracle for faster, more accurate pricing. The shift mattered for safety, and it is why, when V1 was attacked in 2025, V2 came through untouched.

| Feature | GMX V1 (GLP) | GMX V2 (GM) |

|---|---|---|

| Liquidity | One shared multi-asset basket | Isolated per-market pools |

| Oracle | Standard Chainlink feed | Chainlink low-latency feed |

| Risk spread | Shared across all markets | Contained per market |

| 2025 exploit | Drained ~$42M | Unaffected |

GMX Tokenomics and the Real Yield Model

The protocol was one of the early poster children for "real yield," a phrase that got thrown around a lot in 2022. The idea is simple and, for crypto, almost radical: pay people in actual revenue, not in freshly minted tokens.

There are two assets at the center. GLP, covered above, earns 70% of fees. The GMX token earns the other 30%, on top of governance rights. And the fees are paid in ETH on Arbitrum and AVAX on Avalanche — real assets a holder can spend, not more GMX. Stakers also earn esGMX, an escrowed version that vests over time, and multiplier points that reward holding rather than dumping. Supply is capped low, around 13.25 million tokens with roughly 10.42 million circulating, and as of mid-2026 GMX traded near $5.75 for a market cap around $60 million. The honest caveat: real yield is only as real as the trading volume behind it, and when volume dries up, so does the payout. That dynamic is exactly what GMX is living through now. When it was the only serious on-chain perp venue, the fees were fat. As volume scattered to rivals, the same 30% slice of a smaller pie buys a thinner yield, and the token price has followed it down.

| Holder | Share of fees | Paid in |

|---|---|---|

| GLP / GM liquidity providers | 70% | ETH (Arbitrum) / AVAX (Avalanche) |

| GMX stakers | 30% | ETH / AVAX, plus esGMX and points |

GMX TVL, Volume, and Where It Stands

The numbers tell two stories at once, and an honest look needs both. On one hand, GMX is a proven, fee-generating protocol. As of mid-2026 it held about $177 million in total value locked, had cleared roughly $328.5 billion in cumulative perpetual volume, and had generated more than $460 million in lifetime fees across over 720,000 users. Those are not vanity metrics; they are real revenue paid to real liquidity providers.

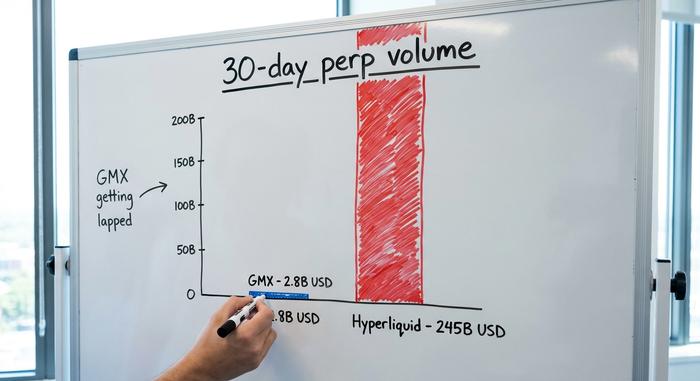

On the other hand, the platform is being lapped. A newer rival, Hyperliquid, went back to an order-book model and now does around $245 billion in 30-day volume, against GMX's roughly $2.8 billion in the same window. That is not a close race anymore. GMX pioneered the on-chain perp; it no longer dominates it.

What pulled the volume away was mostly speed and incentives. Hyperliquid's order book feels like a centralized exchange and ran an aggressive points-and-airdrop campaign, and traders chasing the fastest fills and lowest fees followed. GMX's edge is different now: a battle-tested, pool-based model and a token that pays real fees, rather than the raw volume crown it used to wear.

| Protocol | TVL | 30-day volume | Model |

|---|---|---|---|

| GMX | ~$177M | ~$2.8B | Oracle-priced pool (AMM) |

| Hyperliquid | ~$6B | ~$245B | On-chain order book |

The 2025 GMX Exploit: $42M and a Return

In July 2025 GMX learned the cost of its own design the hard way. The shared-pool model that removes slippage also concentrates risk in one place, and an accounting flaw let an attacker manipulate that place.

How the re-entrancy worked

On July 9, 2025, an attacker hit GMX V1 on Arbitrum with a cross-contract re-entrancy exploit, targeting a flaw buried in the smart contracts governing position accounting. In plain language, they exploited the order in which those contracts updated their books. By manipulating the recorded average price of open short positions, they tricked the system into massively overstating the value of GLP, inflating its price from around $1.45 to roughly $27 mid-transaction. With GLP "worth" almost twenty times its real value, they redeemed it for about $42 million in actual assets and walked away. The team paused V1 trading and minting once the bleeding was spotted.

Why the funds came back

Then something unusual happened. GMX publicly offered the attacker a 10% white-hat bounty to return the rest, no questions asked. Within days, between July 11 and 16, the exploiter sent back roughly $40.5 million and kept about $5 million as the bounty. On-chain money is traceable, laundering large sums is hard, and a clean $5 million beat the risk of getting caught moving $42 million. The V2 system, with its isolated GM pools, was never affected. The episode was, in a strange way, a best-case ending to a worst-case bug.

Security firms that picked apart the incident, including Rekt and CertiK, traced it to the way V1 booked the average price of short positions, a flaw that had sat quietly in the code for years. The team has since steered users toward V2, and the V1 contracts are effectively being wound down. The lesson is uncomfortable but clean: an audit is a snapshot, and old code that has safely held millions for years is not the same thing as safe code.

How to Trade on GMX and Buy GMX Token

Using GMX is more approachable than the mechanics suggest. It comes down to four moves.

First, connect a self-custody wallet such as MetaMask to Arbitrum or Avalanche and bridge in some funds. Second, to trade, open a long or short perpetual: pick your market, set your collateral, choose your leverage, and confirm. Third, to earn instead of trade, provide liquidity by minting GM (or GLP) and collect your share of fees. Fourth, to back the protocol itself, stake the GMX token for the 30% fee cut and esGMX rewards. As for how to buy GMX, you can swap for it directly on GMX or another decentralized exchange like Uniswap, or pick it up on most major centralized exchanges. Just remember that staking and providing liquidity both lock you into the protocol's risks, not just its rewards.

One practical note. Because GMX lives on Arbitrum and Avalanche, fees and gas are cheap compared with Ethereum mainnet, but you still need a little of the native gas token to transact. And every action is final and on-chain, so there is no support desk to reverse a fat-fingered trade or a wrong-network transfer.

Is GMX Worth Using? Risks and the Future

So is GMX worth it? It depends on which seat you take. The product is real and the yield is real, but so are the risks. Smart-contract bugs are not hypothetical here; 2025 proved that. Liquidity providers carry direct exposure to trader profits, leverage can liquidate you in minutes, the whole system leans on oracle accuracy, and the competition is fierce and growing. The future likely rides on V2 and the multichain expansion winning back the volume that drifted to faster rivals. The platform is not dead, but it has to fight for relevance it once owned outright.

What GMX Got Right and What It Got Wrong

GMX proved a genuinely important idea: you can run on-chain perpetual trading that pays for itself with real fees instead of token inflation, and people will use it. That is a real contribution to DeFi, and the 720,000 users and hundreds of millions in fees are the receipts. It also proved the price of its own elegance, because the same shared pool that made trading smooth became a single point of failure the moment an accounting bug appeared. If you take one thing from the GMX story, take this: on this platform you are either the trader or the house — and the clean interface hides the fact that both seats can lose.

The protocol will likely keep running and paying fees for years yet. Whether it ever reclaims the lead it once held is a separate question, and an open one. For now, GMX is a working, honest, and slightly humbled piece of DeFi infrastructure.