Fiduciary Meaning: The Real Fiduciary Definition

Ask ten people what a fiduciary is and most will reach for a synonym — trustee, advisor, "someone you trust" — and miss the only part that matters. The fiduciary meaning is not a feeling. It is a legal status, and it draws a hard line between two kinds of people who handle your money: the ones legally required to put your interests ahead of their own paycheck, and the ones who only have to sell you something "suitable." That line decides who is on the hook when things go wrong. This piece covers what a fiduciary actually is in law and finance, and then where the word goes, and quietly vanishes, once you cross into crypto.

The fiduciary definition: duty of care and loyalty

The fiduciary definition is short, but two words inside it carry the whole weight: care and loyalty. Get those, and the rest of the topic falls into place.

What a fiduciary is

A fiduciary is a person or organization handed authority to act on behalf of someone else, whether a beneficiary, a client, or a principal, and then bound by law to put that person's interest ahead of their own. Cornell's Legal Information Institute says it without hedging: a fiduciary must prioritize the beneficiary's interests above their own. Money or property is almost always involved. A trustee runs a trust, an executor settles an estate, an investment adviser steers a portfolio. What separates this from ordinary good manners is that it is not optional. Break it and you can be sued for it. The obligation lives in a courtroom, not a code of conduct.

The duty of loyalty

Loyalty is the first of the two core duties, and it is blunt: no self-dealing. A fiduciary cannot use your assets, or their power over them, to line their own pockets at your expense. Conflicts of interest will still come up, because they always do. The rule is that the fiduciary has to disclose the conflict, not bury it. An adviser who nudges you into a fund because it quietly pays them a commission has broken the duty of loyalty even if the fund does fine. One question settles most cases: whose interest came first, yours or theirs?

The duty of care

Care is the second duty, and it is about competence rather than honesty. The job has to be done with the skill, diligence, and caution that, in the law's old phrasing, "an ordinarily prudent person" would bring to the same situation. Good intentions do not cover you. A trustee who pours an entire estate into one speculative stock has probably breached the duty of care even if he meant well. Cornell lists a third duty too, obedience, which just means following the terms of the mandate. But care and loyalty are the two that carry the weight.

Who qualifies as a fiduciary: the main roles

Fiduciary is a relationship, not a job title. The same person can owe a fiduciary duty in one setting and none at all in another, which is exactly why the word causes so much confusion. What ties the roles together is structure: someone with legal authority managing money or property on another person's behalf.

The list is broader than most people think. Trustees and executors are the classic cases, managing assets for beneficiaries and heirs who often never see the paperwork. Corporate directors are fiduciaries to shareholders. So is your lawyer, to you. A guardian acts for a ward who cannot act alone, and a registered investment adviser answers to the clients whose portfolios they run. The employer who sets up your 401(k) is, like it or not, a fiduciary to the whole staff for that plan. One job is conspicuously missing from the roll call: the ordinary stockbroker. That absence is where a lot of people quietly get hurt.

| Fiduciary role | Who they serve | What they manage |

|---|---|---|

| Trustee | Trust beneficiaries | Trust assets |

| Executor | Heirs of an estate | The deceased's property |

| Corporate director | Shareholders | The company |

| Registered investment adviser | Clients | Investment portfolios |

| 401(k) plan sponsor | Employees | Retirement plan assets |

| Guardian | A ward | Personal and financial affairs |

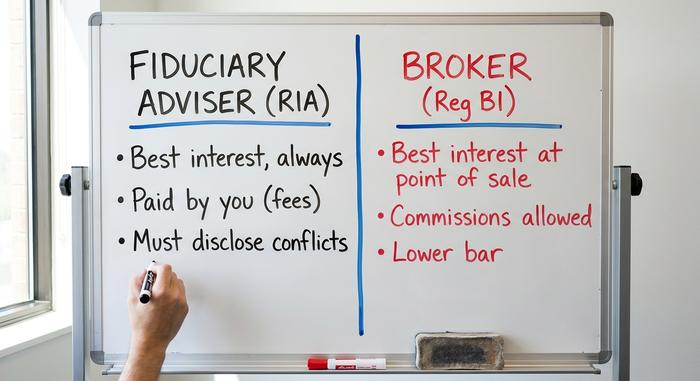

Fiduciary vs suitability: the advisor distinction

Here is the distinction that touches the most wallets, and almost nobody is taught it: the difference between an adviser who is a fiduciary and a broker who is not.

The fiduciary standard

Registered investment advisers are fiduciaries under the Investment Advisers Act of 1940. They must act in the best interest of the client at all times, disclose their conflicts, and generally earn their keep through transparent fees rather than hidden commissions. This is a large slice of the wealth management industry: roughly 16,500 SEC-registered advisers managed about $177 trillion in regulatory assets in 2025, according to the Investment Adviser Association's 2026 snapshot. When they manage your portfolio, the legal obligation runs to you.

The suitability and best-interest standard

Broker-dealers have historically owed a weaker duty. Their old standard was "suitability" — a recommendation had to be suitable, not optimal. Since June 30, 2020, brokers operate under the SEC's Regulation Best Interest, which sounds like a fiduciary duty and is not one. The SEC's own chairman described Reg BI as drawing on "key fiduciary principles" without imposing "the same fiduciary duty" that advisers owe. A broker can still collect commissions and product incentives, so long as the recommendation clears the "best interest" bar at the moment it is made.

The retirement-account gray zone

For retirement money, the line is still being fought over. The Department of Labor has spent a decade trying to drag anyone who advises on a 401(k) or IRA rollover under a fiduciary standard. Its 2016 rule was struck down in 2018. Its 2024 Retirement Security Rule was vacated by a federal court in Texas in March 2026, with a replacement reportedly targeted for later that year. At the rollover layer, in other words, who owes you a fiduciary duty is genuinely unsettled.

| Feature | Fiduciary adviser (RIA) | Broker-dealer |

|---|---|---|

| Legal standard | Fiduciary, at all times | Reg BI "best interest," at point of sale |

| Typical pay | Transparent fees | Commissions, product incentives |

| Conflicts | Must avoid or disclose | Allowed if disclosed and "mitigated" |

| Duty runs | Continuously | Per recommendation |

How fiduciaries get paid and where conflicts hide

Being a fiduciary does not magically erase conflicts of interest. It just changes what you are allowed to do with them. Follow the money. Fee-only advisers are paid only by you, a flat retainer or a slice of assets, and nothing else. Fee-based advisers take your fee and a commission. Commission-only salespeople are paid entirely by the products they can talk you into. Most fiduciary advisory services wrap investment advice and financial planning into one bill, which is fine, as long as you know what you are actually paying for.

Here is the part people miss: even a squeaky-clean fee-only fiduciary has a conflict. An adviser paid a percentage of your assets has a quiet reason to suggest you keep the money invested with them instead of, say, paying off your mortgage. The duty was never to have zero conflicts. That is impossible. The duty is to name the conflict out loud and put your interest first regardless. So ask blunt questions. Are you a fiduciary at all times? How exactly do you get paid? Do you pocket anything for recommending one product over another? I would want those answers in writing, and a real fiduciary hands them over without flinching.

What a breach of fiduciary duty looks like

A breach is what happens when the duty is ignored: self-dealing, hiding a conflict, mismanaging assets, or simply making careless decisions a prudent person would not. The reason the duty means anything is that breaking it carries real consequences, not just disapproval.

A court can order damages, measured as the gap between what the assets are actually worth and what they would be worth had the fiduciary acted prudently. It can also order disgorgement, which means handing back any profit the fiduciary made from the breach, even when the beneficiary suffered no direct loss. Buy trust property cheaply for yourself, flip it later, and the profit is not yours to keep. Regulators can bar the person from the industry, and in the worst cases prosecutors get involved. Trustees get removed, advisers get barred for life, and in the cases that tip into fraud, executives go to prison. That menu of remedies is the entire difference between a fiduciary duty and a pinky promise.

Does a crypto exchange owe you a fiduciary duty?

Crypto borrowed the vocabulary of trust wholesale. Platforms talk about "custody," "holding your assets," "safekeeping." Strip away the language and ask the legal question of whether the company actually owes you a fiduciary duty, and the answer, most of the time, is no.

The default: most platforms owe you nothing like it

When you leave coins on a typical exchange, you usually become an unsecured creditor of that company, not the beneficiary of a fiduciary. Most exchange terms of service explicitly disclaim any fiduciary relationship. The slogan "not your keys, not your coins" is the cultural translation of a legal fact: a custodial exchange is generally a counterparty you are trusting, not a fiduciary bound to you.

The exception: trust-chartered custodians

A few custodians are built on a different legal foundation. Coinbase Custody Trust Company and Gemini Trust Company are New York limited-purpose trust companies, chartered by the state's Department of Financial Services: Coinbase Custody in October 2018, Gemini back in 2015. Under New York banking law, a trust charter carries genuine fiduciary powers; a plain BitLicense does not. Paxos Trust sits in the same category. That one distinction, trust company versus mere licensee, decides whether the firm holding your crypto owes you a fiduciary duty or just a user agreement. The SEC tried to push the whole market toward qualified custodians with a proposed "safeguarding rule" in February 2023, but as of mid-2026 it has not been finalized.

DeFi and DAOs: nobody at the wheel

Decentralized finance makes the question harder still. If "code is law" and no company is in charge, who owes a duty of care? Courts are improvising answers. In 2023 the CFTC won a default judgment against Ooki DAO, with a court accepting that a decentralized autonomous organization can be a "person" liable under the law, and that token holders who voted could be treated as members on the hook. It was not a fiduciary-duty case. It was a warning that "no one is responsible" is not a legal status the system actually recognizes.

FTX and Celsius: fiduciary failure in crypto

The two biggest crypto collapses of the last cycle were fiduciary failures in everything but name. FTX told customers their deposits were their own. They were not. Founder Sam Bankman-Fried was quietly funneling billions to his trading firm, Alameda, the whole time. The Department of Justice put it without euphemism: he stole "over $8 billion" of customer money. In March 2024 he got 25 years and an $11 billion forfeiture order. The estate has since clawed back enough to pay creditors around $10 billion, which sounds like a happy ending until you notice the claims are frozen at November 2022 prices. Anyone who would have held through the next rally still lost, and lost badly.

Celsius ran the same con behind a friendlier face and a yield product. Its founder, Alex Mashinsky, pleaded guilty to fraud and drew 12 years in May 2025; the FTC stamped a $4.7 billion judgment on the company. Roughly that same $4.7 billion in customer assets sat frozen the moment Celsius killed withdrawals in 2022. Not one of these platforms ever used the word fiduciary about itself. That was the whole point.

| Case | What was breached | Outcome |

|---|---|---|

| FTX | Customer funds treated as the founder's own | SBF: 25 years, $11B forfeiture; ~$10B repaid at Nov-2022 values |

| Celsius | Deposits misused; CEL token price manipulated | Mashinsky: 12 years; $4.7B FTC judgment |

How to tell if someone is really your fiduciary

Do not assume — make them say it. For an adviser, ask one question directly: are you a fiduciary, at all times, and will you put that in writing? Check their Form ADV and registration, lean toward fee-only arrangements where the conflicts are smallest, and confirm their advice is built around your financial goals rather than a product shelf. For a crypto platform, look past the word "custody" for an actual trust charter or qualified-custodian status; if the terms of service disclaim a fiduciary duty, believe them. The word costs nothing to use. The legal status behind it is the only thing that protects you.

Why the word fiduciary actually matters

Fiduciary is not a vibe, a marketing badge, or a softer word for "nice." It is a legal obligation with enforceable teeth, and the distance between someone who carries it and someone who merely sounds like they do is exactly where people lose money — in a 401(k) handed to a commissioned broker, and in a wallet handed to an exchange that disclaimed any duty in its fine print. You do not need to memorize the Investment Advisers Act. You need to ask one question before you hand over your money or your coins: are you legally required to put my interest first? Then make them answer in writing.