ACH meaning: Automated Clearing House payments, crypto

Your paycheck, your Netflix bill, your tax refund, and your first crypto buy on a US exchange almost certainly rode the same invisible rail. It is called ACH, short for the Automated Clearing House, and it is the plumbing under most American money movement. In 2025 the network carried 35.19 billion payments worth 93 trillion dollars, according to Nacha, and almost nobody who used it could tell you how it works. An ACH payment is an electronic transfer between US bank accounts, moved in batches rather than one at a time, which is exactly why it is so cheap and so slightly slow. This guide explains what ACH means and how it works, then why it became the default way to fund a crypto account, and where its one real weakness shows up.

What ACH means and how ACH payments work

Start with the name. ACH stands for Automated Clearing House, a nationwide network that transfers funds electronically between US banks, credit unions, and other financial institutions. It is governed by Nacha, the body that writes the rule book, and operated on the back end by the Federal Reserve and a private operator called The Clearing House. The defining word is "clearing." ACH does not move each payment the instant you press send. It collects them, sorts them into batches, and processes those batches in scheduled windows. To send one, a bank needs two numbers: the routing number that identifies the receiving bank, and the account number inside it. That batch design is the reason ACH is nearly free, and the reason it is not instant.

How an ACH transfer actually works

Follow a single payment through the system and the batch logic becomes obvious. You authorise a transfer, and your bank, in ACH terms the originating institution, does not call the other bank directly. It hands your instruction to an ACH operator, either the Federal Reserve or The Clearing House, bundled with thousands of others collected over a few hours. The operator sorts them and passes each one to the receiving bank, which credits or debits the right account. Money settles in scheduled windows, not on demand. This is also where a common confusion lives. ACH is a type of EFT, which simply means electronic funds transfer, the umbrella term for any electronic payment moved between accounts. A wire is an EFT too. So is a debit-card payment. ACH is one specific lane on that road, defined by the batch network and the Nacha rules that run it — not a synonym for every electronic transfer.

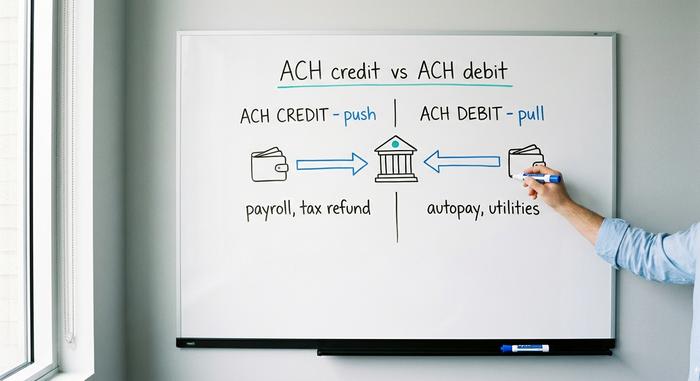

ACH credit vs ACH debit: the two types

Every ACH payment moves in one of two directions, and the direction decides who starts it, who carries the risk, and what it is normally used for.

ACH credit: you push money out

An ACH credit is a push. You, or your bank acting for you, send money into someone else's account. The classic example is direct deposit: an employer pushes wages into thousands of employee accounts at once, which is the single most common thing the ACH network does. Tax refunds, vendor payments, and government benefits are all ACH credits. The sender controls the timing, and the money lands when the batch clears.

ACH debit: someone pulls money in

An ACH debit, sometimes called a direct debit, is a pull, and it runs the other way. You give a company permission, once, to reach into your account and take what you owe. Every recurring payment you have set to autopay, from the gym to the utility to the loan servicer to the streaming service, runs on ACH debit. You authorise it; they initiate it. That convenience is also where the risk lives, because you have handed a third party a standing key to your account. It is the entire reason ACH has strong reversal rules, which matter enormously later.

Direct deposit and payroll

It is worth pausing on payroll, because it is where most people meet ACH without learning the name. When your salary appears on a Friday morning and no paper check ever existed, that is an ACH credit batch your employer submitted a day or two earlier. The same rail replaced the printed paycheck for most of the US workforce, quietly, across a couple of decades. No envelope, no deposit slip, no float, just a file of routing and account numbers settled overnight.

| Type | Direction | Who initiates | Examples |

|---|---|---|---|

| ACH credit | Push | The sender | Payroll, tax refunds, vendor payments |

| ACH debit | Pull | The biller | Autopay bills, utilities, loan payments |

How long does an ACH transfer take

The textbook answer is one to three business days, and for a long time that was the honest one. Standard ACH still settles in that range, held back by batch windows, bank cut-off times, and the hard rule that ACH does not process on weekends or federal holidays. Send one on a Friday afternoon and it may not land until Tuesday. But Same Day ACH, built to fix exactly this, now clears qualifying ACH transactions in one of three daily windows on the same business day. The "ACH takes days" reputation is half out of date — it depends entirely on whether the sender chose the standard or the same-day option.

ACH payment cost and transfer limits

For an ordinary person, ACH is one of the few genuinely free things left in banking. Most consumer ACH transfers, including direct deposit and autopay, cost nothing. Businesses pay a small fee for payment processing on each transaction, usually somewhere between twenty cents and a dollar and a half, which is why merchants like it: a credit card payment can take 1.5% to 3.5% of the sale, while this rail takes pennies. Limits are the more real constraint. The Same Day ACH network caps a single payment at one million dollars, a ceiling in place since March 2022, though Nacha has approved raising it to ten million dollars in September 2027, part of a broader push to let these rails carry bigger sums. On top of the network rule, your own bank sets daily ACH limits for fraud reasons, and those vary widely from one institution to the next. If you have ever hit a wall trying to move a large sum this way, that bank-set cap, not the network rule, is usually the reason.

ACH vs wire transfers and EFT explained

The question almost everyone asks is how ACH differs from a wire transfer, and the honest answer is that they were built for opposite priorities. A wire is fast and final: it moves in near real time, usually settles the same day, and once it is gone it is gone. It also costs real money, commonly twenty-five to thirty-five dollars for a domestic wire, because a different network and often a person stand behind it. ACH is the inverse: cheap, batched, slower, and crucially reversible, since the Nacha rules allow returns. EFT, meanwhile, is neither of these specifically; it is the umbrella term covering both, plus card payments, bank transfers, and more. So when someone asks whether an ACH transfer is the same as an EFT, the answer is that ACH is a kind of EFT, the way a sedan is a kind of car. The table sorts the three.

| Feature | ACH | Wire transfer | EFT |

|---|---|---|---|

| What it is | Batch bank network | Real-time bank-to-bank | Umbrella term |

| Speed | 1-3 days, or same-day | Same day, near-instant | Varies |

| Cost | Free or cents | ~$25-35 domestic | Varies |

| Reversible | Yes, returns allowed | No | Depends |

Same Day ACH, FedNow, and faster rails

The United States spent years with a reputation for slow payments, and it has quietly fixed most of it, though not by speeding up ACH itself. Same Day ACH bolted a faster option onto the existing batch network. Alongside it, two genuinely instant systems now run in parallel: FedNow, the Federal Reserve's real-time rail, which launched in July 2023 and settles around the clock, every day of the year; and RTP, run by The Clearing House, which moved 343 million payments worth 246 billion dollars in 2024. Both recently lifted their per-payment ceilings to ten million dollars. ACH still moves far more total volume than either, but for money that has to arrive right now, the instant rails, not ACH, are the answer.

Buying and withdrawing crypto with ACH

Here is where ACH stops being a banking footnote and starts mattering to anyone who buys crypto. On US exchanges, ACH is the default funding method, and its one weakness, reversibility, shapes the entire experience.

Funding a crypto account by ACH

Link your bank to Coinbase, Kraken, or almost any US exchange, and the cheapest way to add dollars is an ACH transfer. It is usually free, and most exchanges grant instant buying power: you can purchase crypto the moment you start the deposit, before the money has actually settled. That convenience is a small loan the exchange extends to you, betting the ACH transfer will clear. Next to a debit card, which can charge several percent, or a wire, which costs real dollars, ACH is the obvious way to fund an account.

The reversal catch, and why your coins get locked

But ACH cuts both ways. Because an ACH debit can be returned — disputed or reversed for up to 60 days under Nacha and Regulation E rules — the exchange is exposed until that window of risk closes. So it protects itself by holding your withdrawal. Kraken, for instance, states on its support pages that crypto or cash bought with an ACH deposit carries a seven-day withdrawal hold. You own the asset and can trade it; you simply cannot move it off the platform until the hold clears. This is not the exchange being difficult. It is ACH's reversibility working exactly as designed, landing on the one party who cannot reverse a blockchain transaction.

When to use a wire instead

This is why serious or time-sensitive buyers often swallow the wire fee. A wire is final on arrival, so exchanges impose no equivalent hold; the money is unambiguously theirs. For a small recurring buy, the free ACH deposit and its hold are a fair trade. For a large purchase you intend to self-custody quickly, paying twenty-five dollars to skip a seven-day lock can be the cheaper decision in the end.

ACH vs crypto rails and stablecoins

Step back, and ACH and a stablecoin look like photographic negatives of each other. ACH is reversible, batched, business-hours, and US-only; a stablecoin transfer is final, instant, around-the-clock, and global. Each strength is the other's weakness. ACH's reversibility is real consumer protection — if someone drains your account, the rules give you 60 days to claw it back, a backstop no blockchain offers. A stablecoin's finality is the feature that makes it fast and the flaw that makes a mistake permanent. My sense, watching both, is that they are not really competing for the same job. ACH is built for a world where you might need to undo a payment; an on-chain transfer is built for a world where undo does not exist. The table lays the trade-offs side by side.

| ACH | Stablecoin transfer | |

|---|---|---|

| Speed | 1-3 business days | Seconds to minutes |

| Cost | Free or near-free | Network gas fee |

| Hours | Business days only | 24/7 |

| Reach | US bank accounts | Global |

| Reversible | Yes, up to 60 days | No, final |

Conclusion

ACH is the quiet backbone of American money — cheap, batched, reversible, and so ordinary that most people never learn its name even as their salary and their bills ride it every month. That same reversibility is its double identity: it is the consumer protection that lets you reverse a fraudulent debit, and it is the precise reason a crypto exchange holds your coins for a week after you fund with it. When a stablecoin can settle in seconds what this rail settles in days, the thing it still sells is the undo button. So the question worth leaving with is a simple one. How much is being able to take it back actually worth to you?