What Is a Bank Routing Number? Uses, Format, and How to Find It

Every time you set up direct deposit, pay a bill online, or send money to another bank account, a nine-digit code sits quietly behind the transaction. That's the bank routing number — and most people only think about it when someone asks for it and they have no idea where to find it.

A bank routing number identifies the financial institution where your account is held. It tells payment networks which bank to send money to, or pull money from. Without it, electronic transfers don't work.

What Is a Routing Number, Exactly?

Nine digits. That's the whole thing. A routing number is the code that tells the US payment system which bank holds the account you're trying to send money to — or pull money from.

Back in 1910, the American Bankers Association came up with routing numbers to deal with the chaos of sorting paper checks. Every bank got its own code, and processors could bundle checks by destination. The system proved durable enough that it still underpins ACH transfers, wire transfers, and direct deposits well over a century later.

Different names float around for the same thing: routing transit number, ABA routing number, ABA number. They all mean the identical nine-digit code. The terminology depends mostly on which context you're using it in.

About 22,000 routing numbers are active in the US right now. Each belongs to a specific financial institution — a bank, credit union, or savings institution. One important wrinkle: large banks sometimes hold several routing numbers at once. Wells Fargo, for example, assigns different numbers by state depending on where you opened your account.

Both personal checking accounts and savings accounts use routing numbers. The nine-digit code gets money to the right bank. Where it goes inside that bank — your specific account — that's what the account number is for.

Routing Number vs. Account Number

These two numbers always come up together, and people mix them up constantly. They serve completely different purposes.

The routing number identifies the bank. The account number identifies your specific account at that bank. It's like a street address: the routing number is the city and zip code, the account number is the house number and street.

| Routing Number | Account Number | |

|---|---|---|

| What it identifies | The bank or financial institution | Your individual account |

| Length | Always 9 digits | Typically 10–12 digits (varies by bank) |

| Privacy | Public information | Private — keep it secure |

| Same for all customers? | Yes (at the same bank/region) | No — unique to each account |

| Where it appears | Bottom-left of a check | Middle section of a check |

| Used for | Directing funds to the right bank | Directing funds to the right account |

A bank routing number is public — banks post them on their websites, and the ABA maintains a free lookup database. Routing numbers are not sensitive information.

Your account number is another matter entirely. Anyone who has both numbers has enough to initiate debits from your checking account. Share your bank routing number freely when asked. Guard your account number like a password.

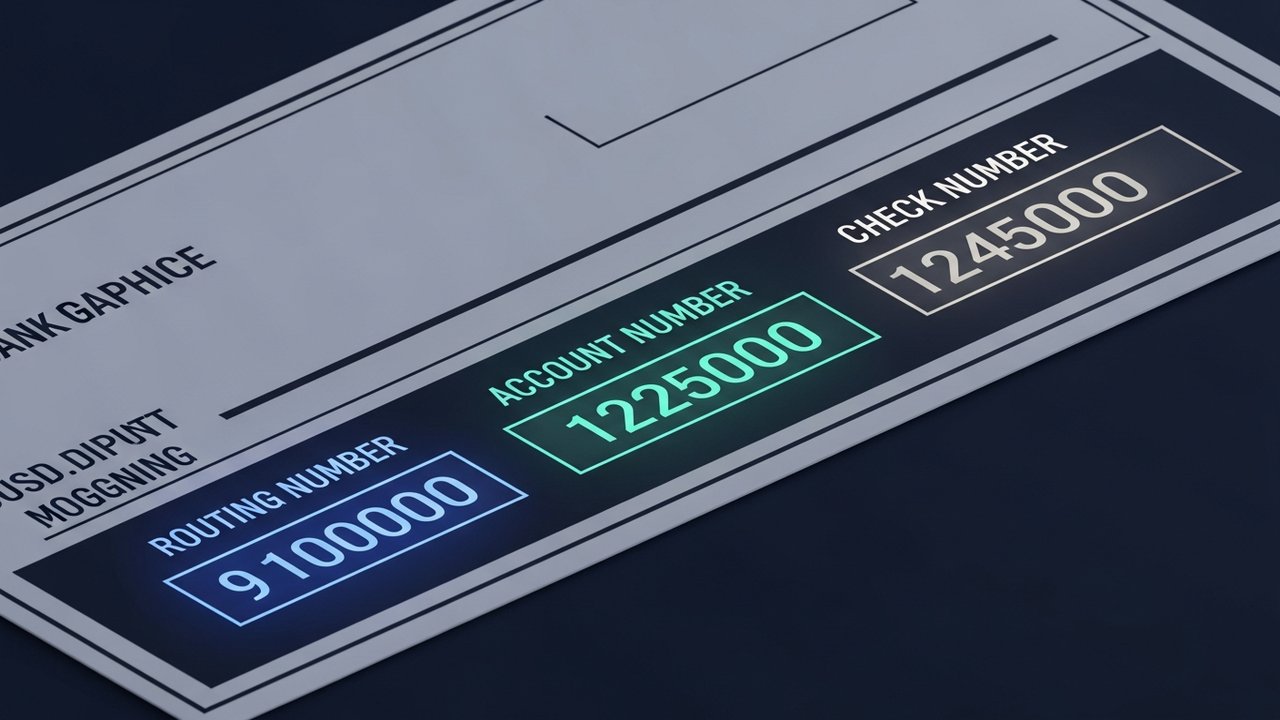

Where Is the Routing Number on a Check?

The bottom edge of a personal check has a row of numbers printed in that slightly blocky, magnetic-ink font — the MICR line. MICR stands for Magnetic Ink Character Recognition, and the whole point is that automated processing machines can read it at high speed without any human involvement.

Reading left to right across that line:

- Routing number — the first nine digits on the bottom-left, enclosed by two transit symbols (⑆)

- Account number — follows the routing number, typically 10–12 digits

- Check number — the final set, matching the printed number in the top-right corner of the check

Worth knowing: the ⑆ symbols bracketing the routing number are MICR delimiter characters, not digits. Don't include them when you're copying the number somewhere.

Most people haven't written a paper check in years. But the MICR line remains useful precisely because everything sits in a fixed, predictable order — unlike hunting through bank app menus trying to remember which submenu hides the routing number.

How to Find Your Routing Number Without a Check

You don't need a checkbook. Here are the most reliable ways to look it up:

- Online banking — log in, navigate to account details, and look for "routing number" or "ABA number"; most major US banks display it in the account summary

- Mobile app — open your bank's mobile app, tap the account, find routing number under account details or settings; usually the fastest option

- Bank's public website — many banks list routing numbers right on their homepage or in the help center, because they're public information

- Paper statement — monthly or quarterly statements print both the routing number and account number on the document

- Bank customer service — call the number on the back of your debit card and ask directly

- ABA routing number lookup — the American Bankers Association runs a free public database at routingnumbers.aba.com, searchable by bank name or location

If your bank has multiple routing numbers (Wells Fargo and Chase both do), verify which one applies to your specific account. The number can depend on the state where you opened the account, not where you live now. Online banking and mobile apps typically show the right routing number for your account, making them the most reliable starting point.

What Is a Routing Number Used For?

Routing numbers are involved in nearly every electronic transaction that moves money between US banks. The main use cases:

- Direct deposit — employers, the IRS, and government agencies use your routing number and account number to deposit funds directly into your checking account or savings account

- ACH transfers — when you pay a utility bill online, send money via Zelle, or move funds between linked accounts, the ACH network routes those transactions using bank routing numbers

- Wire transfers — larger or time-sensitive domestic transfers go through the Fedwire system using routing numbers; check our guide on wire transfer limits for details on fees and amounts

- Autopay and bill payment — mortgage payments, subscription services, and loan repayments set up via bank account all require a routing number

- Linking external accounts — brokerage accounts, investment apps, and savings platforms need your routing number to connect to your bank

- Tax refunds — the IRS needs routing number plus account number to send refunds by direct deposit

Any transaction routed through the US banking system needs that nine-digit identifier to find the right financial institution.

ABA Routing Number vs. ACH Routing Number

For most banks, the routing number is the same whether you're doing an ACH transfer or a wire. But not always.

Some large banks — Chase and Wells Fargo are the common examples — use different routing numbers depending on the transaction type. The ABA routing number runs wire transfers via Fedwire. A separate ACH routing number handles standard electronic transfers. Using the wrong one doesn't always kill a transaction, but it can slow things down considerably.

ACH transfers settle in one to three business days, processed in batches overnight. That's why a payment sometimes shows as pending the next morning. For more on why that happens, see how bank transactions are processed. Wire transfers move through Fedwire, settle same-day if sent before cutoff, and usually cost $15–$30.

The routing transit number printed on a check is typically the ACH routing number. For wire transfers, search your bank's website for "wire transfer routing number" — it may match or differ.

When setting up a payment, ask specifically whether they need an ACH routing number or a wire routing number. Most everyday transactions — direct deposit, bill pay, online transfers — run on ACH.

US Routing Numbers vs. International Payment Codes

ABA routing numbers are a US-only system. Send or receive money internationally and different codes take over.

| System | Where It's Used | Format | Purpose |

|---|---|---|---|

| ABA Routing Number | United States only | 9 digits | Identifies US bank for domestic transfers |

| SWIFT / BIC Code | International (190+ countries) | 8–11 characters | Identifies a bank globally for international wires |

| IBAN | Europe and many other countries | Up to 34 alphanumeric characters | Full account identifier for international transfers |

| SORT Code | United Kingdom | 6 digits (XX-XX-XX) | Identifies UK bank branches |

For international wire transfers into a US bank account, the sending bank typically needs your ABA routing number, your account number, and the bank's SWIFT code. The routing number gets money to the right US institution; the SWIFT code handles the international leg.

Freelancers and businesses receiving cross-border payments run into the limits of the routing number system quickly. Payments that bypass US banks entirely — cryptocurrency, for instance — skip routing numbers altogether. A crypto payment gateway handles those flows outside traditional banking infrastructure, which is why cross-border crypto payments can settle faster with fewer intermediaries.