SEPA payments: euro transfers and crypto on-ramps

For roughly 400 million people, sending euros from one country to another has quietly stopped being a "transfer" at all. Pay a supplier in Lisbon from a Berlin account and it costs the same as paying someone across town, clears about as fast, and uses the same account number format. That sameness is the entire point of the Single Euro Payments Area, or SEPA. A SEPA payment is just a euro bank transfer that follows one shared rulebook across the continent. And because it made euros so cheap and dull to move, SEPA also became the default way Europeans fund and cash out their crypto. This guide covers how SEPA payments work, then where they meet the blockchain.

What is SEPA and how SEPA payments work

SEPA is not a bank, an app, or a company. It is a set of rules. The Single Euro Payments Area is an arrangement, run by the European Payments Council, that requires banks and payment service providers across the region to handle euro transfers the same way, whether the money crosses a border or stays put. The practical effect is that you need only one piece of information to pay anyone in the zone: their IBAN, the international bank account number that replaced dozens of national account formats. As of the European Payments Council's December 2025 list, SEPA covers 41 countries and territories. Within that area a euro is a euro — and the bank on the other end is obliged to treat your payment like a domestic transfer.

How a SEPA transfer works step by step

Behind that simplicity sits a short chain. You give your bank, or any payment service provider, the payee's IBAN and an amount in euro. Your provider debits your account and passes the transaction into a SEPA clearing system, which routes it to the recipient's provider, which credits their account. No correspondent banks, no string of intermediaries each taking a cut, no currency conversion. That last part matters more than it sounds. A SWIFT wire abroad can pass through two or three banks, each adding a fee and a day. A SEPA transfer is a single hop inside one harmonised system, which is precisely why it is cheaper and more predictable. You will occasionally be asked for a BIC, the bank identifier code, but for payments inside the area the IBAN alone is now enough. The standardisation is the product — the speed and the low cost simply follow from it.

The three SEPA payment schemes explained

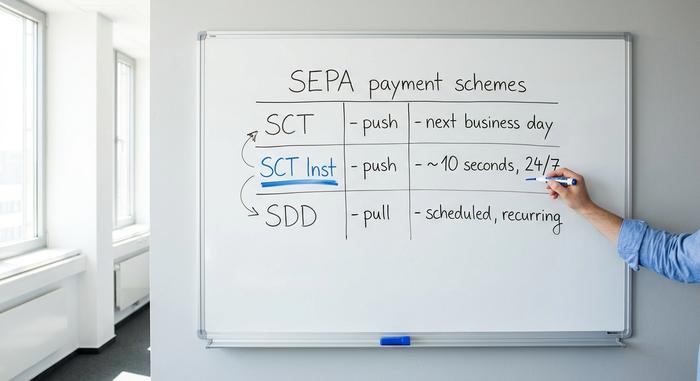

Here is where people get tripped up. "SEPA" is not one payment type but three, and the differences decide how fast your money moves and whether someone can pull it automatically.

SEPA Credit Transfer (SCT)

The workhorse. An SCT is a push payment: you instruct your bank to send a set amount to an IBAN, once. It is what most people mean by a "SEPA transfer." Standard credit transfers settle by the next business day at the latest, and often the same day if you send before your bank's cut-off. Salaries, invoices, one-off payments to a friend all run on SCT.

SEPA Instant Credit Transfer (SCT Inst)

The upgrade. SCT Inst moves money in about ten seconds, any hour, any day, weekends and holidays included. There is no batch window to wait for. For years it was an optional premium some banks charged extra for or skipped entirely. That is changing by law. Under the EU's Instant Payments Regulation, euro-area banks have had to be able to receive instant payments since 9 January 2025 and to send them since 9 October 2025, and they cannot charge more for an instant transfer than for a standard one. Adoption has followed: instant credit transfers reached 23% of euro-area credit-transfer volume in the first half of 2025, up from 16% six months earlier, according to the European Central Bank.

SEPA Direct Debit (SDD)

The opposite direction. A direct debit is a pull payment: you authorise a company to collect from your account, and it initiates the transfers. This is how recurring payments such as subscriptions, utilities, gym memberships, and insurance premiums get collected across Europe. SDD comes in two flavours, Core for consumers and B2B for business-to-business, the difference being how refunds and authorisations are handled. A credit transfer is you paying out; a direct debit is you letting someone pull, with rules to protect you if they overreach.

How long does a SEPA transfer take

The honest answer is "ten seconds or one business day," and which one depends entirely on the scheme your bank used. An instant transfer lands in roughly ten seconds, around the clock. A standard credit transfer is guaranteed within one business day, though weekends, holidays, and a bank's daily cut-off can stretch the calendar even when the working time is short. Send a standard SEPA payment on Friday evening and it may not appear until Monday. The same payment sent as an instant transfer would arrive before you locked your phone.

How much SEPA payments cost and the limits

Inside the euro area, a cross-border SEPA payment is not allowed to cost more than a domestic one. That is not a courtesy; it is written into EU law, specifically Regulation (EU) 2021/1230. For most consumers it means standard transfers are free or close to it. The old instant-payment loophole, where banks charged a premium for SCT Inst, is being closed by the same Instant Payments Regulation that mandated the service: instant can no longer cost more than standard. Limits are a separate question — and a more bank-specific one. SEPA itself no longer imposes a low ceiling on instant transfers; the old €100,000 cap on SCT Inst was lifted in October 2025 and replaced with a figure so high it is effectively no limit at all. What remains are the limits your own bank sets for fraud and risk reasons, which vary widely and can usually be raised on request. The table below sorts the three schemes by speed and direction.

| Scheme | Direction | Speed | Best for |

|---|---|---|---|

| SEPA Credit Transfer (SCT) | Push | By next business day | One-off payments, salaries |

| SEPA Instant (SCT Inst) | Push | ~10 seconds, 24/7 | Urgent, real-time payments |

| SEPA Direct Debit (SDD) | Pull | Scheduled | Subscriptions, recurring bills |

SEPA countries and the SEPA area

A common misconception is that SEPA equals the eurozone. It does not. The area is wider than the countries that use the euro and wider than the EU itself. The European Payments Council's current list runs to 41 countries and territories. It includes all 27 European Union member states, the three EEA countries of Iceland, Liechtenstein, and Norway, and a set of non-EU participants such as the United Kingdom, Switzerland, Monaco, San Marino, Andorra, and the Vatican. Several European countries that do not use the euro still belong to SEPA; they simply send and receive euro-denominated payments. The currency, not the political map, defines the scheme.

SEPA vs SWIFT vs ACH: key differences

Three systems get confused constantly, because they all move money between accounts. They are not really competitors so much as tools for different maps. SEPA is euro-only and covers one defined region, cheap and fast by design. SWIFT is not a payment rail at all; it is a global messaging network for cross-border payments that lets banks in different countries instruct each other to move almost any currency. That reach is both its strength and its weakness — a SWIFT transfer can go anywhere, but it often passes through correspondent banks, picks up fees, and takes one to five days. ACH is the United States' domestic batch system for dollars, the rough American equivalent of a standard SEPA credit transfer. So the choice is simple once you frame it by geography and currency: euros inside Europe, use SEPA; dollars inside the US, ACH; anything leaving those borders or in another currency, SWIFT.

| Feature | SEPA | SWIFT | ACH |

|---|---|---|---|

| Region | 41 SEPA countries | Global | United States |

| Currency | Euro | Almost any | US dollar |

| Speed | 10 sec to 1 day | 1-5 days | 1-3 days |

| Typical cost | Free or cents | Higher, layered fees | Low |

| Best for | Euro within Europe | Cross-border, other currencies | USD within the US |

Buying and withdrawing crypto with SEPA

None of the SEPA guides written by banks mention this, but it is where the scheme matters most to a crypto user. Over the past decade SEPA quietly became the default euro rail of European crypto, the cheapest and fastest way to get fiat onto an exchange and back out again.

Funding an exchange by SEPA

Almost every exchange serving European customers, Kraken, Bitstamp, Coinbase, and the rest, lists a SEPA bank transfer as the primary way to deposit euro. You send an ordinary SEPA payment from your bank to the exchange's account, add the reference they give you, and the balance appears in your fiat wallet. From there you buy crypto. It is the same SCT or instant transfer described above, pointed at an exchange instead of a friend. The one practical catch is the reference: exchanges match your deposit to your account using a code you have to include, and the name on your bank account usually has to match your verified exchange profile, or the transfer gets bounced back to you.

The fees and timing that make it the default

This is the part card payments cannot match. SEPA deposits are usually free, and withdrawals cost a flat few cents. On Kraken, a euro transfer costs nothing to deposit and around nine cents to withdraw; Bitstamp deposits are free with a small fixed withdrawal fee. Compare that to a debit-card purchase, where the processor commonly takes 1.5% to 4%. On a 1,000-euro buy, the card route can cost twenty or thirty euro that the SEPA route does not. Timing has improved too: where SEPA deposits once meant a one-day wait, banks and exchanges that support instant transfers now credit euro in seconds.

Why euro users reach for SEPA over a card

Lower fees are only half of it. SEPA transfers also carry far higher limits than cards, which suits anyone moving meaningful size, and they run directly bank-to-bank, with no card network in the middle to decline a "high-risk" crypto merchant. For a European buying or cashing out regularly, the bank transfer is the cheap, high-limit default, and card payments are the expensive convenience.

SEPA Instant vs stablecoins explained

Here is the irony worth sitting with. Instant SEPA now does, for euros, almost exactly what a stablecoin promised to do: move value in about ten seconds, at any hour, for no meaningful fee. A few years ago that was crypto's pitch against the banks — and, to my mild surprise, they more or less caught up inside the euro area once regulation pushed them. So what is left for a euro stablecoin such as EURC? Three things, mainly. It settles globally, not just across 41 SEPA countries. It runs on rails that never close for a holiday weekend in any jurisdiction. And it is programmable: it plugs into smart contracts, DeFi, and on-chain apps that a bank transfer cannot touch. Instant SEPA wins on simplicity and consumer protection for everyday euro payments; stablecoins win where the money has to cross outside Europe or slot into code. Under the EU's MiCA rules, regulated euro stablecoins are now a defined category rather than a grey area, which sharpens the competition rather than settling it.

| SEPA Instant | Euro stablecoin (e.g. EURC) | |

|---|---|---|

| Speed | ~10 seconds | Seconds to minutes |

| Cost | Free or negligible | Network gas fee |

| Hours | 24/7 | 24/7 |

| Reach | 41 SEPA countries | Global |

| Programmable | No | Yes (DeFi, smart contracts) |

Conclusion

SEPA turned cross-border euro transfers into a non-event, and in doing so handed European crypto its cheapest bridge to fiat. The same standardisation that lets you pay a stranger in another country for free is what lets you fund an exchange for nine cents. Instant payments have now blurred the old line between a bank transfer and a stablecoin to the point where, for euros inside Europe, it is genuinely hard to say what the on-chain version is competing on. That is the question worth carrying out of here. When your euros already move in ten seconds for nothing, what is the blockchain actually offering you that your bank does not?