Thruster Finance: The Blast-Native DEX and Thruster V3

For a few months in 2024, Thruster Finance was the busiest thing on one of crypto's loudest new chains. Today it trades a sliver of its old volume, and its token sits more than 95% below its high. That gap between the hype and the present is the most useful thing about it. Thruster Finance is the native decentralized exchange of the Blast layer-2 network, and its short life so far is a clean case study in what happens when liquidity is rented with rewards instead of earned with usage. This review covers what the protocol actually does, how its V3 engine works, what the THRUST token is for, and why the numbers look the way they do in 2026.

What is Thruster Finance, the Blast-native DEX

Thruster is an automated market maker (AMM) built specifically for Blast, an Ethereum layer-2 chain launched in 2024 by the team behind the Blur NFT marketplace. Calling it "blast-native" is not marketing. Thruster was seeded by Blast's own incentive program and positioned as the chain's flagship DEX from day one, the place where most early trading and liquidity were meant to live.

The core job is the same as any decentralized exchange: let users swap between cryptocurrencies without an order book or a custodian, with each trade settling as an on-chain transaction on a layer 2 network. You trade against a pool of assets rather than a counterparty, and an algorithm sets the price based on the ratio of tokens in the pool. What set Thruster apart was the chain underneath it. Blast pays native yield on idle ETH and its USDB stablecoin, so capital parked in a Thruster pool could, in theory, earn on three fronts at once. That single design choice shaped everything about how the protocol grew, and how it shrank.

Blast itself arrived with unusual fanfare. It was built by Pacman, the pseudonymous founder of the Blur NFT marketplace, and launched with a points-and-airdrop campaign that locked up billions of dollars in deposits before the blockchain even opened to developers. Native yield was the headline feature: rather than letting ETH and stablecoins sit idle, Blast routed them into staking and treasury-bill DeFi protocols and passed the return back to users automatically. For a moment, the Blast ecosystem looked like the fastest-growing corner of decentralized finance (DeFi). Thruster was designed to plug straight into that machinery, which is why so much of the early Blast liquidity flowed through it rather than through a generic exchange ported over from another chain.

How Thruster V3 works: a concentrated liquidity DEX

Thruster Finance ships two AMM designs side by side, and the difference matters more than it sounds.

Constant-product pools versus concentrated liquidity

The classic model is the constant-product formula, x times y equals k, the same math Uniswap V2 popularized. Liquidity sits spread evenly across every possible price, which is simple and reliable but wastes most of the capital, since trades almost always happen near the current price. Thruster V3 is the concentrated-liquidity version, modeled on Uniswap V3. Here a liquidity provider chooses a price range and concentrates their funds inside it. Inside that band, the same money does far more work, so fees per dollar deposited can be much higher. The trade-off is active management: if the price leaves your range, your position stops earning and sits fully in the weaker asset.

In practice this splits liquidity providers into two camps. Passive providers tend to prefer the constant-product pools, where a single deposit keeps working across the whole price curve without any maintenance. More active providers use V3 ranges to chase higher fee income, rebalancing as the market moves. Keeping both models live let Thruster serve both crowds from the same interface, which mattered when it was trying to be the one venue everyone on Blast used.

The triple-yield model

This is the pitch that pulled capital in. On most chains, a liquidity provider earns one thing: trading fees. On Blast, a Thruster position could stack three. Trading fees from swaps, Blast's native yield auto-accruing on the underlying ETH and USDB, and THRUST token incentives directed at that pool. For a while the combined number looked irresistible, and the market behaved accordingly.

Thruster Spaceport, the token launch hub

Thruster also runs Spaceport, a fair launch platform for new Blast-native tokens. New projects could bootstrap a market and initial liquidity on Thruster directly, which let teams explore distribution while keeping fresh trading pairs flowing into the exchange, and tied the protocol's fortunes even more tightly to Blast's own deal flow.

The THRUST token and veTHRUST governance model

THRUST is the Thruster Finance governance and incentive token, and its design borrows directly from Curve's playbook. Holders lock THRUST to receive veTHRUST, and that vote-locked balance decides which liquidity pools receive emissions through a gauge system. In plain terms: lock the token, vote on where the rewards go, and ideally point them at pools you benefit from. It is an elegant flywheel when a protocol is growing and an unforgiving one when it is not, because emissions keep diluting holders whether or not new users arrive.

The launch leaned heavily on that flywheel. Thruster announced a roughly $35 million THRUST airdrop aimed at the users and liquidity providers who had carried it through the Blast points phase, and a gauge-and-bribe market grew up around the emissions, where projects could effectively pay veTHRUST holders to steer rewards toward their pools. The model works as long as fresh demand keeps arriving to absorb the new supply. When it stops, the same mechanism that bootstrapped the exchange becomes a slow leak.

The supply math is the part worth slowing down for, because it explains the persistent downward pressure on price.

| THRUST token snapshot (June 2026) | Figure |

|---|---|

| Price | ~$0.0061 |

| Market cap | ~$953K |

| Fully diluted valuation | ~$3.07M |

| Total supply | 500,000,000 |

| Circulating supply | 155.4M (31.1%) |

| All-time high | ~$0.2221 |

Two numbers there should stop you. The fully diluted valuation is below the $7.5 million the team raised in its seed round. And only about 31% of supply is circulating, which means roughly 40% of the total is still waiting to be emitted through gauges. That is a steady stream of new tokens hitting a market that is no longer growing.

Thruster by the numbers: TVL and trading volume

Here is where the Thruster Finance review earns its title, because the on-chain statistics tell a story competitors mostly skip.

The rise, riding the Blast points mania

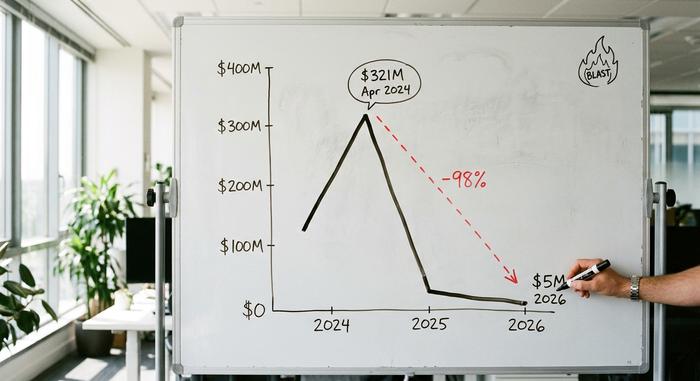

In early 2024, Blast ran an aggressive points campaign, and Thruster was the main venue to farm it. At its peak in April 2024, Thruster's total value locked (TVL) reached about $321 million, according to on-chain analytics, and it became the largest dApp on the chain. Cumulative trading volume across its V3 pools has since passed $8.78 billion, which shows the activity was no illusion while it lasted.

The capital behind it was serious too. In April 2024, Thruster raised a $7.5 million seed round led by Pantera Capital at a $70 million valuation, with OKX Ventures, ParaFi, and Mirana Ventures among the backers, and was described at the time as the largest dApp on Blast. For a project a few weeks old, that was a strong vote of confidence.

The fade, after the airdrop

Then the rewards ended, and the liquidity left. By June 2026, Thruster's combined V2 and V3 TVL had fallen to roughly $5 million, per DeFiLlama, a decline of about 98% from the peak. The exchange now lists a single-digit number of active pairs, with WETH against USDB carrying most of what trading remains. This did not happen in a vacuum. Blast itself peaked near $2.2 billion in TVL in mid-2024 and has since shed about 97% of it; the chain secures only around $70 million today, roughly 0.12% of all layer-2 value. Thruster did not fail on its own terms so much as ride its chain down.

| Metric | Peak (2024) | Now (2026) |

|---|---|---|

| Thruster TVL | ~$321M | ~$5M |

| Blast L2 value | ~$2.2B | ~$70M |

| Position on Blast | #1 dApp | quiet DEX |

| Cumulative DEX volume | — | $8.78B |

Security, audits and smart contract risk on Blast

On the engineering side, Thruster Finance is better than its price suggests. The core AMM was reviewed by Code4rena in a public competitive audit in February 2024, covering around 1,465 lines of code across 11 contracts, and additional reviews were carried out by other firms. The headline result was reassuring: no medium or higher severity issues in the core contracts, plus timelock delays and publicly verifiable code.

That Code4rena contest ran from February 16 to 23, 2024, with a $25,200 prize pool, and put the contracts in front of a large field of independent auditors competing to break them. Open, adversarial review of that kind tends to surface more than a single private audit, which, I think, counts in Thruster's favor.

The honest caveat is that an audit prices code risk, not market risk. The gauge and router contracts sat outside the scope of that public audit, and no later review has surfaced publicly. So a user can reasonably trust the swap math while still facing the larger dangers that no audit addresses: a token that keeps inflating and a chain that has lost almost all of its users.

Risks and limits for Thruster liquidity providers

For anyone considering providing liquidity, the risks are concrete. Impermanent loss is the classic one: in a volatile pair, you can end up worse off than if you had simply held the two assets. On top of that, thin TVL means real slippage on anything but small trades, and concentrated-liquidity positions need an active range strategy or they stop earning. The biggest risk has nothing to do with the code. Thruster's health is bolted to Blast's, and Blast's own L2BEAT risk profile carries serious flags around upgrade controls and bridge safety.

What that dependence means for Thruster Finance users in 2026 is fairly stark. A DEX with only a few million dollars of liquidity cannot absorb large orders without moving the price against the trader, so the practical use case has narrowed to small swaps in a handful of pairs. The yield opportunity that once made providing liquidity attractive has thinned along with the volume, and the THRUST rewards that topped it up are now diluted by ongoing emissions. For most users, the honest assessment is that Thruster is interesting to study and risky to farm.

Thruster vs other Blast DEXs: the DeFi landscape

Thruster won the native-DEX slot on Blast, but winning that slot never let it escape the chain. Compared with other Blast AMMs that competed for the same liquidity, Thruster's edge was always its first-mover status and its tight integration with Blast's native yield and points. Those advantages were real during the farm and largely evaporated after it. The broader lesson for the DeFi landscape is that a native DEX inherits both the upside and the downside of its host chain, with very little room to diverge. When the ecosystem is hot, the native exchange looks unstoppable; when it cools, there is nowhere to hide. Names like Ring Protocol and Fenix competed for the same deposits, and none of them found a way to keep growing once Blast's incentives dried up. The table below frames the trade-off Thruster always carried.

| Factor | Thruster | Other Blast DEXs |

|---|---|---|

| Launch status | First, Blast-endorsed | Later entrants |

| Native yield integration | Built in | Varies |

| Peak TVL | ~$321M | Lower |

| Fate after points farm | Sharp decline | Similar decline |

What Thruster Finance teaches about Blast DeFi

Thruster Finance is a well-built decentralized exchange that arrived at the right moment on the wrong chain, or at least a chain whose moment passed quickly. The code held up, the volume was real, and the design was sensible. None of that mattered once the incentives that summoned the liquidity were switched off. As a tool it still works; as an investment it is a cautionary tale about mercenary capital. The open question is bigger than one protocol: can any native DEX outlive the hype cycle of the chain it was built to serve, or is that fate sealed the moment the points run dry?