APR meaning: interest rate, credit cards, and crypto

A 24% APR on a credit card and a 24% APR on a DeFi pool look like the same promise. They are not even close. One is a number a lender is legally required to calculate a certain way and disclose accurately. The other is an estimate that floats from block to block and answers to nobody. APR, short for annual percentage rate, is one of the most quoted figures in money and one of the most misread. This piece starts where most people first meet it, with credit cards, loans, and mortgages, where the annual percentage rate has a strict legal meaning. Then it follows the same three letters into crypto, where they mean something looser and a good deal riskier.

What APR means and why APR is important

Start with the official version. In the United States, the annual percentage rate is defined under the Truth in Lending Act and its rulebook, Regulation Z, as the cost of credit expressed as a yearly rate. That phrasing carries weight. APR is not just interest. It folds in the mandatory fees that come with a loan, such as origination charges and certain closing costs, and expresses the whole package as one yearly percentage. Lenders do not get to be vague about it, either. According to the Consumer Financial Protection Bureau, a disclosed APR on a regular transaction has to be accurate within one-eighth of a percentage point of the real figure. That precision is exactly what crypto quietly drops, and we will come back to it.

APR vs interest rate: the real difference

People use "APR" and "interest rate" as if they were the same word. They are not, and the difference is money. The interest rate is the price of borrowing the principal, the raw cost of the money itself. The APR includes the interest rate plus the fees required to get the loan, spread across a year. On a no-fee credit card the two are usually identical, because there are no extra charges to fold in. On a mortgage they pull apart, sometimes by half a point or more, because closing costs and points get baked into the APR but not the rate. A simple way to use them: compare interest rates to understand your monthly payment, and compare APRs to understand the true cost of borrowing money over the life of the loan. There is a third number that muddies all of this — APY — and it belongs in the same table.

| Term | What it measures | Includes fees? | Includes compounding? |

|---|---|---|---|

| Interest rate | Cost of the principal | No | No |

| APR | Yearly cost of the loan | Yes | No |

| APY | Yearly return with compounding | Yield side | Yes |

How APR works and how it's calculated

The arithmetic is the easy part. The fee inclusion is where lenders quietly compete.

The basic APR formula

To find what you actually pay day to day, lenders take the APR and divide it by the number of periods in a year. A 26.99% APR on a credit card becomes a daily periodic rate of about 0.0739%, which is 26.99 divided by 365. Carry a $3,000 balance for a full year at that rate and you are looking at roughly $810 in interest, which is why a high-APR balance is so punishing to sit on. The headline number is annual — the damage is daily.

What APR includes and what it leaves out

Where lenders differ is in what they pack into the figure. A mortgage APR is meant to include loan origination fees, discount points, and certain closing costs, which is the whole reason it sits above the quoted interest rate. It leaves out charges you can avoid, like late fees or over-limit penalties, because those are the price of behavior, not the price of the credit. So when two lenders quote the same interest rate but different APRs, the higher APR is telling you that one of them is charging more in fees. Read that gap closely.

Fixed vs variable APR

An APR can also move. A fixed APR stays put unless the lender notifies you and follows the rules. A variable APR is tied to a benchmark, usually the prime rate, and shifts when that benchmark does. When the prime rate increases, your variable APR climbs with it, often within a billing cycle, and your minimum payment can rise without you borrowing another cent. Most US credit cards run on variable APRs, which is why card rates marched higher through the recent run of rate hikes. If your card's rate seems to change on its own, that is the reason.

Types of APR on credit cards explained

Here is something most people never notice: a single credit card can carry four or five different APRs at once, and which one applies depends entirely on what you do with the card. The purchase APR covers everyday spending. The cash advance APR, almost always higher and with no grace period, kicks in the moment you pull cash from an ATM. The balance transfer APR applies to debt you move over from another card, sometimes at a teaser 0%. The penalty APR is the punishment rate, triggered by a late payment, and it can push your cost toward 30%. Then there is the introductory APR, the 0% offer that makes new cards look free for a while. It is not free. It expires. The one piece of genuinely good news is the grace period on purchases. Pay your statement balance in full by the due date and you owe no interest on those purchases at all. Carry even a dollar into the next cycle and that grace period usually collapses.

Mortgage APR and the cost of a loan

On a 30-year mortgage, the APR is the number that quietly exposes the fees. Two lenders can advertise the same 6.5% interest rate, but if one charges two points and a heavy origination fee, its APR might read 6.8% while the other sits at 6.55%. Spread across a few hundred thousand dollars and three decades, that gap is real money, often tens of thousands of dollars over the life of the loan. The larger the loan amount, the more a small APR difference compounds into a large absolute cost. When you shop a mortgage, the interest rate sells you the monthly payment, but the APR tells you what the loan costs.

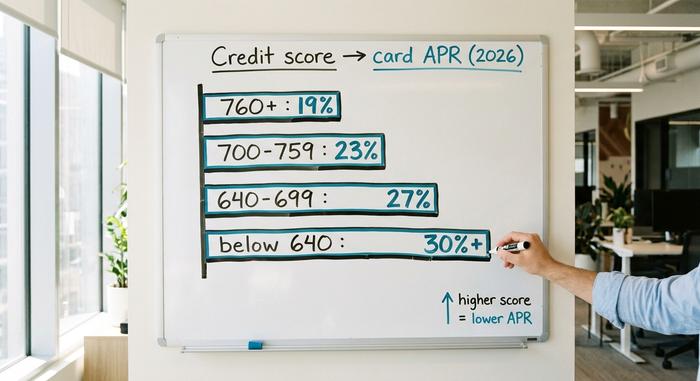

How your credit score affects the APR

APR is priced to risk, and your credit score is how a lender measures that risk in one number. A borrower with a 780 score and one with a 620 score applying for the same card are not offered the same deal. The higher score gets the lower APR, because the lender expects to lose less money on them. This is the most direct lever you have. Building credit, paying on time, and keeping balances low push your score up, and a better credit score pulls your APR down on the next card or loan you take. "What is a good APR?" has no single answer, because it depends on the product and your profile. A respectable credit-card APR for someone with excellent credit would be a brutal one on a mortgage. The table below shows roughly where US credit-card APRs landed by score band in 2026. It is illustrative, not a quote, since every issuer prices its own way.

| Credit score band | Typical card APR (2026, illustrative) |

|---|---|

| Excellent (760+) | ~18–21% |

| Good (700–759) | ~21–25% |

| Fair (640–699) | ~25–29% |

| Poor (below 640) | ~29%+, or declined |

What APR means in crypto and DeFi

Now the same three letters cross into crypto, and the ground shifts under them. In a decentralized finance app, APR still means an annual percentage rate, but it is no longer the price you pay to borrow. It is the yield you might earn for lending, staking, or supplying liquidity. And the part that matters most — nobody is legally on the hook to make the number accurate.

Staking APR

Lock up ETH to help secure Ethereum and you earn a staking reward, quoted as an APR. As of June 2026, Ethereum's official staking page shows a base APR of about 2.6%, with more than 40 million ETH staked, roughly 32% of the total supply. If you would rather not run your own validator, a liquid-staking service like Lido does it for you and hands back a token; Lido's stETH was paying about 2.36% in late June 2026, after the protocol's 10% fee. Notice how modest those are. The real yields of crypto staking sit nowhere near the four-digit numbers people remember from the last bull market.

Lending APR

Lend a stablecoin into a money market like Aave and you earn a supply APR set by demand. When more people want to borrow, the rate rises; when borrowing dries up, it falls. In late June 2026, USDC suppliers on Aave V3 were earning about 3.22% and USDT suppliers about 2.22%, according to the analytics tracker Aavescan. That yield is real in one specific sense — it comes from borrowers actually paying to borrow. Plenty of crypto yields are not backed by anything so concrete.

Why crypto APR isn't TradFi APR

Here is the catch. None of these crypto APRs carry the guarantees behind a credit-card APR. There is no Truth in Lending Act, no regulator's tolerance, no requirement to fold in fees or disclose anything accurately. The rate is a live estimate that can change block by block, and the real costs, such as gas, protocol cuts, and smart-contract risk, are yours to find out the hard way. The label is identical; the protections are gone.

| Where | Rate (mid-2026) | Backed by |

|---|---|---|

| ETH staking (ethereum.org) | ~2.6% APR | network rewards |

| Lido stETH | ~2.36% APR | staking, net of 10% fee |

| Aave V3 USDC supply | ~3.22% APR | borrower demand |

| Aave V3 USDT supply | ~2.22% APR | borrower demand |

| US high-yield savings | ~4–5% APY | bank deposit, insured |

APR vs APY: the crypto compounding trap

Crypto platforms love to show you APY instead of APR, and the reason is marketing. APR is the simple annual rate. APY, annual percentage yield, assumes you keep reinvesting your earnings, so it folds compounding back in. The formula is APY = (1 + APR/n)^n − 1, where n is how often it compounds. At ordinary rates the difference is cosmetic: a 20% APR compounded daily works out to 22.13% APY, a gap of barely two points. At absurd rates it becomes a lie. A new farm advertising "365% APR" compounded daily computes to an APY of around 3,678%, a number that assumes the reward token holds its price for a full year while the protocol mints more of it every block. It almost never does. High-emission reward tokens routinely lose 50% to 95% of their value within twelve months, so the dollar return bears no resemblance to the headline. The rule of thumb writes itself. When a yield is small, APR and APY tell roughly the same story. When a yield is enormous, the APY is the number engineered to impress you, and the interest accrues to whoever printed the token, not to you.

When a high APR is a warning sign

The cleanest lesson in crypto APR came from a project that did exactly what the math said it could. Anchor Protocol, built on the Terra network, offered a fixed 19.5% APY on deposits of the UST stablecoin. Not a floating rate set by borrowers, a fixed one, subsidized to stay high. It worked — in the way a fire works. By April 2022, more than 72% of all UST in existence was parked in Anchor, and its deposits had swollen from $8.65 billion in January to a peak of $17.15 billion in May. The subsidy keeping the rate alive was burning around $6 million a day. When confidence cracked, the deposits ran for the exit, and Anchor's total value locked fell from $17.15 billion to under $30 million in twenty-six days. The yield was never coming from real economic activity. It was a countdown. I think of Anchor every time a platform dangles a double-digit "safe" yield. Whenever an APR sits far above what borrowers or a network can plausibly pay, that is the question to ask: where is this money actually coming from?

Conclusion

Same three letters, two different worlds. In traditional finance, APR is a regulated, fees-inclusive price that a lender has to calculate properly and disclose within a fraction of a point, a number with a law behind it. In crypto, APR is an estimate of yield with no such backing, accurate only until the next block or the next bank run. The skill, oddly, is the same in both places. Do not just read the rate; read what is behind it. Before you chase any APR, on a card, a mortgage, or a DeFi pool, ask the one question that protects you: who, exactly, is obligated to make this number true?