Yield farming explained: how to earn passive income on DeFi platforms

CoinDesk pegged DeFi's total value locked at over $130 billion in early 2026. A big chunk of that money landed there because somebody decided to farm it. Yield farming turned idle crypto into working capital, and five years after the initial craze, it is still one of the main reasons people put tokens into DeFi at all.

So what actually is this thing? Yield farming is the practice of staking or lending crypto assets on DeFi platforms to collect rewards. Fees from trades, interest from borrowers, freshly minted governance tokens. It remains the most popular yield farming strategy in the DeFi sector. DeFi Summer in 2020 started the rush. The hype died down, but the tools got better, the risks got clearer, and the yield opportunities are still real. This piece walks through how the process of yield farming works, which cryptocurrency protocols matter in 2026, and what risks involved you should worry about. If you want to learn how yield farming can become a way to earn passive income, or if you just want to understand the DeFi infrastructure, read on.

What is DeFi yield farming and how does it work?

Strip away the jargon and yield farming is simple: you put crypto into a protocol, the protocol uses it, and you get paid. Usually what the protocol needs is liquidity, and what you get back is a cut of the action.

Take Uniswap. It is a DEX, a decentralized exchange. No order book. It runs on an automated market maker (AMM) where traders swap tokens against a liquidity pool. Somebody has to fill that pool. That somebody is you.

Drop ETH and USDC into the pool. You get LP tokens back. Those LP tokens are your receipt, proof of how much of the pool belongs to you. Every swap that goes through generates a fee. Your cut matches your share. On top of that, many DeFi protocols hand out governance tokens to liquidity providers as a bonus.

Lending works the same way. Aave and Compound hold your crypto so borrowers can use it. The interest borrowers pay? That is your yield. Smart contracts handle all of it. No bank. No broker.

Why should you care? Because yield farming is how decentralized finance gets its liquidity. Pull the liquidity providers out and the whole DeFi ecosystem stalls. No trades on DEXs. No loans on lending protocols. Nothing. Yield farming allows DeFi users to become the plumbing of the financial system and get paid for it. Liquidity providers earn trading fees and token rewards by supplying digital assets to these protocols. In return, they earn passive income on crypto assets that would sit dead in a wallet otherwise. The rewards are typically sent straight to your address through smart contracts, and rewards are often paid in the platform's governance token.

How to get started with yield farming step by step

Getting started with yield farming is more straightforward than most guides make it sound. The yield farming process breaks down into six steps, and once you understand them, you can get started with yield farming on most DeFi platforms that offer it.

First, you need a Web3 wallet. MetaMask, Rabby, and Trust Wallet are the most common. These wallets plug straight into DeFi protocols. Your keys, your crypto.

Next, buy the crypto you plan to farm with. Stablecoins like USDC and USDT are solid starting points. They dodge the price swings that make other tokens harder to predict.

Then comes the part that matters most: picking a pool. Look at audit reports. Check how much TVL the protocol holds. See how long it has been running. A protocol that has been live for two years with $500 million in deposits is a different bet than one that launched last month.

Once you have picked your platform, connect your wallet and deposit. For DEX liquidity pools, you will need two tokens in equal dollar amounts, like $500 of ETH and $500 of USDC. The protocol gives you LP tokens that track your position. Some DeFi protocols let you stake those LP tokens in a separate contract for additional rewards. That is liquidity mining.

Last step: claim and reinvest. Rewards build up over time. You can pull them out, swap to stablecoins, or roll them back into the same pool to compound. Yield aggregators like Yearn Finance handle the reinvestment part so you do not have to touch anything.

One thing to note: every transaction on Ethereum costs gas. Moving tokens, depositing, claiming rewards, each step has a fee. On Ethereum mainnet, gas can eat into small positions. Different DeFi platforms on Layer 2 networks like Arbitrum or on chains like Solana and Avalanche offer much lower transaction fees, making yield farming accessible even with a few hundred dollars. Many DeFi protocols now deploy across multiple chains specifically to give users cheaper options. The process may seem complex at first, but the actual steps are the same regardless of which chain you use.

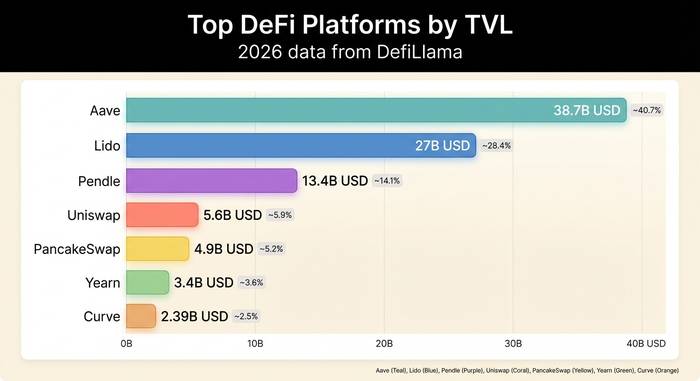

Top DeFi yield farming platforms in 2026

The market has consolidated around a handful of protocols that have proven themselves over years of operation. These are the top DeFi yield farming platforms for earning in 2026. Various DeFi projects and protocols compete by offering yield through different mechanisms, and platforms offer everything from conservative lending to aggressive leveraged pools.

| Platform | Type | TVL | Typical APY range | Chains supported | Key feature |

|---|---|---|---|---|---|

| Aave | Lending/borrowing | $38.7B | 2-15% | Ethereum, Polygon, Arbitrum, Optimism, Avalanche | Flash loans, multi-chain |

| Lido | Liquid staking | $25-30B | 3-5% | Ethereum, Polygon | ETH staking without 32 ETH minimum |

| Pendle | Yield tokenization | $13.4B | 8-25% | Ethereum, Arbitrum | Fixed/variable yield splits |

| Uniswap | DEX (AMM) | $4.5-6.8B | 5-25% | Ethereum, Polygon, Arbitrum, Base, BNB Chain | Concentrated liquidity (v3) |

| Curve Finance | DEX (stablecoins) | $2.39B | 3-10% | Ethereum, Polygon, Arbitrum | Low slippage stablecoin swaps |

| PancakeSwap | DEX (AMM) | $4.9B | 10-400%+ | BNB Chain, Ethereum, Arbitrum | High APY farms, low fees |

| Yearn Finance | Yield aggregator | $3.4B | 5-80% | Ethereum, Fantom, Arbitrum | Automated yield optimization |

Aave sits at $38.7 billion in TVL as of 2026. That makes it the largest DeFi protocol by deposits, and it is not close. It was the first to do flash loans, where you borrow without collateral and repay in the same transaction. For farmers, the real draw is Aave's multi-chain deployment. You can lend stablecoins on Arbitrum and pay a fraction of the gas you would on Ethereum mainnet.

Nobody was talking about Pendle in 2023. By 2026, it holds $13.4 billion in TVL. What happened? Pendle lets you split any yield-bearing token into two pieces: the principal and the yield. Trade them separately. Lock in a fixed rate. Or bet on rates going up. It captured over half the DeFi yield sector's TVL by August 2025. The next biggest yield tokenization protocol has roughly a fifth of that.

Uniswap v3 changed the math for LPs. Old-style pools spread your money across every possible price. V3 lets you pick a narrow band, say ETH between $3,000 and $3,500. All your capital works inside that range, so your fee income per dollar goes way up. Sounds great until the price drifts outside your band and you earn nothing. Managing these positions is a part time job.

Curve is the stablecoin spot. Because the tokens in Curve pools trade near the same price (USDC, USDT, DAI), impermanent loss barely registers. Curve also kicked off the veToken model. Lock your CRV, get votes, steer rewards to specific pools. A whole mini economy grew around that mechanic.

Yearn Finance sits on top of everything else as a yield aggregator. Deposit your tokens and Yearn's automated yield strategies move capital to wherever the best yields are. It takes a performance fee, but for farmers who do not want to manually shuffle assets between protocols, Yearn saves time and gas costs. Platforms like these allow users to earn rewards without constantly monitoring positions. These platforms often update their strategies to capture shifting yield opportunities across the crypto yield farming space, and they offer different risk profiles to match your investment strategy.

Crypto yield farming strategies, APY, and how returns work

Not all crypto yield farming approaches carry the same risk or produce the same yield farming returns. As a DeFi strategy, yield farming may range from conservative stablecoin lending to aggressive leveraged plays. Understanding each helps you see how yield farming can offer high rewards when the approach fits your comfort level. Finding the best DeFi yield farming setup is about matching risk to reward.

Most people start with DEX liquidity. That means providing liquidity to decentralized exchanges and taking a cut of swap fees. Pair two tokens, drop them in an AMM, and collect additional rewards in governance token incentives. How much you make depends on how busy the pool is. High traffic pools on Uniswap or PancakeSwap pay 10-30% APY. Smaller or brand new pools plaster 200% APY numbers everywhere to lure in early capital. Those numbers almost never last.

Lending crypto is the conservative play. Put USDC into Aave, someone borrows it, you get interest. Simple. Stablecoin lending crypto on established platforms pays 2-8% APY right now. That moves with demand. When the market heats up and more people want to borrow, rates climb. Some protocols sweeten the deal with governance token rewards. Users who want to lock up their crypto for predictable returns without touching volatile pools tend to park here first.

Yield aggregation through Yearn Finance or Beefy Finance takes the manual work out of compounding. Instead of claiming rewards and putting them back in yourself, the aggregator does it for you. This saves gas and grows your stack faster. Automated yield strategies can produce 5% to 80% APY depending on the protocol and market conditions.

Liquid staking blew up over the past two years. Lido lets you stake ETH and hands you stETH, a token that earns staking rewards but can still be used elsewhere. Drop that stETH into Aave as collateral or into a Curve pool and you are earning two layers of yield at once. This "stacking" trick is how the experienced yield farmers squeeze 15-20% out of ETH that would otherwise earn 3-4%.

Then there is leveraged farming, which is either brilliant or suicidal depending on timing. You borrow extra tokens to beef up your position. If the pool pays 15% and you borrow at 5%, the 10% spread is your profit, multiplied by however much leverage you took. Alpaca Finance built an entire platform around this idea. The catch? One bad hour and your whole position gets liquidated.

APY vs APR: know the difference

Annual Percentage Yield (APY) folds in compounding. Annual Percentage Rate (APR) does not. A pool showing 50% APR pays less than one showing 50% APY over the same period. DeFi platforms love showing APY because the number looks bigger. Before you move money, figure out which number you are looking at.

| APR displayed | Compounding frequency | Effective APY |

|---|---|---|

| 10% | None (simple interest) | 10.0% |

| 10% | Monthly | 10.47% |

| 10% | Daily | 10.52% |

| 50% | None | 50.0% |

| 50% | Daily | 64.8% |

CoinGecko nailed it: "If you don't know where the yield comes from, you are the yield." If the APY looks insane, ask where the money is actually coming from. Real yields come from trading fees that real people pay, from interest on real loans, from protocol revenue. When a pool pays you in a token that was printed yesterday with no revenue behind it, that yield is a countdown timer. The token dumps, and your "100% APY" turns into a 50% loss.

Benefits and risks of yield farming

The benefits and risks of yield farming is where most beginners either protect their money or lose it. Yield farming can pay more than any savings account at a bank. But the risks involved have cost people real money, and risks like smart contract exploits are not just theory.

What yield farming offers:

Your tokens can work while you sleep. Instead of crypto sitting dead in a wallet, it generates fees, interest, or token rewards. Stablecoin farming on Aave or Curve gives 3-8% a year. Not exciting compared to 2021 numbers, but way better than a savings account paying 0.5%. Want more? Push into riskier pools. Some exceed 50% APY, though they eat your time and test your nerves.

There is a secondary benefit people overlook. Earning COMP, CRV, or UNI as rewards in the form of governance tokens means you get a vote in how the protocol runs. Some of these tokens went on to do 10x or more after distribution, adding capital gains on top of farming income. Others crashed to near zero. That is the game.

What can go wrong:

| Risk | What happens | Severity | How to reduce it |

|---|---|---|---|

| Impermanent loss | Token prices in your pool diverge, leaving you worse off than just holding | Medium-High | Use stablecoin pools or narrow-range positions on Curve |

| Smart contract bugs | A vulnerability in the protocol code gets exploited | High | Stick to audited protocols with long track records |

| Rug pulls | Project developers drain user funds and disappear | Critical | Avoid unaudited protocols, check if admin keys are renounced |

| Liquidation | Leveraged positions get forcibly closed when collateral value drops | High | Keep leverage low, monitor positions, set alerts |

| Regulatory changes | New laws restrict DeFi activity or specific tokens | Medium | Diversify across jurisdictions and protocol types |

| Token price decline | Reward tokens lose value, erasing farming profits | Medium | Regularly convert rewards to stablecoins or blue-chip assets |

The numbers tell the story. Chainalysis counted $3.41 billion stolen from crypto protocols in 2025. One hack, Bybit, was $1.5 billion of that. North Korean hackers, FBI confirmed. In Q1 2026, Drift Protocol on Solana lost $285 million. Rug pulls took another $2.8 billion in 2025. MetaYield Farm alone vanished with $290 million in February 2025. One bright spot: DeFi exploit losses in Q1 2026 dropped 89% compared to the year before, so the protocols are getting tougher to crack. But "tougher" is not "safe."

Impermanent loss catches more beginners than anything else. Here is what happens. You drop equal amounts of ETH and USDC into a pool. ETH pumps 50%. Sounds good, right? Except the AMM has been selling your ETH the whole way up and buying USDC. You end up with less ETH and more USDC than if you had done literally nothing. The word "impermanent" is misleading. The loss only reverses if prices go back to exactly where they started. Good luck with that. One study of Uniswap V3 found that 54.7% of LPs in volatile pairs lost money when all was said and done.

Yield farming vs crypto staking

People mix these up all the time. "Is crypto staking the same as yield farming?" No. Not really.

Staking is one specific thing: you lock tokens to help run a Proof of Stake blockchain. Ethereum needs validators to lock 32 ETH. They earn staking rewards for doing it, around 3-5% a year. Lido made this accessible in 2025 with a Community Staking Module that cut the minimum to just 1.3 ETH. You stake, you wait, you collect.

Farming covers more ground. It wraps staking into a bigger bag that includes liquidity pools, lending, borrowing tricks, and chasing yields across protocols. Staking is passive. Farming takes work.

| Factor | Yield farming | Crypto staking |

|---|---|---|

| Returns | 5-100%+ APY, variable | 3-15% APY, more predictable |

| Risk level | Higher (smart contract risk, impermanent loss, rug pulls) | Lower (slashing risk, token depreciation) |

| Complexity | Requires research and active management | Deposit and wait |

| Lock-up period | Usually flexible, withdraw anytime | Often fixed (days to months) |

| Gas costs | Multiple transactions, higher fees | Single deposit, minimal fees |

| Tokens needed | Often token pairs | Single token |

| Best for | Experienced users comfortable with DeFi | Beginners wanting predictable income |

My honest advice for anyone new to DeFi: start with staking or stablecoin lending. Learn how wallets work. Learn what gas feels like on your balance. Get used to the interface before touching anything complicated. I keep watching people dive into 300% APY pools with leverage on tokens they found yesterday. It ends the same way almost every time.

Why yield farming is the backbone of decentralized finance

Yield farming is the backbone of DeFi. Take it out and the whole thing collapses. That is not hyperbole.

DEXs need liquidity or trades fail. Lending protocols need deposits or nobody can borrow. Bridges need reserves or tokens cannot move between chains. Every single one of those functions depends on regular people deciding to park their crypto in a smart contract. Farming rewards are the reason anyone bothers.

Go back to 2019. Early DeFi had a chicken-and-egg problem. Nobody wanted to trade on DEXs because the liquidity was thin and the slippage was terrible. Nobody wanted to provide liquidity because there were no traders. Then Compound dropped COMP tokens on lenders and borrowers in June 2020. Money flooded in. TVL went from under $1 billion to over $10 billion in a few months. By July 2025, TVL hit $153 billion, a 57% jump from just three months earlier. The flywheel is simple: more liquidity means tighter spreads, tighter spreads bring traders, traders generate fees, and fees pull in more liquidity.

The game has moved way past simple token drops. Curve built a whole economy around vote-locked CRV tokens. Lock your CRV, get voting power, direct rewards to specific pools, and earn boosted yields. An entire layer of "Curve wars" protocols like Convex emerged just to control those votes. Yearn Finance wraps all of this into one-click vaults so you can earn from many DeFi protocols without touching any of the complexity yourself. Meanwhile, real-world assets are creeping into DeFi. Protocols now offer yield at 5-8% APY on tokenized US Treasuries. DeFi's infrastructure supports everything from basic stablecoin lending to stacked, multi-protocol plays. Many DeFi platforms now serve as platforms for earning that rival what banks offer. The best opportunities combine solid liquidity provision with real revenue, not just token printing, and that means providing liquidity to DeFi platforms that actually generate fees.

Mordor Intelligence puts the DeFi market at about $238 billion in 2026 and projects $770 billion by 2031. Sounds big until you compare it to the $50.8 trillion US securities market. That gap is the opportunity and the gamble, depending on how you look at it. Farming is what fills the gap, one pool at a time.

Will it all work? Some of it. Not all of it. Smart contract bugs are still real, governments are still writing rules, and most protocols will not survive the next five years. But here is something worth noting: during the February 2026 market crash, DeFi TVL only dropped 12%. In 2022, it fell over 50%. That is progress. The core idea, paying people to provide liquidity to decentralized platforms, has now lived through two bear markets and come back stronger each time. If you want in, understand what you are risking, start with small money, and never lock up more than you can stomach losing.