Rocket Pool: The Decentralized ETH Staking Protocol

Rocket Pool runs about 3.67% of Ethereum's liquid staking market. Next to Lido, which dwarfs it, that is a rounding error. And yet on the one measure Ethereum actually loses sleep over, who controls the validators, Rocket Pool may be the most important staking protocol there is.

The reason is structural, not commercial. Most staked ETH flows through a handful of operators. Rocket Pool spreads it across roughly 1,500 of them, and anyone can join. This guide explains how Rocket Pool works, why that design matters for decentralization, what changed with the 2026 Saturn upgrade, and where the real risks sit. Small by size, the protocol is built to answer a problem the giants created.

What Rocket Pool is and how it works

Rocket Pool is a decentralized Ethereum staking protocol. Strip away the jargon and it is a two-sided marketplace. On one side are people who want staking rewards without running hardware or locking up a full 32 ETH. On the other are node operators who run the validators. Rocket Pool's smart contracts match them and split the rewards. In short, it is a liquid staking protocol that turns staking into something anyone can join from either side.

rETH: liquid staking without 32 ETH

When you deposit ETH, you receive rETH, Rocket Pool's liquid staking token. You can hold it, sell it, or use it across DeFi while the underlying ETH stays staked. The entry point is as low as 0.01 ETH, far below the 32 ETH a solo validator needs.

rETH does not pay you tokens. It grows in value instead. One rETH was worth about 1.1666 ETH as of June 2026, and that exchange rate rises as staking rewards accrue. Your balance never changes; the rate does. This rising-rate design is cleaner for taxes and for DeFi than the rebasing model some competitors use.

By mid-2026 there were roughly 329,000 rETH in circulation, worth on the order of $654 million, with the protocol securing more than 500,000 ETH in total and around $925 million in value locked. Because rETH is a plain ERC-20 token, holders put it to work elsewhere: as collateral in lending markets, in liquidity pools, or as a building block in other DeFi strategies, all while the staked ETH underneath keeps earning.

Minipools and node operators

The validators themselves run inside minipools. A node operator puts up a bond of their own ETH, and the protocol tops it up from the pooled deposits until the minipool holds enough to run a validator. The operator runs the hardware; the rETH holders supply most of the capital. Both earn, in different proportions.

Smart nodes and the oracle DAO

Operators run open-source smart node software that manages their validators on Ethereum's beacon chain and talks to Rocket Pool's contracts. Watching over the system is the oracle DAO, an elected set of operators that reports validator performance and exchange-rate data on-chain. It is the bridge between Ethereum's validators and Rocket Pool's accounting.

Why Rocket Pool matters for decentralization

Here is the argument that justifies the whole project. Ethereum's security risk is not that any one protocol is large. It is that stake concentrates in a few hands. A single entity approaching a third of all staked ETH can threaten the chain's ability to finalize blocks; past half, it could censor or reorganize them. Concentration also creates correlated risk: if most validators run the same client software or sit in the same data centres, one bug or one outage can slash a huge share of the network at once. Spreading validators across many independent operators is the cleanest defence, and the staking market has been drifting the wrong way for years.

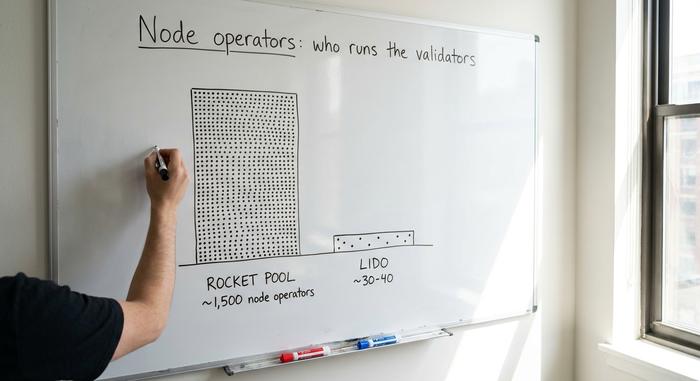

1,500 operators versus a curated few

Lido, the dominant liquid staking protocol, has historically run its validators through a few dozen professional operators it selects. It has been opening up through a Community Staking Module that adds hundreds more permissionless operators, which narrows the gap, but the bulk of its stake still sits with the curated set. Rocket Pool took the opposite path from the start: permissionless onboarding. Anyone who meets the bond requirement can spin up a node and start validating, permissionless staking in its purest form, no application, no gatekeeper. That is how it reaches roughly 1,500 independent Rocket Pool node operators spread across the world, a level of validator diversity that has been baked into the design rather than bolted on later.

Rocket Pool versus Lido and the centralization risk

The numbers frame the stakes. The total ETH staked on Ethereum reached about 39 million by mid-2026, near 32% of supply. Lido alone accounted for roughly 22.7% of all staked ETH, below the 33% finality-threat threshold but uncomfortably close, and it controls close to a majority of the liquid staking sub-market. Rocket Pool sits at about 3.67% of that market. By size it loses badly. By structure it is the credible decentralized alternative, which is why Ethereum researchers keep pointing to it even as its market share stays small.

Governance: the protocol DAO and oracle DAO

Control is split between two bodies. The oracle DAO is a small, elected group of operators trusted to report off-chain data such as validator balances and the rETH exchange rate. The protocol DAO, on-chain since the Houston upgrade, is the broader governance layer: it sets parameters, controls the treasury, and votes on upgrades, with voting power tied to staked RPL. The two-tier design keeps the sensitive data feeds in expert hands while pushing the bigger policy decisions out to token holders. It is not flawless decentralization, but it is a real attempt to put protocol decisions in token holders' hands rather than a company's.

The RPL token and collateral model

RPL is the most misunderstood piece of Rocket Pool, partly because most guides describe it as it used to be. For years, node operators had to bond RPL worth at least 10% of their staked ETH as insurance against poor performance, with the option to stake up to 150% for extra rewards. That made RPL mandatory collateral.

Saturn changed this. RPL is no longer required collateral; it became an optional, revenue-bearing asset, with a protocol fee switch directing real income to those who stake RPL from February 2026. The token still carries 5% annual inflation and governs the protocol. As an investment it has been brutal, though: RPL traded near $61.90 at its April 2023 peak and around $1.33 by mid-2026, a drop of roughly 98%.

| RPL token | Detail |

|---|---|

| Role | Governance + optional revenue-bearing stake (post-Saturn) |

| Old role | Mandatory operator collateral (10-150% of ETH bond) |

| Supply | ~22.4 million RPL |

| Inflation | 5% annual |

| Price | ~$1.33 (Jun 2026) vs $61.90 ATH (Apr 2023) |

Saturn I: the 4 ETH bond and megapools

If you read an older guide to Rocket Pool, it will tell you node operators need 8 or 16 ETH. That is out of date. The Saturn I upgrade, live in February 2026, was the biggest change since launch, and it reshaped the economics.

The headline is the bond. At mainnet in 2021, an operator needed 16 ETH. The Atlas upgrade in April 2023 cut that to 8 ETH. Saturn I cut it again to 4 ETH, doubling how many validators a given amount of capital can support and lowering the barrier for new operators. Saturn also introduced megapools. Instead of each validator living in its own separate minipool contract, a megapool lets one node operator run many validators under a single contract, cutting gas costs and making it far simpler to manage a large set of validators. Combined with the 4 ETH bond, that lowers both the capital and the operational overhead of scaling up. Saturn also flipped RPL from mandatory collateral to the optional revenue model above.

| Era | Operator bond | Protocol tops up | RPL required |

|---|---|---|---|

| Launch (2021) | 16 ETH | 16 ETH | Yes (collateral) |

| Atlas (Apr 2023) | 8 ETH | 24 ETH | Yes (collateral) |

| Saturn I (Feb 2026) | 4 ETH | 28 ETH | No (optional) |

The direction is clear: smaller bonds, more operators, a lower bar to running your own validator. For a protocol whose entire pitch is decentralization, that matters more than any price chart.

Rewards, APR, and the 14% commission

Be honest about the yield, because the marketing rarely is. As a passive rETH holder, your net staking return was around 2.00% APR in May 2026, in line with Ethereum's base staking rate after fees. That is not a high-yield product — it is ordinary ETH staking with extra liquidity bolted on.

The split is where node operators earn their edge. Rocket Pool takes a commission on the rewards generated by the pooled, or rETH-side, ETH, historically around 14%, and pays it to the operator running the validator. So an operator earns the base rate on their own bond, plus that commission on the protocol-supplied ETH, plus any RPL revenue under the new model. With a smaller bond now matched against far more pooled ETH, a well-run node can earn a meaningfully higher effective APR than a passive rETH holder, which is the incentive that keeps operators showing up. Operators can also opt into the smoothing pool, which pools MEV and block-proposal rewards across participating nodes and shares them evenly, smoothing out the luck of which validator proposes a lucrative block. rETH holders earn the base rate through the rising exchange rate, with the commission already netted out. Nobody is getting rich on the rETH side, and any guide promising a passive double-digit yield is selling something.

Risks: smart contracts, RPL, and liquidity

Three risks deserve a clear look, not a generic warning. The first is smart contract risk. Rocket Pool's contracts have been audited repeatedly by firms including ConsenSys Diligence and Sigma Prime, which is reassuring, but the code is complex and audits reduce risk rather than remove it.

The second is RPL itself. Its roughly 98% fall from the 2023 peak hurt node operator economics under the old collateral model and dented confidence, and a revenue switch does not undo years of underperformance overnight. The third is liquidity. rETH trades in thinner secondary markets than Lido's stETH, so in a sharp sell-off it can slip to a discount against its underlying ETH until arbitrage closes the gap. Slashing risk, worth noting, falls on operators rather than rETH holders, which is one reason rETH is the lower-stress way in.

There is a fourth, quieter risk: governance. With RPL cheap and turnout often low, a determined holder could accumulate outsized voting power over the protocol DAO. Decentralized validators do not automatically mean decentralized decision-making, and that is a tension Rocket Pool, like every DAO, still has to manage.

How to stake ETH with Rocket Pool

There are two doors, and they ask very different things of you. The easy one is rETH: deposit ETH through the Rocket Pool dApp or buy rETH on a decentralized exchange, from as little as 0.01 ETH, and you are done. It is passive, needs no hardware, and you earn staking rewards automatically through the rising rETH rate.

The other door is running a node. That means putting up a 4 ETH bond, installing the smart node software, and keeping a machine online and healthy. You earn more, but you take on real operational work and slashing exposure. For most people, rETH is the answer; running a node is for those who want to contribute to decentralization directly.

Is Rocket Pool worth it? The honest verdict

Separate the protocol from the token, because they are not the same bet. As a protocol, Rocket Pool is the most credible decentralized alternative in Ethereum staking, and Saturn I made it cheaper and more open to run. As a token, RPL has been a poor hold, down around 98% from its high, and a fresh revenue model has yet to prove it can reverse that. If you want liquid staking with a clean conscience about decentralization, rETH is a reasonable choice. RPL is a separate, riskier question. Which leaves the real open question hanging over the whole sector: does Ethereum reward decentralization enough for the principled option to win, or does convenience keep concentrating stake in a few hands?