Pendle Finance: How to Trade and Lock Crypto Yield

Wall Street has split bonds into principal and interest for decades. Pendle does the same thing to crypto yield. It takes a yield-bearing token, separates the original deposit from the interest it earns, and lets you trade the two halves on their own. That sounds abstract until you see what it buys you: a way to lock a fixed return in a market where yields swing wildly, or a way to bet on those yields going up.

Most explainers stop at "Pendle is a yield protocol." That skips the part that actually matters. This guide covers what Pendle is, how the PT and YT tokens work, the ways people use it, and the risks. No finance degree required.

What Is Pendle and Who Built It

Pendle is a permissionless DeFi protocol for trading yield. In plain terms, it turns a variable, messy crypto yield into something you can price, fix, or speculate on, the way a bond desk handles interest rates. It works with all sorts of yield-bearing assets, from staked ETH and liquid restaking tokens to stablecoin yield positions.

It is not new or untested. Pendle launched on Ethereum on 17 June 2021, built by TN Lee, a former Kyber Network contributor, and Vu Nguyen as chief technology officer. The team raised around $17 million from backers including Binance Labs, Spartan Group, and HashKey. Today it runs on Ethereum, Arbitrum, BNB Chain, Base, and several other networks.

It also won its niche convincingly. As the leading yield-trading platform, Pendle holds roughly 98% of the on-chain yield-tokenization market, which means when people talk about trading yield in DeFi, they are usually talking about Pendle. The reason it caught on is simple. Crypto yields move constantly, and most of the time your capital is stuck in one position earning whatever the market gives it. Pendle breaks that open.

The cleaner way to picture it is an interest-rate market for crypto. In traditional finance, traders bet on and hedge interest rates all day long, yet on-chain that barely existed before Pendle. In late 2025 the team pushed further into the same territory with Boros, a venue for trading funding rates, the recurring payments that drive perpetual futures. The underlying idea never changes: take a floating, unpredictable rate and turn it into something you can fix, trade, or hedge.

How Pendle Works: PT, YT, and Yield Trading

Here is the whole engine: one wrap, one split, two tokens. Get that and everything else falls into place.

Splitting yield into SY, PT, and YT

Start with a yield-bearing token, say a staked-ETH token that earns staking rewards. Pendle first wraps it into a standardized format called SY. Then it splits that SY into two separate tokens. One is the Principal Token, or PT, which represents your original deposit. The other is the Yield Token, or YT, which represents all the future yield that deposit will earn until a set expiry date. Now the deposit and its interest are two assets you can hold or sell independently.

A quick example makes it click. Deposit a staked-ETH token worth $1,000 that earns about 4% a year into a one-year Pendle market. Pendle hands you back a PT worth roughly $960 today plus a YT that collects the next twelve months of staking rewards. Sell the YT and you have effectively cashed out a year of future yield up front. Keep it and you ride whatever the real yield turns out to be.

Locking a fixed yield with PT

PT is the calm half. It trades at a discount to the full value, and at maturity it redeems one-for-one for the underlying asset. So if a PT costs 0.95 and redeems for 1.00 at expiry, that 5% gap is your locked, fixed return. You buy it, you wait, you collect. No guessing about where rates go next week. This is the closest thing DeFi has to a fixed-rate bond, and it is the main draw for people who just want a predictable yield. Why bother? Because crypto yields are famously fickle. A staking or lending rate can sit at 8% one month and 3% the next. PT lets you nail down a number today and stop watching the chart.

Trading yield with YT and the AMM

YT is the spicy half. Holding YT means you collect the variable yield as it streams in, right up to expiry, when YT decays to zero. Buy YT and you are betting yield stays high or climbs. Sell it and you are hedging, locking in today's rate before it can fall. A custom automated market maker, built specifically for assets that decay over time, prices PT and YT and lets people trade in and out. Every Pendle market has a fixed maturity date, which is why timing matters so much here. There is a subtlety worth flagging. YT loses value as it nears expiry simply because less yield is left to collect, so a YT bought a month before maturity is a very different bet from one bought a year out. The closer to expiry, the cheaper the YT, and the sharper the gamble.

| Token | What it is | Who buys it | At maturity |

|---|---|---|---|

| PT (Principal) | Your deposit, minus the yield | Fixed-income seekers | Redeems 1:1 for the asset |

| YT (Yield) | The future yield only | Yield speculators, hedgers | Decays to zero |

PENDLE Token, vePENDLE, and sPENDLE

PENDLE is the protocol's own token, and its job changed in a big way recently. The maximum supply sits around 258 million. The price peaked at $7.50 in April 2024 during the protocol's biggest boom, and trades near $1.44 for a market cap around $248 million in mid-2026.

For years, the token worked through vePENDLE, a vote-escrow model. You locked PENDLE for up to two years, and in return you got governance votes, a boost on your liquidity-provider rewards of up to 250%, and a share of protocol fees. Lock longer, earn more. It rewarded commitment but punished anyone who wanted to stay liquid.

In January 2026 Pendle replaced that system with sPENDLE. Staking is now liquid, with a 14-day withdrawal window instead of multi-year locks, and the economics shifted toward buybacks: roughly 80% of protocol fees are used to buy PENDLE on the market for stakers. The goal was to widen the buyer base beyond governance die-hards and tie the token more directly to revenue.

| PENDLE snapshot | Detail |

|---|---|

| Max supply | ~258 million |

| All-time high | $7.50 (April 2024) |

| Price / market cap | ~$1.44 / ~$248M (mid-2026) |

| Staking | sPENDLE (liquid, fee buybacks) since Jan 2026 |

How to Use Pendle: Fixed Yield and Strategies

There are four common plays, from safest to spiciest. Pick the one that matches what you believe about yields.

First, lock a fixed yield. Buy PT, hold it to maturity, and you know your return up front. This is the boring, reliable option, and most newcomers start here.

Second, go long yield. If you think a yield will rise or stay high, buy YT cheaply and collect the stream. Because a small amount of capital controls the yield on a much larger deposit, it behaves like a leveraged bet on rates. Done right, a spike in yield pays off handsomely; done wrong, the YT simply expires worthless and you lose what you paid. It is the high-risk, high-reward corner of Pendle.

Third, hedge or short yield. If you expect rates to drop, selling YT locks in today's higher rate, the same way a farmer locks in a crop price before harvest.

Fourth, provide liquidity. Supply PT and YT to a pool and earn trading fees plus PENDLE rewards. This is also how a lot of people farmed points and airdrops during the 2024 craze, when depositing certain tokens on Pendle multiplied their rewards across several programs at once. That stacking effect put Pendle at the center of the farming frenzy, and it is also why much of that capital left the moment the rewards dried up.

Pendle Market Growth: TVL Boom and Cooldown

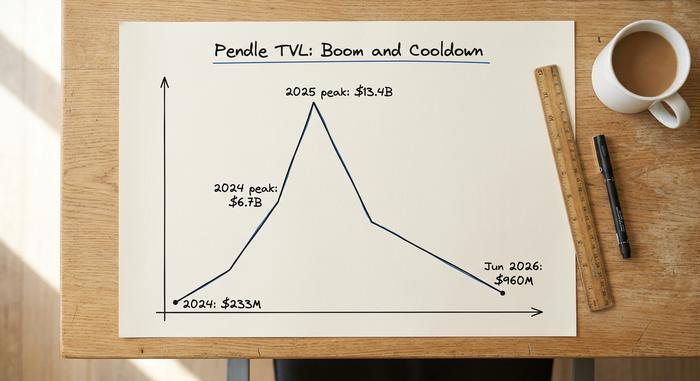

Pendle's total value locked tells a dramatic story, and it is worth knowing before you assume the protocol only goes up. The first surge came in 2024, when liquid restaking tokens and the points meta sent TVL from about $233 million to a peak near $6.72 billion in a matter of months. The second wave came in 2025, driven by Ethena and stablecoin yields. Average TVL that year was about $5.8 billion, up 79%, with a record around $13.4 billion at the peak and $8.3 billion in August. Protocol fees hit $44.6 million for 2025, up 134%.

Then came the cooldowns across Pendle's markets. Because every market has an expiry, big batches of positions mature and unwind at once, draining TVL in waves once a narrative fades. By June 2026, TVL had cooled to roughly $960 million across 11 chains. The rails kept working; the hype just moved on. For a beginner, the lesson is not that Pendle failed. It is that money on Pendle follows whatever yield narrative is hot, so a quiet chart usually means there is no mania to farm right now, not that the protocol broke.

| Period | TVL | Driver |

|---|---|---|

| Early 2024 | ~$233M → $6.72B | Liquid restaking + points meta |

| 2025 (avg / peak) | $5.8B / ~$13.4B | Ethena + stablecoin yields |

| June 2026 | ~$960M | Post-boom cooldown |

The Main Risks of Using Pendle

Pendle is powerful, but it is not a savings account, and you should manage the risk like an adult. Smart-contract risk is real: in September 2024 a hack drained about $27 million from Penpie, though it is worth being precise here, Penpie was a third-party reward aggregator built on top of Pendle, not Pendle's core contracts. Maturity risk catches beginners off guard: once a market expires, the yield stops and YT is worth nothing, so positions are not "set and forget." You have to come back, redeem, and roll into a new market if you want to keep earning. Liquidity providers face impermanent loss when PT and YT prices move apart. And there is plain rate risk, a fixed yield you locked can look bad if market rates jump right after you commit. None of this means avoid Pendle. It means size your positions and watch the expiry dates.

One more habit is worth building: check who actually holds your money. Pendle's audited core contracts are one layer, but the dozens of third-party vaults, aggregators, and points programs that plug into Pendle each run their own code, and each carries its own risk. Penpie was exactly that kind of add-on. When a yield looks unusually high, it is often because an extra layer of smart-contract risk is bolted on somewhere. Read what you are depositing into, not just the headline rate.

Where Pendle Fits in DeFi Today

Strip away the boom-and-bust headlines and Pendle did something durable: it built the first real yield-trading market on-chain, the place where crypto figured out how to price and fix yield instead of just chasing it. The TVL cooled from its manic highs, but the machinery is still running, still settling fixed and floating yield every day. The open question is whether on-chain fixed income becomes a quiet utility everyone uses or stays a trader's playground. The sPENDLE buyback shift and the move into funding-rate markets suggest the team is betting on the former, a slower, more durable business rather than another points sprint. Either way, if you want to understand DeFi yields, start by understanding how Pendle splits them.