ESMA: How the EU Supervises Crypto and Capital Markets

ESMA is one of the most consequential crypto regulators on the planet, and it has never licensed a single exchange. That sounds like a contradiction. It isn't. The European Securities and Markets Authority writes the rulebook and keeps the list of who is allowed to operate, while the actual licences are stamped somewhere else entirely. If you trade crypto in Europe, use a European platform, or run one, this quiet office in Paris already shapes your day whether you have heard of it or not.

Most explainers stop at "ESMA is the EU's securities watchdog" and move on. That leaves out the part that matters for crypto: who actually does what. So let's sort out the real division of labor, because almost everyone gets it wrong.

What ESMA Is and Where It Came From

ESMA is not a crypto agency. It is the European Union's securities regulator, and crypto landed on its desk years after it was built. That history matters, because it explains how the authority thinks.

The European Securities and Markets Authority opened its doors on 1 January 2011, replacing a weaker advisory committee called CESR. It was a direct response to the 2008 financial crisis, when national regulators had watched the same banks blow up and somehow reached different conclusions. The fix was an independent EU authority with real teeth over EU financial markets, set up under Regulation (EU) No 1095/2010 and based in Paris.

It is a lean operation for the scope it covers. ESMA ran on about 358 staff and a budget near €76 million in 2024, according to its 2024 annual accounts, supervising markets that move trillions. It is led by the ESMA chair, Verena Ross, and answers to the European Parliament. The European Commission signs off on its technical standards before they become law. That independence is the whole point. ESMA is supposed to care about financial stability across the whole union, not about any one member state's pet industry. Keep that mandate in mind, because it drives everything the authority does with crypto.

How ESMA Fits the EU Supervision System

You cannot understand ESMA's crypto powers without the org chart. The authority almost never supervises individual firms directly. It sets standards and pushes national regulators to apply them the same way. The goal it repeats in every annual report is dull but telling: stable and orderly financial markets, deeper EU capital markets, and stronger protection of investors. The day-to-day cop on the beat, though, is somebody else.

The three European Supervisory Authorities

ESMA is one of three European Supervisory Authorities created after the crisis. The European Banking Authority covers banks, the European Insurance and Occupational Pensions Authority covers insurers and pension funds, and ESMA covers the securities markets. Above them sits the European Systemic Risk Board, watching for the kind of risk that brings down the whole system. Together they form the European System of Financial Supervision. They also meet in a Joint Committee to handle problems that cut across all three sectors, and crypto is exactly that kind of problem.

National competent authorities and supervisory convergence

Here is the part people miss. ESMA's Board of Supervisors is made up of the heads of the national competent authorities, the actual financial regulators in each member state, such as Germany's BaFin or France's AMF. ESMA's job is supervisory convergence: making sure a rule means the same thing in Dublin as it does in Frankfurt. It does that through binding technical standards, guidelines, and Q&As rather than by licensing firms one by one.

What ESMA supervises directly

There are exceptions. ESMA does directly supervise a short list of pan-European entities where one EU-level regulator makes more sense than 27 national ones: credit rating agencies, trade repositories, and certain central counterparties. From 2026 it also oversees ESG rating providers. The list is deliberately narrow, and for most of the market ESMA stays one level up, setting the rules others enforce.

| Authority | Sector | Headquarters | Crypto role under MiCA |

|---|---|---|---|

| ESMA | Securities and markets | Paris | Rule-setting, central register, convergence |

| EBA | Banking | Paris | Direct supervision of significant stablecoins |

| EIOPA | Insurance and pensions | Frankfurt | Limited; mainly cross-sector via Joint Committee |

ESMA's Crypto Role Under MiCA Explained

Here is where it gets practical. The Markets in Crypto-Assets Regulation, MiCA, is the EU's single rulebook for crypto, and it slots neatly into the structure above. The single most common mistake is to assume ESMA licenses your exchange. It does not.

Who actually licenses a crypto firm

Under MiCA, a crypto-asset service provider, a CASP, applies to its national competent authority, not to ESMA. A CASP is any firm that runs an exchange, holds customer crypto in custody, operates a trading platform, or gives crypto advice. BaFin licenses German platforms, the AMF licenses French ones, and so on. ESMA's role is to make those national decisions consistent and to keep convergence tight so market participants cannot shop for the softest regulator.

The stablecoin side is split off to a different desk. The European Banking Authority directly supervises the issuers of "significant" asset-referenced tokens and e-money tokens. Those are the ones large enough to matter for the whole financial system. The thresholds are high enough that, so far, no asset-referenced token has been classed as significant and only a handful of e-money token issuers sit under EBA's direct watch. So a crypto licence in Europe can run through three desks, and ESMA owns the rulebook, not the rubber stamp.

The MiCA register of authorized CASPs

ESMA's most underrated power is a list. Under Articles 109 and 110 of MiCA, it maintains a central public register of every authorized CASP and every white paper for crypto-assets offered in the EU. If a platform is licensed under MiCA, it is on that register. If it is not on the register, it is not licensed, full stop. As of mid-June 2026, the register showed 216 authorized CASPs across 30 EEA markets, as tracked across the official national registers. That list is now the thing that decides which crypto firms get to touch hundreds of millions of Europeans legally.

ESMA keeps a second list that gets less attention but matters just as much: a public register of entities flagged for offering crypto services without authorization. One register tells you who is cleared; the other names firms that national regulators have called out as non-compliant. For a careful user, those two lists do more work than any marketing page a platform can put up, because they come from the regulators themselves rather than from the company selling you something.

Technical standards and the single rulebook

The unglamorous engine room is the technical standards. ESMA has drafted dozens of regulatory and implementing technical standards, plus guidelines and Q&As, that turn MiCA's broad articles into precise rules: what a white paper must contain, how custody must be segregated, what counts as market abuse in crypto. This is where "convergence" stops being a slogan. When every national regulator applies the same standard, a firm licensed in one member state can passport across the EU on equal terms.

| Date | What applied | Who leads |

|---|---|---|

| 2023 | MiCA enters into force | EU co-legislators |

| 30 June 2024 | Stablecoin rules (Titles III and IV) | EBA and ESMA |

| 30 December 2024 | CASP rules (Title V) | National authorities and ESMA |

| 1 July 2026 | EU-wide transitional period ends | National authorities |

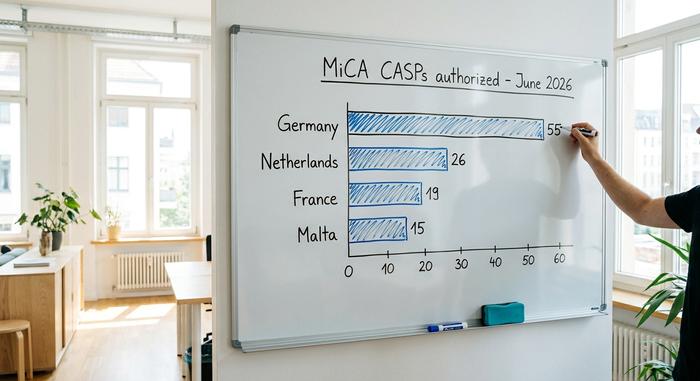

Where are the licences being granted? Very unevenly. A handful of member states have done most of the early authorizing.

| Country | Authorized CASPs (as of 16 June 2026) |

|---|---|

| Germany | 55 |

| Netherlands | 26 |

| France | 19 |

| Malta | 15 |

ESMA Warnings and Investor Protection in Crypto

ESMA cannot approve a coin or promise that one is safe. So its main retail lever is blunt: warnings, plus the power to restrict or ban harmful products. Investor protection, its duty to safeguard retail investors, is written into its founding mandate, and crypto is where that mandate gets tested hardest.

The authority keeps repeating the same message. In a December 2024 warning it told consumers plainly that many crypto-assets are highly risky and speculative, and that MiCA does not make them safe. In October 2025 the three European Supervisory Authorities issued a joint revised warning, a coordinated reminder that a licensed platform is not the same as a protected investment. The subtext is honest: ESMA can regulate the plumbing, but it cannot stop a token from going to zero.

That product-intervention power is not theoretical. The authority used it in 2018 to ban binary options for retail clients across the EU and to cap leverage on contracts for difference, two products that were steadily draining ordinary investors. It is the same legal muscle the authority can point at the riskiest corners of crypto, and everyone in the industry knows it.

The warnings are not landing the way regulators might hope. Crypto ownership in Europe keeps climbing. The European Central Bank found that 9.7% of surveyed eurozone households held crypto by late 2024, up from roughly 4% in 2022. In money terms it is still small, around €75 billion, about 0.23% of EU household financial assets, but the direction of travel is clear. More Europeans are buying, which is exactly why ESMA keeps the product-intervention power loaded.

How ESMA Is Closing the Offshore Crypto Loophole

The most consequential recent move was not a fine. It was a set of guidelines that shut a door offshore exchanges had leaned on for years.

The trick was "reverse solicitation": the claim that an offshore platform did not market into the EU because the customer came to it. Used narrowly, the exemption is fine. Used as a business model, it let non-EU exchanges serve millions of Europeans while ignoring MiCA. ESMA's reverse-solicitation guidelines, published in February 2025 and effective from 27 April 2025, read the exemption very narrowly. A slick onboarding flow, a localized website, or an EU ad campaign is not a customer wandering in by accident.

The pressure has continued. ESMA's April 2026 statement pushed national authorities to enforce orderly wind-downs. The EU-wide transitional period, the grandfathering window that let pre-MiCA firms keep operating, closes on 1 July 2026. After that date the rule is simple: be on the register, or be out of the EU market. The authority is deliberately narrowing the perimeter, and offshore platforms that assumed Europe was optional are finding out it is not.

What ESMA Means for Crypto Users and Builders

For a user, the practical move is one click: check the register before you trust a platform. If a service touts an EU licence, it should appear in the MiCA register; if it doesn't, treat the claim as marketing. For a builder, the headline is the passport. A MiCA licence from one national authority lets you serve the whole EU without 27 separate applications. That is the single biggest reason firms are racing to get authorized. Retail investors get more disclosure, clearer complaint channels, and standardized risk warnings; what they don't get is a guarantee that the asset will hold its value, and ESMA is careful never to imply one.

What ESMA's Crypto Power Comes Down To

ESMA's power over crypto is structural. It does not run raids or freeze wallets. It writes the rules everyone else enforces, and it keeps the list that decides who is in and who is out. That list is now the gatekeeper to 450 million people. The interesting question for the next few years is not whether ESMA gets tougher. It is whether convergence holds once dozens of national regulators start reading the same rulebook under real commercial pressure. Before you send money to any European platform, do the boring thing first: look it up on the register.