What Is Crypto Lending and How Crypto Loans Work in 2026

Three years ago, the crypto lending business looked dead. Celsius, BlockFi, and Genesis had vaporized roughly $34.8 billion in customer loans between them, and the survivors were small enough to fit on one screen. By Q3 2025 the combined market was back at an all-time high of $73.59 billion, according to Galaxy Digital's lending report. The recovery did not happen the way most people expected. It was not CeFi clawing its way back; it was DeFi quietly absorbing the demand, with Aave and Morpho alone holding more than $26 billion in active TVL by mid-2026. The other surprise is who the new customers are. Most of them are not chasing yield. They are borrowers who want cash without selling their bitcoin.

What is crypto lending in plain English?

Think of crypto lending as two parallel queues. One queue holds people who own crypto assets — various cryptocurrencies, often USDC or USDT, sometimes BTC or ETH — and want their idle coins to earn interest and a bit of liquidity along the way. The other queue holds people who own coins they refuse to sell but still need cash for something — a tax bill, a house deposit, a leveraged trade. A platform stitches the two queues together. With CeFi the platform is a company that takes custody; with DeFi it is a lending protocol that runs on smart contracts. So the two main types of crypto lending you will meet are centralized crypto lending and decentralized lending, and the rest of this guide takes them apart one at a time. In 2026 the borrower queue is longer than the lender queue, mostly because borrowing against bitcoin is, for a long-term holder, structurally different from selling it.

How crypto loans work for borrowers

Here is how crypto lending works in practice on the borrow crypto assets. You pick a lending platform. You move your cryptocurrency into the right wallet or custody account, putting up your crypto as collateral. You tell the platform the loan amount you want, and a moment later the funds (USDC, USDT, or in some cases plain fiat through a bank transfer) show up. You pay interest each month or have it accrued. When you pay off the loan and repay the balance in full, your digital asset comes back to you. The underlying blockchain handles the settlement either way. The three numbers that decide whether this goes smoothly are LTV, liquidation threshold, and the breathing room between them.

LTV (loan-to-value) is the share of your collateral you can borrow against. Aave V3 sets ETH collateral at 80% LTV with an 83% liquidation threshold. Nexo caps borrowers at 50% LTV and pulls the trigger around 83.3% of collateral value. The unwritten industry standard for BTC-backed loans hovers near 50%, partly out of post-2022 caution.

Now run the actual math. You put $10,000 worth of ETH on Aave V3 and pull $5,000 in USDC. Starting LTV: 50%. ETH falls 20%? Your collateral is worth $8,000, LTV is 62.5%, you are still fine. ETH falls 40%? Collateral is $6,000, LTV is 83.3%, and the contract is now free to liquidate you. CeFi platforms usually send a margin call before that point and give you a window to top up the collateral or pay down the loan. DeFi protocols are not so polite. The smart contract liquidates the second the threshold breaks, dumps your collateral on a DEX, and skims a liquidation penalty for the trouble.

A habit that saves a lot of borrowers from waking up to a sold bag: keep a 20-point gap between starting LTV and liquidation threshold. On an 83% threshold, start at 50–60% and you can absorb a serious selloff before anything bad happens. The lower you start, the larger the price drop the loan can swallow before bitcoin you wanted to keep is gone.

| Platform | Asset | Max LTV | Liquidation threshold | Margin call before liquidation? |

|---|---|---|---|---|

| Aave V3 | ETH | 80% | 83% | No, instant |

| Aave V3 | BTC (WBTC) | 73% | 78% | No, instant |

| Nexo | BTC | 50% | ~83.3% | Yes |

| Ledn | BTC | 50% | 70% | Yes |

| SALT | BTC | 70% | varies | Yes |

What lenders earn — and how rates are formed

The other side of the market looks different. A lender deposits stablecoins or crypto into a pool, and the platform routes those assets to borrowers. Interest is paid back to lenders, minus a platform fee. On DeFi protocols, the interest rate is not "set" by anyone. It floats with utilization: when borrowing demand is high, rates rise to attract more deposits; when the pool is mostly idle, rates fall. CeFi platforms post fixed rates and absorb the floating-rate risk themselves, which is why their rates are usually higher but also why their failure modes are worse.

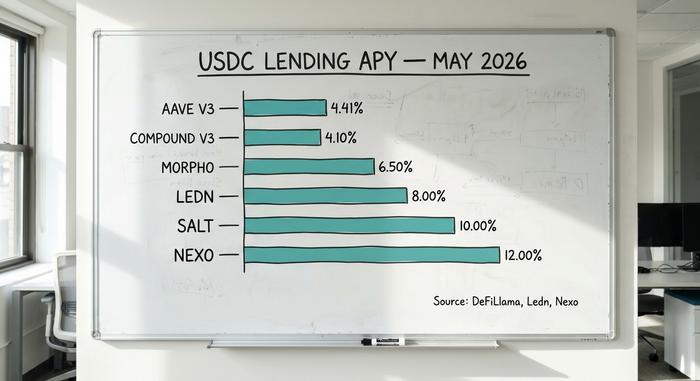

In April 2026, USDC on Aave V3 averaged about 4.41% APY over 30 days. Compound V3 sat near 4.1%. Morpho vaults reached 4–7% depending on the strategy. CeFi rates were noticeably higher: Ledn paid 6.5–8.5% on USDT, Nexo advertised up to 12%, and YouHodler reached 15% on certain tiers. That premium does not come from CeFi being smarter. It comes from CeFi taking risks DeFi does not, mainly lending pooled deposits to institutional borrowers at terms retail lenders never see.

CeFi vs DeFi crypto lending platforms compared

Most explainers stop at "CeFi is a company, DeFi is a smart contract." Unlike traditional lending, where a bank mediates every transaction, crypto lending routes lenders and borrowers through either a custodial company or an autonomous smart contract. The more useful distinction in 2026 is who eats the loss when something breaks.

On a CeFi platform, you transfer ownership of your coins to the company. If the company goes bankrupt, you become an unsecured creditor in bankruptcy court. Celsius depositors learned this in 2022; many recovered cents on the dollar, years late. On a DeFi protocol, your funds sit in a smart contract you can audit, and bad debt is socialized across remaining depositors or absorbed by the protocol's safety module. Aave's response to the April 2026 Kelp DAO exploit, where attackers minted $293 million in counterfeit rsETH and posted it as collateral, illustrates this. The protocol faced up to $230 million in potential bad debt, $6.6 billion in TVL was withdrawn within days, and the recovery was handled through governance rather than a court.

| Dimension | CeFi (Nexo, Ledn, SALT) | DeFi (Aave, Morpho, Compound) |

|---|---|---|

| Custody | Platform holds your keys | Smart contract holds funds |

| KYC | Required | Not required (wallet only) |

| Rate setting | Fixed, set by platform | Floating, set by utilization |

| Transparency | Periodic attestations | On-chain, live |

| Failure mode | Insolvency, frozen withdrawals | Smart-contract bug, bad debt |

| Recovery path | Bankruptcy court | Governance, safety module |

| 2026 market share | ~37% ($24.37B) | ~55.7% ($40.99B) |

DeFi dominance is concentrated. Aave alone holds roughly 62.8% of all DeFi lending. CeFi is also concentrated, just differently: Tether's lending desk accounts for 57% of the CeFi book, around $10.14 billion. Both ecosystems carry concentration risk; it just sits in different places. For most crypto holders, sound risk management means spreading exposure across both models rather than concentrating crypto holdings on one platform.

Crypto loan rates and APYs in May 2026

The numbers below come from each platform's published rates and DeFi dashboards in April–May 2026. They move daily, so treat them as a snapshot.

| Platform | Type | USDC supply APY | USDC borrow APR | Max LTV (BTC) | Source |

|---|---|---|---|---|---|

| Aave V3 | DeFi | ~4.41% | ~5.8% | 73% | DeFiLlama, Apr 2026 |

| Compound V3 | DeFi | ~4.1% | ~5.5% | 75% | Compound dashboard |

| Morpho | DeFi | 4–7% (vaults) | 5–8% | varies | Morpho app |

| Coinbase Borrow | DeFi (Morpho) | n/a (borrow only) | ~6.5% | 70% | Coinbase, $2.17B issued |

| Nexo | CeFi | up to 12% | from 2.9% | 50% | Nexo, Apr 2026 |

| Ledn | CeFi | 6.5–8.5% (USDT) | from 11.4% | 50% | Ledn Open Book |

| SALT | CeFi | up to 10% | from 9.95% | 70% | SALT Lending |

| YouHodler | CeFi | up to 15% | varies | up to 97% | Public rates |

DeFi rates are noticeably tighter and lower because the rate clears the market in real time. CeFi rates fan out because each platform sets its own spread and serves a different customer.

Best crypto lending platforms compared in 2026

There is no single "best" platform. The right choice depends on which side of the market you are on and how much custody risk you accept.

For HODLers who want cash without selling. Ledn has been operating since 2018 and has originated more than $10.2 billion in BTC-backed loans, with the cleanest reserve attestations in CeFi. SALT runs since 2016 with no customer asset losses on record. Coinbase Borrow, powered behind the scenes by Morpho, originated over $2.17 billion in USDC loans by April 2026, and expanded its collateral list this year to include XRP, DOGE, ADA, and LTC alongside BTC and ETH.

For DeFi-native borrowers. Aave V3 carries $14.25 billion in TVL and $10.99 billion in active loans, generating $708 million in annualized protocol fees. Morpho has grown to $11.78 billion in TVL with backing from Apollo Global Management. Both protocols are non-custodial, so you never give up your keys.

For yield-chasers with higher risk tolerance. Nexo returned to the US market on February 16, 2026, after a $45 million settlement with regulators. It manages around $11 billion in customer assets and offers up to 12% on stablecoins to crypto lenders. The CeFi premium is real, and so is the custody risk.

For institutional borrowers. Maple Finance, with roughly $2.1 billion in TVL, runs undercollateralized loans to vetted market-makers and trading desks. Most retail users will never touch it, but it is where the crypto-credit business is regrowing fastest.

One thing I keep coming back to when watching this market: the surviving platforms in 2026 are the ones that practiced segregated custody, published attestations, and refused rehypothecation in 2022. The list of disappeared platforms is much longer than the list of survivors. Past stability is not a guarantee, but it is the closest thing this market has to a track record.

Borrowing against bitcoin without selling: the tax angle

Ask any US holder who has been in bitcoin since 2017 why they would borrow against it instead of just selling. The answer almost always comes down to one number: the capital gains bill. IRS Notice 2014-21 (and Rev. Ruling 2019-24 after it) treats a crypto-backed loan the way the tax code treats a mortgage. You hand the lender collateral, you walk away with cash, and the IRS records nothing.

Picture a holder with 1 BTC bought at $40,000, now sitting at $100,000. Sell it, and at the long-term federal bracket of 15% they owe roughly $9,000 to the IRS that April. Borrow $50,000 against the same coin at 50% LTV, and the immediate tax bill is zero. They still pay interest on the loan, but the cost basis stays intact and the bitcoin stays under their name.

Here is the part most explainers gloss over. If the price collapses and the lender sells your collateral to cover the loan, the IRS treats that liquidation as a sale at the liquidation price. So a bad week can leave a borrower with both a tax bill and no asset, which is roughly the worst outcome a tax planner can imagine. From tax year 2026 onward, exchanges must file Form 1099-DA with cost basis on every sale, liquidations included. The era of unreported crypto sales is over.

Risks of crypto lending and liquidation no one warns about

Crypto lending exposes users to four risk categories most platform marketing glosses over.

Smart-contract risk. The April 2026 Kelp DAO exploit took $293 million through a single 1-of-1 verifier flaw in a LayerZero bridge and turned Aave V3 into the collateral receiver for $230 million in potentially worthless rsETH. Audits do not eliminate this; they reduce probability.

Liquidation cascades. When prices fall sharply, automated liquidations on DeFi protocols sell collateral into a falling market, depressing prices further and triggering more liquidations. The March 2024 ETH flash crash produced exactly this loop. Lenders with collateral at high LTV get wiped out first.

Custodial bankruptcy. Celsius, BlockFi, and Genesis all let depositors withdraw freely until they did not. Rehypothecation, lending the same collateral multiple times, turned a credit problem into a solvency problem. The 2026 survivors avoid this practice, but you have to trust the attestation, and attestations are not audited financial statements.

Regulatory and concentration risk. Tether holds 57% of the CeFi book; Aave holds 62.8% of DeFi. A regulatory action against either entity, or a stablecoin depeg, would ripple through every connected lending platform. MiCA's July 1, 2026 deadline reshapes EU access, and US retail access to crypto lending remains a narrow corridor of DeFi protocols and the few CeFi platforms (Nexo, Ledn) cleared by regulators.

Crypto loans carry no FDIC insurance, no SIPC protection, and no central counterparty. If something breaks, the recovery is in your hands. Unlike unsecured personal loans from a bank, the asset can be seized automatically and sold against you.

How to choose a crypto lending platform

Five quick checks before you deposit anything. Custody model first. Non-custodial (DeFi) means you hold the keys. Custodial (CeFi) means somebody else does, and that somebody has gone bankrupt before. Look at the gap between LTV ceiling and liquidation threshold next. Wider gap, more breathing room for a price drop. Then jurisdiction. Plenty of platforms legally cannot serve US residents. Security history is fourth. Did the platform freeze withdrawals in 2022? Has it been audited since? Transparency rounds out the list. Public attestations, on-chain proofs, monthly reserve reports. If any single check fails badly, the yield is not worth the trouble.