Compound Finance: the DeFi lending protocol that started it all

June 15, 2020. Compound Labs flipped a switch and started distributing COMP tokens to everyone who lent or borrowed on the protocol. Within a week, Compound's TVL went from $100 million to over $1 billion. Yield farmers piled in from everywhere. People were borrowing crypto just to earn more COMP than they paid in interest. DeFi Summer had officially begun.

That single event changed crypto. Not just Compound. The entire DeFi ecosystem. Every protocol that handed out governance tokens for using their product, every yield farming strategy that involved looping borrows and deposits, every "APY goes brrrr" meme on crypto Twitter for the next 18 months can trace its origin to what Compound did that week. Sushi copied it. Yearn built on top of it. Thousands of forks followed. The playbook: give users tokens for using your protocol, and they will come running.

Six years later, the landscape looks different. Aave overtook Compound in TVL and never looked back. Morpho, Euler, and newer lending protocols chipped away at the edges. Compound V3 redesigned the entire architecture. But Compound still runs. Still processes billions in loans. And still holds the distinction of being the protocol that proved permissionless lending could work at scale.

This is what Compound Finance is, how it works today, what happened between V2 and V3, and whether the COMP token and the protocol itself still matter in 2026.

How Compound Finance works: the lending mechanics

I lent my first USDC on Compound in 2020 and the experience was disorienting. There was no application form. No credit check. No bank employee asking about my income. I connected MetaMask, deposited 5,000 USDC, and within 15 seconds I was earning interest. The rate was about 4% APY at the time. The interest accrued every Ethereum block, roughly every 12 seconds.

Here is what happens when you deposit into Compound. You supply crypto to a liquidity pool managed by a smart contract. The protocol gives you cTokens in return (on V2) or credits your account directly (on V3). Your deposit joins a pool of the same asset. Borrowers take from that pool. They pay interest. That interest gets distributed to all depositors proportionally.

Borrowing works the opposite direction. You deposit collateral (say, ETH), and the protocol lets you borrow a percentage of that collateral's value in another asset (say, USDC). The maximum you can borrow depends on the collateral factor: if ETH has a collateral factor of 82%, you can borrow up to 82% of your ETH's dollar value. If ETH's price drops and your loan-to-value ratio exceeds the liquidation threshold, anyone can liquidate your position. They repay part of your debt and take your collateral at a discount.

The interest rates are not set by anyone. They are algorithmic, determined by a formula that considers how much of the available pool is being borrowed. Low utilization (lots of supply, few borrowers) means low rates for borrowers and low yields for lenders. High utilization (most of the pool is borrowed) means rates spike for both sides. This push and pull keeps supply and demand in balance without any human intervention.

| How lending works on Compound | Details |

|---|---|

| Supply | Deposit crypto, earn interest automatically |

| Borrow | Deposit collateral, borrow other assets |

| Interest model | Algorithmic (based on utilization rate) |

| Collateral factor | 60-90% depending on asset |

| Liquidation | Automatic when LTV exceeds threshold |

| Requirements | Crypto wallet + assets, nothing else |

| KYC | None |

| Minimum | None |

Compound V2 vs V3: what changed and why

Compound V2 was the version that powered DeFi Summer. It used a pooled model where every asset shared risk. You could deposit ETH and borrow DAI against it, or deposit WBTC and borrow USDC. All assets sat in interconnected pools. If one asset had a problem (an oracle failure, a depeg, an exploit), the contagion could spread across the entire protocol. Multiple assets meant multiple risk surfaces.

V3, called Comet, took a completely different approach when it launched in 2022. Instead of one big pool with everything in it, each V3 market has a single base asset. The USDC market lets you borrow USDC. Only USDC. You deposit ETH, WBTC, COMP, or other approved tokens as collateral, and you borrow USDC against them. The collateral tokens do not go into a shared pool. They stay isolated in the contract.

Why does this matter? Risk isolation. If something goes wrong with one collateral type, it does not contaminate the borrowing pool for other collateral types. Each market stands alone. V3 also simplified the interest model and removed the cToken wrapper. On V2, when you deposited USDC, you received cUSDC that accumulated value over time. On V3, you just deposit USDC and your balance grows directly. Cleaner for users, simpler for integrations.

The tradeoff: V3 is less capital flexible than V2. On V2 you could borrow against a basket of different assets. On V3, each market is separate. Want to borrow against ETH and WBTC simultaneously? You might need two separate positions in two markets. Aave kept the multi-asset model and many DeFi power users prefer it for that reason.

Compound V3 is deployed on Ethereum, Arbitrum, Polygon, Base, Optimism, and several other chains. Each deployment has its own markets with locally set risk parameters. The multi-chain expansion has been steady but slower than Aave's aggressive push to 14+ chains.

The COMP token: governance, distribution, and reality

COMP launched as the governance token for the Compound protocol. Maximum supply: 10 million tokens. The initial distribution allocated 42% to protocol users (liquidity mining), 26% to the founding team, 24% to investors, and 8% to community incentives.

The liquidity mining distribution was the spark that lit DeFi Summer. 2,880 COMP tokens distributed daily to lenders and borrowers, split equally between the two sides. At peak prices above $900 in 2021, that daily distribution was worth over $2.5 million. People borrowed assets they did not need, deposited collateral they did not want to lock up, all to earn COMP rewards worth more than the interest they paid. Recursive leverage. Deposit. Borrow. Deposit the borrowed amount. Borrow again. Stack the COMP rewards at every layer.

The COMP token hit an all-time high near $910 in May 2021. It trades far below that in 2026. The liquidity mining rewards have been reduced dramatically through governance votes as the community recognized that paying users millions in tokens to use the protocol was unsustainable.

In 2026, COMP exists primarily as a governance token. Holders vote on risk parameters, interest rate models, new market deployments, and treasury spending. The governance process works through on-chain proposals with 3-day voting periods and 2-day timelocks before implementation. Anyone holding or delegated at least 25,000 COMP can create a proposal. The threshold is high by design to prevent spam.

| COMP token snapshot | Details |

|---|---|

| Max supply | 10 million COMP |

| Type | ERC-20 governance token |

| Launch | June 2020 |

| Initial distribution | 42% users, 26% team, 24% investors, 8% community |

| All-time high | ~$910 (May 2021) |

| Governance | On-chain voting with 3-day period |

| Proposal threshold | 25,000 COMP |

Compound vs Aave: why Aave is winning

I have used both protocols for years. Let me be direct about the competitive reality.

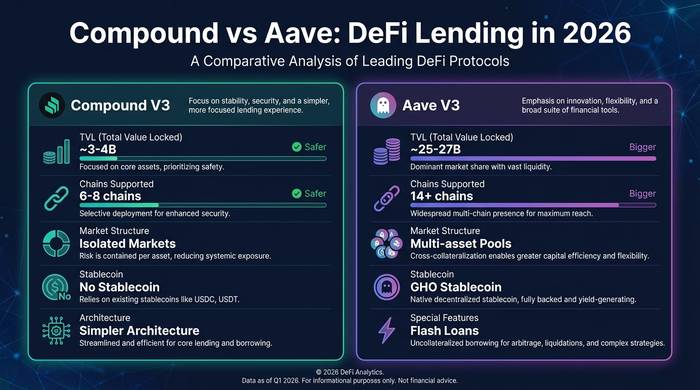

Aave has more TVL. Significantly more. Compound sits around $3-4 billion in 2026. Aave is north of $25 billion. That gap has been widening, not closing. Aave V3 deployed on 14+ chains. Compound V3 is on fewer. Aave launched its own stablecoin (GHO). Compound did not. Aave runs flashloans, rate switching between variable and stable, and dozens of collateral types per market. Compound V3's isolated market model is simpler but less flexible.

Why did Aave win? Execution speed and product breadth. When new chains launched and needed lending infrastructure, Aave deployed first. When the market wanted more collateral options, Aave added them faster. When stablecoins became a revenue opportunity, Aave built GHO. Compound moved more cautiously. V3's architecture is arguably more secure (risk isolation is a real advantage), but the market rewarded Aave's aggression over Compound's prudence.

| Metric | Compound V3 | Aave V3 |

|---|---|---|

| TVL (2026) | ~$3-4B | ~$25-27B |

| Chains deployed | 6-8 | 14+ |

| Market model | Single base asset per market | Multi-asset pools |

| Native stablecoin | No | GHO |

| Flash loans | No | Yes |

| Governance token | COMP (10M max) | AAVE (16M max) |

| Interest model | Utilization-based | Utilization-based (stable + variable) |

Compound's edge: simplicity and security. The V3 architecture is easier to audit, easier to reason about, and isolates risk better than Aave's shared pool model. For institutional users who prioritize safety over flexibility, Compound V3 is arguably the better choice. For DeFi power users who want maximum capital efficiency and product variety, Aave wins.

The newer competitors are worth watching too. Morpho started as an optimization layer on top of Compound and Aave but evolved into its own lending protocol with modular architecture. Apollo Global (the $938 billion asset manager) invested in Morpho, which tells you where institutional money thinks DeFi lending is heading. Euler V2 relaunched after its 2023 exploit with a completely redesigned architecture. Spark (MakerDAO's lending arm) carved out a niche for DAI borrowers. The DeFi lending market is not a two-horse race anymore, even if Aave and Compound still hold the most TVL.

My read on where Compound sits in 2026: it is the Honda Civic of DeFi lending. Not the fastest. Not the flashiest. But reliable, well-built, and it has been on the road long enough that you know it will not break down on the highway. People who want excitement use Aave. People who want sleep at night use Compound. Both approaches are valid.

How to use Compound Finance: the practical walkthrough

I walk new DeFi users through Compound before anything else because the interface makes lending intuitive in a way that most protocols do not.

Go to app.compound.finance. Connect MetaMask or any WalletConnect-compatible wallet. You will see the available markets: USDC on Ethereum, USDT on Arbitrum, ETH on Base, and so on. Pick the market that matches the asset you want to supply or borrow.

For lending: select your asset, enter the amount, approve the token spend, and confirm the deposit transaction. You start earning interest immediately. The rate shows on the dashboard and updates in real time based on utilization. Withdrawing is the same process in reverse. No lock-up period. Pull your funds whenever you want.

For borrowing: first deposit collateral (ETH, WBTC, or other approved assets). Then go to the borrow tab and enter how much of the base asset you want. The interface shows your health factor: a number that represents how close you are to liquidation. Stay above 1.0 or you risk losing collateral. I keep mine above 1.5 at all times because crypto can drop 20% before I wake up.

Gas fees vary by chain. Ethereum mainnet costs $5-20 per transaction. Arbitrum and Base cost under $0.10. If you are depositing less than $1,000, use an L2 deployment to avoid gas eating your yield.

Who founded Compound and where the protocol stands today

Robert Leshner, a former economist, founded Compound Labs in 2017. The team included Geoffrey Hayes as CTO. They raised $33 million across multiple rounds from Andreessen Horowitz, Bain Capital Ventures, Polychain, and Paradigm. The pedigree was top-tier Silicon Valley crypto.

Leshner stepped back from day-to-day operations in 2022 to focus on a new venture, Superstate, which builds tokenized Treasury funds for institutional investors. Compound Labs continues development. The protocol is governed by the Compound DAO, which controls the treasury, parameter settings, and upgrade decisions.

I think Compound's biggest contribution to crypto is not the protocol itself. It is the idea it proved: that you can build a bank without a bank. Before Compound, lending in crypto meant trusting a centralized platform (BlockFi, Celsius, Nexo) that could mismanage your funds and go bankrupt. After Compound, the smart contract does the work. No custody risk. No human in the loop deciding who gets a loan. No CEO who can gamble your deposits on bad trades.

When BlockFi went bankrupt. When Celsius collapsed. When Voyager shut down. Compound kept running. Every block. Every second. The smart contracts did not panic. They did not freeze withdrawals. They did not run to Dubai. The protocol processed liquidations during the worst crashes in crypto history and came out with zero bad debt. That track record is Compound's real legacy.