What is CeFi? Centralized finance in crypto explained

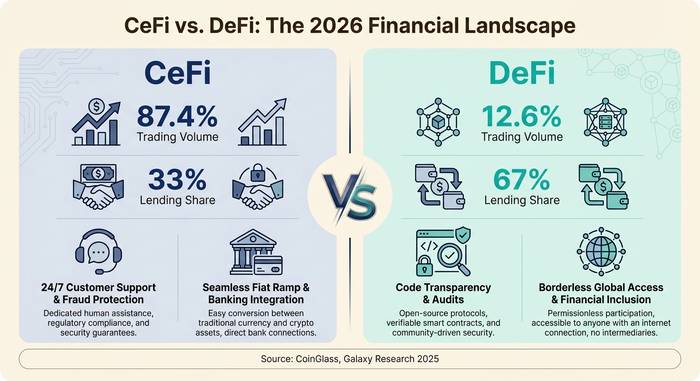

Binance processed $25 trillion in trading volume during 2025. Coinbase pulled in $7.18 billion in revenue. Centralized crypto exchanges handled 87.4% of all crypto trading volume. For all the talk about decentralization, the reality is blunt: most people interact with crypto through centralized companies.

CeFi is centralized finance. The part of crypto that feels like a bank. A company runs it. You sign up, deposit money, and the company holds your coins, runs your trades, and deals with everything technical. Coinbase, Binance, Kraken, Nexo. If you bought BTC on an exchange and left it sitting there, that was CeFi.

The CeFi versus DeFi argument never stops. DeFi people say: trust code, not companies. CeFi people say: my mom is not managing a seed phrase. Both are right. And the implosion of FTX, Celsius, and BlockFi in 2022 proved what happens when the "trust a company" model goes wrong.

Here is the full picture: how CeFi actually works, what it offers, where it beats DeFi and where it does not, and what changed after the industry nearly burned itself to the ground.

How CeFi works

Same mechanics as your bank, different asset class. Open an account. Verify your identity (KYC). Deposit money. The platform takes over.

When you hit "buy" on Binance, the trade does not actually touch the blockchain. It settles on Binance's internal ledger. An off-chain database matches your buy with someone else's sell in milliseconds. Way faster than on-chain. Way cheaper too. The exchange pockets a trading fee for the service.

Here is the part that crypto purists hate: the platform holds your private keys. That old line, "not your keys, not your coins," is not a metaphor. Your BTC on Coinbase belongs to Coinbase until you withdraw it to your own wallet. If Coinbase shuts down tomorrow, you are a creditor in bankruptcy court, not a Bitcoin holder.

That is the deal. You get a clean app, customer support, someone to call when things go wrong, and the ability to move between dollars and crypto without touching a blockchain directly. You give up control. For 580 million crypto users worldwide in 2025, that has been a trade worth making. Most people do not want to babysit a seed phrase. They want to tap a button and own Bitcoin.

What CeFi platforms actually do

CeFi covers a lot of ground. Think of it as five overlapping businesses, all run by companies.

Trading is the money machine. CEXs moved $81.57 trillion in 2025. Spot was $19 trillion. Derivatives crushed it at $62 trillion. Binance alone handles about 40% of spot and 35% of derivatives. Those are numbers that no DeFi protocol comes close to.

Lending is the second business. Nexo, Ledn, and Tether's institutional desk had $24.4 billion in outstanding loans by Q3 2025. You hand over BTC, you get dollars. Rates run 2.9% for Nexo's VIP tier up to 18.9% for basic accounts. Tether controls roughly 57% of the CeFi lending pie.

Yield products used to be the biggest draw. Celsius was offering 18% on deposits. Then it blew up. In 2026, yields are humbler: 3-8% on stablecoins, 1-4% on BTC. Nexo and Crypto.com still run earn programs, but nobody is promising 18% anymore.

Fiat conversion is where CeFi has no competition at all. You cannot buy ETH with a credit card on Aave. You need Coinbase or Binance for that. And when you want to cash out, you need them to wire dollars to your bank. DeFi cannot do this.

Custody rounds it out. The exchange stores your crypto. Cold wallets, multi-signature setups, insurance policies. Coinbase keeps most customer funds offline and carries crime insurance. Whether you trust that more than holding your own keys is a personal call.

| CeFi service | What it does | Examples | Market size (2025) |

|---|---|---|---|

| Trading (spot + derivatives) | Buy, sell, trade crypto | Binance, Coinbase, Kraken | $81.57T volume |

| Lending | Borrow against crypto collateral | Nexo, Ledn, Tether | $24.4B outstanding |

| Yield / earn | Earn interest on deposits | Nexo, Crypto.com | Rates 1-8% |

| Fiat on/off ramp | Convert between fiat and crypto | Coinbase, Binance, MoonPay | Embedded in exchanges |

| Custody | Secure storage of crypto assets | Coinbase Custody, BitGo, Fireblocks | Institutional-grade |

CeFi vs DeFi: where each one wins

This fight never ends. But instead of picking a side, look at where each one actually delivers.

CeFi owns ease of use. Download Coinbase. Tap "Buy Bitcoin." You are done. No seed phrase, no wallet setup, no staring at gas estimates. 560 million people own crypto. Most of them got in through CeFi because it felt normal.

CeFi owns trading volume. 87.4% of all crypto trading runs through centralized order books. Deeper liquidity. Tighter spreads. Big traders need CEXs because no DEX can absorb a $50 million market order without massive slippage.

CeFi owns fiat. Want to turn your paycheck into ETH? CeFi. Want to cash out to your bank? CeFi. DeFi has no good answer here.

DeFi owns lending. Two-thirds of all crypto loans live on-chain as of Q3 2025. Aave, Compound, Morpho. People shifted because the code is transparent, you do not need permission, and nobody can freeze your account.

DeFi owns transparency. Every trade on Uniswap is on-chain. Every Aave loan is visible. CeFi? Black box. You see your balance and hope the company is solvent. Post-FTX, that hope does not go as far as it used to.

DeFi owns access. No KYC. No country restrictions. A teenager in Nigeria can use Aave the same way a London hedge fund does. CeFi gates keep people out. DeFi gates do not exist.

| Metric | CeFi | DeFi |

|---|---|---|

| Share of trading volume | 87.4% | ~12.6% |

| Share of lending market | ~33% | ~67% |

| User experience | Easy, app-based | Complex, wallet-based |

| Fiat support | Yes | Limited |

| KYC required | Yes | No |

| Transparency | Opaque (trust-based) | On-chain (verifiable) |

| Customer support | Yes | No |

| Asset custody | Platform holds keys | You hold keys |

| Primary risk | Company failure | Smart contract bugs |

What happened when CeFi trust broke

2022 was the year CeFi almost destroyed itself.

FTX looked like the gold standard of crypto exchanges. Sponsors on MLB stadiums. Larry David in Super Bowl ads. Then November happened. Turns out SBF had been siphoning customer deposits into Alameda Research, his trading firm. $8 billion missing. Criminal conviction. 25-year sentence.

Celsius had been promising 18% yields while secretly lending customer money to counterparties like Three Arrows Capital. 3AC blew up. Celsius could not cover the hole. Withdrawals frozen in June 2022. Bankruptcy in July. Creditors got back about 65% over three painful rounds totaling $2.75 billion.

BlockFi, Voyager, Genesis: same dominoes, same crash, same contagion of interconnected bets and missing collateral.

Total body count: 4.3 million investors. $46 billion gone.

What came after? Proof of reserves. Binance, Kraken, OKX, Crypto.com all publish regular attestations now. The GENIUS Act passed in July 2025, giving the US its first real stablecoin rules. MiCA went live in Europe, requiring every crypto service provider to register by July 2026. These laws are not perfect. But the era of exchanges running with zero oversight is over.

The rule going forward: if a CeFi platform refuses to prove it has your money, it does not deserve your money.

The CeFi ecosystem in 2026

CeFi did not just survive. It got bigger. Coinbase put up $7.18 billion in revenue for 2025. Binance added 50 million new users in seven months. Nexo walked back into the US market in April 2025 carrying $11 billion in AUM.

Lending consolidated brutally. Tether, Galaxy, and Ledn now own about 90% of the CeFi loan book. Tether bought into Ledn in November 2025 to lock down the Bitcoin-backed lending niche. Everyone else either went bankrupt, got absorbed, or shrank to irrelevance. Nexo is the exception, holding $1.96 billion in outstanding loans.

Regulation actually showed up this time. GENIUS Act in the US. MiCA across Europe. These are real laws with real consequences. Reserve requirements. Mandatory audits. Criminal penalties for lying about solvency. CeFi platforms now have to behave more like banks. Some would say that is the whole point.

The exchange industry is projected to pull $85.75 billion in revenue in 2026. As long as people need a way to turn dollars into crypto and back, CeFi has a job.

Perfect? Not even close. You still hand your keys to a company. You still trust them. But the worst actors are gone, the survivors publish proof of reserves, and the regulators are actually watching this time.