Best Upcoming Crypto in 2026: The Next Big Cryptocurrencies and Tokens

Bitcoin's 2024 ETF approval did something the 2017 ICO boom and the 2021 NFT mania never could: it made the question "what's the next big crypto?" worse, not better. The spot Bitcoin ETFs now hold about 1.32 million BTC, roughly 6.3 percent of total supply, with cumulative AUM above $102 billion as of May 2026. When a single asset class absorbs that much institutional capital, the rotation pattern downstream changes. You can no longer screen for the next Bitcoin, because Bitcoin itself became the on-ramp. The cryptocurrencies that perform from here will not be the ones that look most like Bitcoin in a whitepaper. They will be the ones that capture flow when capital leaves the ETF wrapper and looks for productive uses on-chain. That is not a single coin trade. This piece does two things differently from the standard listicle. First, it maps where 2026 on-chain data actually shows revenue and liquidity rotating. Second, it gives you a five-step framework you can run yourself the next time the cycle changes.

Why "next big crypto" is the wrong question in 2026

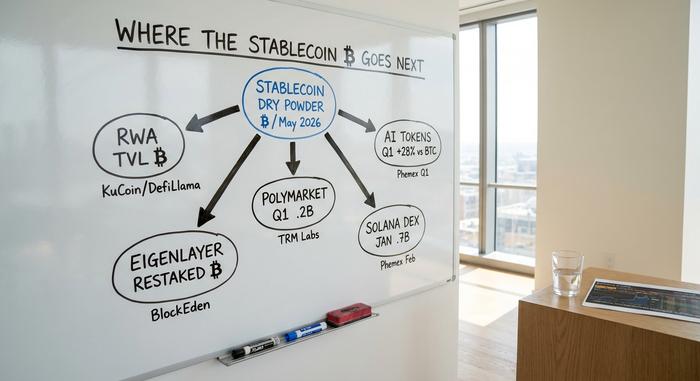

The listicle frame has a structural problem in 2026. Bitcoin dominance sits near 58 percent, the highest level in years, because spot ETFs absorb institutional flow that used to spill into the broader cryptocurrency market during prior cycles. The dry powder that would historically rotate into altcoins is now parked in stablecoins. Total stablecoin supply hit a record $320.6 billion in May 2026, with USDT at $185.5 billion and USDC at $78 billion, according to KuCoin and DefiLlama. That is the indicator to watch closely; the BTC price chart matters less right now, because stablecoin growth tells you how much capital is on standby waiting to deploy.

Developer activity tells the other half of the story. Crypto weekly code commits fell roughly 75 percent between early 2025 and March 2026, according to Electric Capital data summarised by CoinDesk. Ethereum still leads in absolute developer count at about 2,811, although that figure is down 34 percent year-on-year. BNB Chain dropped 85 percent. The talent did not retire; much of it migrated to AI repositories, and that migration is the sharpest evaluation signal we have. A chain losing developers is shrinking in slow motion even when its token chart looks flat.

Even the ETF tape has cooled. After a strong April with $2.44 billion of net inflows into US spot Bitcoin ETFs, May 2026 saw six consecutive days of outflows, and year-to-date net flows have compressed to about $536 million. The institutional bid is still there, but it is selective.

What this means in practice: the next outperformer is more likely to be a sector trade than a single-coin moonshot. The flow goes to whichever vertical can show on-chain revenue, real users, and tolerable token unlocks at the same time. That filter is narrow. It also rules out roughly 80 percent of what shows up on a "top crypto to buy" listicle.

Sectors where capital is rotating — RWA, AI, and Solana DePIN

Five sectors had verifiable 2026 on-chain revenue or total value locked that rose against the broader cryptocurrency markets. Narrative noise is one thing; on-chain numbers are another. The list below uses the second.

Real-world asset tokenization

RWA on-chain TVL crossed $20 billion in May 2026, up roughly three times since early 2025, according to Yellow.com research. Tokenized US Treasuries account for about $13.5 billion of that figure. BlackRock's BUIDL fund passed $500 million inside its first year, while Ondo Finance held its lead among native crypto-RWA issuers. The thesis is not subtle: blockchain technology that settles yield-bearing dollar exposure on-chain solves the most boring use case in crypto, and boring works during institutional cycles.

AI tokens

AI tokens were the only crypto sector that finished Q1 2026 in positive territory. The AI basket was down 14 percent while Bitcoin lost 23 percent and Ether dropped 32 percent, per Phemex data. The standout is Bittensor (TAO), which booked $43 million in Q1 revenue against a roughly 20x price-to-revenue multiple, high but not absurd against software comparables. Render Network (RENDER) and Fetch.ai (FET, recently merged into the Artificial Superintelligence Alliance) round out the basket. The shared trait is that all three can point to actual users paying for compute.

Solana DEX activity

Solana processed $117.7 billion in DEX volume during January 2026, about 35 percent of all on-chain volume that month, and total Q1 transactions came in at 126 times Ethereum's count. The 21Shares spot Solana ETF received SEC approval in early 2026, the first US spot ETF for a smart contract platform other than Ethereum. Firedancer, the second validator client, remains the technical catalyst for the year because it pushes the network toward its 1 million TPS target. Solana's proof-of-history timestamping is the blockchain design choice that makes that throughput plausible.

Prediction markets

Polymarket recorded $26.2 billion of trading volume in Q1 2026, up 90 percent quarter-on-quarter, and March became the first month above $10 billion. A year earlier the platform was running about $1.2 billion a month, a 17x expansion in twelve months. TRM Labs flagged prediction markets as the fastest-growing on-chain vertical of the first half of 2026.

Modular L1s and restaking

EigenLayer crossed $18 billion in restaked ETH with 1,900 operators as of February 2026, although the figure bounces with the ETH price. BlockEden later flagged a March pullback to $8.9 billion as repricing rather than withdrawals. Across L2s, Arbitrum and Base together hold 77 percent of the $48 billion combined TVL, leaving Optimism, ZkSync, and the long tail to share the rest.

| Sector | Key metric | Value | As of |

|---|---|---|---|

| RWA tokenization | On-chain TVL | $20B+ | May 2026 |

| AI tokens | Q1 sector return | -14% (vs BTC -23%) | Q1 2026 |

| Solana DEX | January volume | $117.7B | Jan 2026 |

| Prediction markets | Q1 volume | $26.2B | Q1 2026 |

| Restaking (EigenLayer) | Restaked ETH | $18B (Feb) / $8.9B (Mar) | Q1 2026 |

Contender cryptocurrencies — BTC, ETH, XRP, and Cardano

If you want a concrete shortlist, and most readers eventually do, here are eight names that show up across every serious 2026 watchlist, framed by sector role rather than price-target ranking. Each entry pairs the coin with one verifiable 2026 catalyst and one risk flag, because catalysts alone are how listicles get written and risk flags are how readers stay solvent.

Bitcoin (BTC) remains the store-of-value layer and the original digital currency benchmark. The 21 million supply cap is the only piece of scarcity logic that has survived four cycles, and the ETF wrapper makes that scarcity legible to allocators who would never touch a hardware wallet. The halving cycle still functions; the 2024 event tightened issuance on schedule, even if the price reaction now lags ETF flow rather than retail.

Ethereum (ETH) is the smart contract base layer. Its L2 ecosystem holds about $48 billion in combined TVL, the Pectra upgrade improved validator economics and bandwidth, and the restaking layer is now mature enough to host a separate $18 billion market. The risk: ETH price has lagged its own ecosystem TVL for two years, and that gap is unresolved.

Solana (SOL) earned the 2026 ETF approval and the DEX volume crown. Firedancer pushes the network toward 1 million transactions per second, well past what any payment use case currently demands. The honest concern is validator concentration and the dependency on a single team's roadmap.

XRP cleared the SEC overhang in August 2025 with a $50 million settlement. Ripple Labs now sits inside the US strategic crypto reserve, alongside Bitcoin and Ethereum, which functionally legitimises XRP for cross-border payments use. Banks will move slowly, but the regulatory blocker is gone.

Cardano (ADA) carries the peer-reviewed development reputation and the strategic-reserve inclusion, although its dev activity and DeFi traction lag its market cap. ADA is the contender most exposed to the developer-drain trend.

Chainlink (LINK) is the oracle backbone for RWA tokenization. The US Department of Commerce partnership in August 2025 and the LINK spot ETF approval in January 2026 changed how the market thinks about oracle infrastructure: critical national stack, not just decentralized finance plumbing.

Monero (XMR) is the contrarian leg. As MiCA 2 in the EU and the FATF Travel Rule expansion tighten on-chain analytics, the privacy hedge becomes structurally rarer. XMR delistings on regulated exchanges are themselves the bull case if you read them inversely.

Bittensor (TAO) is the speculative outlier worth naming. The 21 million cap mirrors Bitcoin's scarcity model, the subnet revenue is verifiable at $43 million for Q1, and the price-to-revenue multiple is the open question.

| Coin | Sector role | 2026 catalyst | Risk flag |

|---|---|---|---|

| BTC | Store of value | $102B+ ETF AUM | Cycle compression |

| ETH | Smart-contract base | Pectra + restaking | Price lags TVL |

| SOL | High-throughput L1 | 21Shares ETF approved | Validator concentration |

| XRP | Cross-border payments | SEC settled Aug 2025 | Bank adoption lag |

| ADA | Peer-reviewed L1 | Strategic reserve inclusion | Dev activity lag |

| LINK | RWA oracle | DOC partnership + LINK ETF | Fee-share concentration |

| XMR | Privacy hedge | Regulatory delisting bull case | Exchange access |

| TAO | AI compute | $43M Q1 subnet revenue | Multiple vs hype |

A framework to evaluate the next big cryptocurrency

The shortlist above will be obsolete in eighteen months. The framework that produced it will not. Five quantifiable screens, each runnable on free or cheap tools.

Start with on-chain revenue, since promises are cheap. DefiLlama publishes daily fee revenue including transaction fees, and TokenTerminal calculates price-to-fees multiples for the major chains and protocols. The signal here is unambiguous: when a token's market capitalization implies $500 million in annual fee equivalent but the protocol generated $4 million last year, the math is broken or the multiple is pre-narrative. Both can be correct; only one is investable.

Token unlock overhead comes next. The 2026 unlock calendar is heavy. Arbitrum's vesting tranches, several Aptos and Sui cliffs, and a number of restaking-derivative tokens unlock significant supply against thin buyer interest. CryptoRank and TokenUnlocks publish dated schedules. The mechanism is simple: while monthly supply expansion exceeds monthly new buyer demand, the price-discovery direction is already set.

Developer activity trajectory matters more than it did a year ago. Electric Capital's monthly reports remain the cleanest data on this. Because the sector-wide -75 percent commit decline is now baseline, the outliers carry more signal weight than they did in 2024. Solana's developer count grew while the average shrank. Base's ecosystem expanded as a sub-network of Ethereum. Bittensor subnets aggregated independent teams under one revenue umbrella. Where developers are still showing up, the long-term bid still functions.

The fourth screen is tokenomics and validator distribution. Supply cap is a starting point; vesting cliffs, treasury holdings, and validator concentration matter more in 2026 than they did when proof-of-work blockchains dominated. For a proof-of-stake network, ask: how many independent validators hold a meaningful stake, what proportion of supply sits in foundation or insider wallets, and what is the realistic decentralization measured by Nakamoto coefficient? Decentralized applications running on top of those validators inherit whatever risk the validator set carries.

Smart-money wallet tracking closes the list. Nansen and Arkham publish methodology for aggregating on-chain flows from labelled cohort wallets: venture funds, market makers, treasuries. The trap is copying individual wallets, since their entries get front-run and their exits get screenshotted. The use case is aggregate flow: which sector are smart-money clusters net-buying this month? That number is more honest than any analyst thesis.

I keep coming back to point one. Most candidates fail it. A protocol that cannot show fee revenue or a near-term path to fee revenue is a beta trade on the broader cryptocurrency market, not an idea. The market is impatient about that distinction in 2026 in a way it was not in 2021.

Hidden risks — meme coins, unlocks, and stablecoins

Three failure modes are responsible for most "next big crypto" disappointments. None of them is exotic.

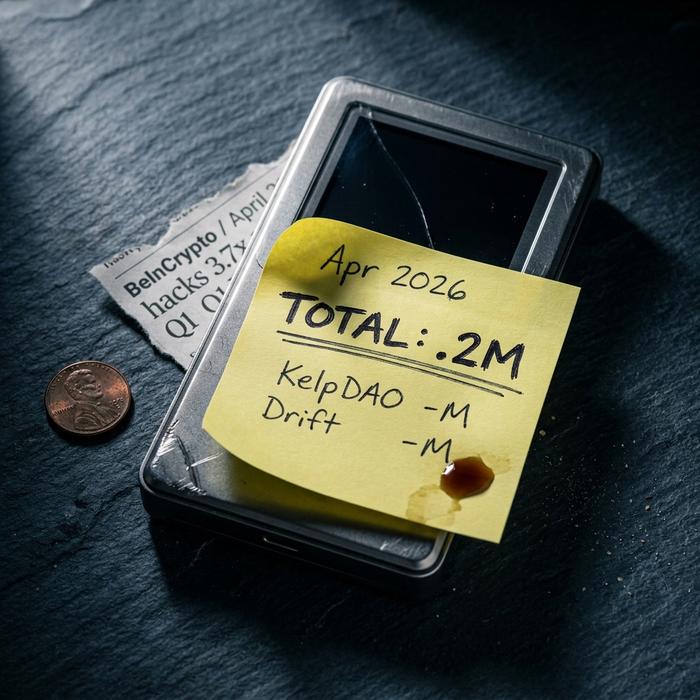

The first is exploit risk concentrated in newer infrastructure. April 2026 alone saw $606.2 million in crypto hack losses, 3.7 times the entire Q1 figure, and two events accounted for 95 percent of that: a $290 million KelpDAO incident and a $285 million Drift exploit, per BeInCrypto. Restaking layers and perp DEXs are concentrating risk in code that has not been battle-tested across a full cycle.

The second is the meme coin lottery. A token at a fraction of a cent feels accessible, and Dogecoin reaching 73 cents in 2021 is the screenshot that funds the dream. Dogecoin sat at 13 cents by mid-2024 with no fundamental change in supply schedule. Memecoins are extreme-volatility instruments; treating them as scarcity bets confuses unit price with circulating supply.

The third is regulatory whiplash. The GENIUS Act takes effect in January 2027 and reshapes the US stablecoin compliance perimeter; MiCA 2 in the EU and the Securities and Exchange Commission's evolving framework move the goalposts for tokenized assets. The hedge against inflation pitch — including the argument that crypto outperforms fiat over multi-year periods — survives intact, although the operational reality of running compliant services around it does not. Energy-intensive proof-of-work mining is a separate regulatory front to track.

The smart-money crypto playbook for 2026

If you want one paragraph: hold core crypto assets — specifically BTC and ETH — for store-of-value and base-layer beta. Rotate satellite exposure across two or three sectors where 2026 on-chain revenue is verifiable — currently RWA tokenization, AI tokens with paying users, and prediction markets. Watch stablecoin supply growth as the rotation timing signal; when $320 billion starts deploying meaningfully, the sector that absorbs it first wins the trade. Exit any individual position when developer activity diverges from price, because that gap closes downward. Buying and holding is still the dominant strategy for the top cryptocurrencies; sector rotation matters at the satellite layer, not at the core. Most of this just requires not getting frontrun by your own narrative.

Conclusion: where the next big crypto really comes from

The listicle question of "what's the next big crypto" dies a quiet death in 2026. A better one replaces it: which sector compounds on-chain revenue while the cycle digests $320 billion in stablecoin dry powder, and which tokens within that sector survive the next unlock cliff with their developer base intact. Watch flows, not Twitter threads. The cryptocurrencies that earn their place this cycle will not announce themselves; their fee revenue will.