FCFS Meaning Explained: First-Come, First-Served in Crypto

On the launch day of the TRUMP memecoin in January 2025, one wallet bought 5.97 million tokens at the very first block for $1.09 million and walked away with roughly $109 million in profit, using $80,000 in Solana priority fees to guarantee block-zero inclusion. That is what "first come, first served" looks like in 2026 crypto. The bot came first, the bot got served, and a few hundred thousand retail buyers got the leftovers a few blocks later. FCFS is still the most popular launch model in crypto. It is also the one most consistently captured by automation. This guide explains what FCFS actually means, where the term came from, how it plays out in modern crypto launches, and what alternatives are starting to work.

What does FCFS mean in plain English?

FCFS stands for First-Come, First-Served, sometimes written as FCFS scheduling when the term refers to the scheduling algorithm specifically. The principle is the simplest scheduling rule in existence: whoever arrives first gets served first. No priority, no lottery, no committee. Just arrival order. It is the discipline behind a corner-shop queue, a deli counter, an emergency-room triage in a non-critical case, and the line outside a sneaker drop. The term originated in computer science as an operating-system scheduling algorithm and then leaked outward into logistics, freight, customer service, and eventually crypto. In every context, the appeal is the same: it feels fair because nobody gets special treatment. The catch, also the same, is what we will get to in the rest of this article.

FCFS scheduling: where the term actually comes from

The original FCFS lives in operating systems. It is the first scheduling algorithm any computer-science student meets — a non-preemptive scheduler that pulls each process off a FIFO queue in the order they arrive. In CPU scheduling, the FCFS algorithm becomes the baseline against which more advanced schedulers (SJF, Round Robin, priority queues) are measured. Simple to implement, easy to reason about, and fair by construction. The well-known flaw is the convoy effect: a short job stuck behind a long job has to wait, which can wreck average turnaround time. The OS scheduler does not know that the short job is more urgent. It only knows arrival order.

The same logic shows up in freight and warehouse operations. A facility running FCFS at its loading docks unloads trucks in the order they arrive, with no scheduled appointment. Carriers can roll up any time during opening hours and join the queue. The advantage is flexibility for drivers and lower coordination overhead for the warehouse manager when handling routine shipping and delivery flows efficiently. The disadvantage is long wait times when multiple trucks arriving together pile up, no priority for time-sensitive shipments, and a brittle dependency on efficient dock turnaround. The impact on truck drivers stuck in long wait times at FCFS facilities is lost money on hours-of-service compliance. Shippers pay more in detention costs. The standard solution most logistics teams adopt is a hybrid appointment model, since pure FCFS rarely scales when resource constraints tighten. The trade-offs are well-documented across the supply chain industry, and they map almost perfectly onto the crypto version.

How FCFS works in crypto token launches

In crypto, FCFS is the structure of a public sale or mint where the contract opens at a specific time and allocation goes to whoever's transaction is included first. There is no whitelist, no lottery draw, no committee approval. Anyone with the contract address and enough money can try. The structural truth most explainers skip is this: "first" never means "first human to tap a button". It means "first transaction the validator chose to include in a block".

That distinction is the whole story. On Ethereum L1, transaction priority is set by an open gas-price auction. The transaction with the highest gas fee wins inclusion. After the Dencun upgrade in March 2024 and Pectra in May 2025, average ETH gas collapsed from 72 gwei to about 2.7 gwei, and a typical NFT mint went from $145 to under a dollar. But the auction mechanic is unchanged. When a hot mint opens, the auction reopens at full intensity, and the bots paying the highest gas still win.

On Solana, the equivalent mechanism is Jito's priority-fee system. Validators sort the mempool by tip size. A bot willing to pay $80,000 in tips for one block, as on the TRUMP launch, gets that block. Pump.fun's bonding-curve launches sit at the extreme end: no presale, no vesting, 80% of liquidity goes to the bonding curve, 20% to the creator, and anyone can buy from block one. The model is FCFS in its purest form, and the result is exactly what game theory would predict. Bots win, every time, by milliseconds.

The convoy effect from the OS textbook is alive in both ecosystems. Retail users, the equivalent of short jobs in the FCFS queue, are stuck behind larger, automated traders. They show up on time, they have enough money, and they still lose, because the bots arrive a few milliseconds before they do.

The 2024-2026 FCFS hall of shame

The case studies below are not cherry-picked. They are the standard outcomes of FCFS at scale. The table summarizes the impact, then each case gets a paragraph.

| Launch | Date | Chain | Outcome | Loss |

|---|---|---|---|---|

| Doodles public mint | Oct 2021 | Ethereum | 90%+ failed transactions | ~$1.26M wasted gas |

| Otherside (Yuga) | Apr 2022 | Ethereum | Chain stalled hours | $150M+ in gas |

| Azuki Elementals | Jun 2023 | Ethereum | Floor -30–40% in 24h | -$11M+ paper loss |

| TRUMP memecoin | Jan 2025 | Solana | Bot bought block 0 | $109M extracted by 1 wallet |

| Pump.fun aggregate | 2024–2025 | Solana | 84% sniped in 5 sec | 65%+ of liquidity to bots |

| PENGU (Pudgy Penguins) | Dec 2024 | Solana | Claims portal DDoSed | -88% from peak |

Doodles public mint (October 2021). 13,000 mint attempts from roughly 10,000 wallets. More than 90% of those transactions failed because they were outbid in the gas auction. Roughly 335.2 ETH (about $1.26 million at the time) was spent on failed gas alone, money that bought literally nothing. Successful mints paid a median of 4.0 ETH in gas. The collection itself was solid; the mint mechanic incinerated millions of dollars in user funds.

Yuga Labs Otherside land sale (April 30, 2022). 55,000 NFTs sold in roughly three hours, with participants collectively burning more than $150 million in Ethereum gas fees. The chain was effectively stalled for hours. Yuga itself called the mint "a learning experience".

Azuki Elementals (June 2023). Sold out in 15 minutes for $38 million in revenue. The floor price fell 30–40% within 24 hours. The FCFS rush rewarded speed at mint and immediately punished holders.

TRUMP memecoin (January 2025). One wallet bought 5.97 million tokens in block zero for $1.09 million, then sold for approximately $109 million in profit. Cost of the priority fees that secured the block: $80,000. A single transaction extracted more value than 99% of the launches that year combined.

Pump.fun aggregate, 2024–2025. A 300-launch on-chain sample showed sniper-bot activity within the first five seconds of 84% of launches. Bots captured more than 65% of initial liquidity, leaving retail with 15–25%. Across the platform, only 0.63–1.4% of tokens graduate from the bonding curve to Raydium, and 30–50% of new tokens are dumped by bots within five minutes of launch.

PENGU (Pudgy Penguins, December 17, 2024). 4.7 million site visits in the first hour. The claims portal was DDoSed. Market cap peaked above $2 billion in the first weeks and then fell roughly 88% from peak. Most of the people who tapped "claim" the hardest were the ones who lost the most.

Why FCFS keeps failing fair launches

The pattern repeats because pure FCFS is structurally inefficient for public token launches, not a result of any specific project getting the design wrong.

Mechanically, blockchain block times plus general-purpose automation guarantee that bots always win the milliseconds race. A retail buyer with a fast finger and a desktop browser is competing with software running in a colocated server next to a validator. That race is already over.

Economically, every "fair" priority-fee auction is a pay-to-win FCFS layered on top of an arrival-order FCFS. The pretense is order; the reality is capital. Whoever can pay the most for guaranteed block inclusion gets the allocation.

The macro evidence is hard to argue with. According to Memento Research and CryptoRank, 85% of all 2025 token launches traded below their issue price; the median fully diluted valuation dropped 71% from TGE; only 12% of token sales stayed above launch valuation. 11.56 million tokens failed in 2025 alone, about 86% of all crypto token failures since 2021 in a single year. FCFS launch design is one contributor to that wreckage, not the only one, but a consistent one.

There is also a network-level externality that is worth mentioning. On Solana, arbitrage-bot failed transactions consume roughly 40% of total compute units while paying only 7% of fees. The losing side of every FCFS race is paying the network in opportunity cost, and the cost gets spread across everyone else trying to use the chain at the same time.

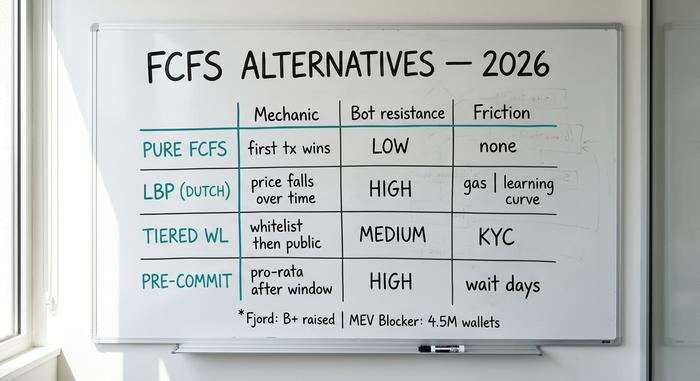

FCFS alternatives that are starting to work

Not all FCFS designs are equal, and the last two years have produced credible alternatives.

Liquidity Bootstrapping Pools (LBPs). Fjord Foundry, the successor to Copper, runs Balancer-style LBPs where the token's starting price is high and falls over the sale window unless buyers push it up. The mechanic actively penalizes sniping because the early buyer pays the worst price. Through 2026, Fjord has facilitated more than $1 billion in raises across 100-plus IDOs, with about $1.5 billion in trading volume and 100,000 participants. It is not perfect, but it removes the millisecond race.

Tiered FCFS with whitelisting. A whitelist round restricted to vetted wallets opens first, then a public FCFS round for the remainder. Adds KYC friction and a curation step, but does more to minimize bot capture than any pure-FCFS design.

Pre-commit blind allocation. A deposit window opens for a defined period (24 hours, a week). At the end, allocation is calculated pro-rata or by lottery from all deposits. There is no race to enter and no advantage to arriving in the first millisecond.

MEV protection for participants. On Ethereum, Flashbots Protect has shielded $43 billion in DEX volume across 2.1 million accounts since 2021, and more than 50% of all Ethereum gas now flows through private mempools. MEV Blocker, run by CoW Protocol, has paid back 6,177 ETH in rebates to 4.5 million wallets and protected $60 billion in DEX volume. These tools do not stop FCFS bots from winning the launch race, but they do stop ordinary swaps from being sandwiched. On Solana, no equivalent retail-grade MEV protection has reached scale yet, which is part of why FCFS launches there are so bot-dominated.

How to actually participate in an FCFS launch

For retail users determined to try anyway, a short checklist beats hopium.

Use Flashbots Protect RPC or MEV Blocker on Ethereum-side launches. Pre-fund the wallet with the exact purchase amount plus a comfortable gas headroom. Pre-sign any token approvals the contract requires, well before the launch window opens. Avoid the default RPC endpoint of a popular wallet during a hot launch; Infura or Alchemy public endpoints are congested precisely when you most need throughput, so run your own RPC or use a private one. On Solana, the same idea applies: pay for a private RPC and build in a priority-fee buffer that lets you bid into the Jito tip range without being mechanically outbid by serious bots.

Before clicking buy, run through the scam-launch checklist: contract verified on-chain, team doxxed or KYC'd through a reputable launchpad, no insider unlock cliff under 30 days, liquidity locked for at least six months. If any of these fail, the launch is hostile by design.

Set a maximum loss tolerance before you click buy. Most FCFS launches lose money for retail in 2026, and treating the buy as a gamble rather than an investment is the only intellectually honest framing.

Regulatory pressure reshaping FCFS launches

2026 is the first year regulators are arriving at the FCFS party. The EU's MiCA framework reaches full enforcement on July 1, 2026. After that date, anonymous IDOs are effectively banned across the EU; any public token offering above €1 million or with more than 150 participants must publish a compliant whitepaper and operate through an authorized Crypto-Asset Service Provider.

In the United States, the SEC and CFTC issued a joint clarification on March 17, 2026 classifying BTC, ETH, SOL, and XRP as digital commodities, with parallel guidance tightening the disclosure trail for token issuers. The practical effect is straightforward: more launches move to KYC'd platforms with vetted wallets, fewer pure-FCFS public sales target US-resident retail directly, and the offshore long tail (still significant) keeps doing what it has always done.

The bottom line on FCFS in crypto

FCFS sounds fair. It rewards the fastest, and in 2026 the fastest are bots, not humans. For participants, the lesson is simple: the FCFS race is not competitive for retail without MEV protection, and any launch should be treated as a high-variance bet rather than an investment. For projects, pure FCFS in 2026 is a marketing choice, not a fairness one. Hybrid models — whitelisted tiers, LBPs, pre-commit allocation — are more honest about who they actually serve, and the data on token survival rates suggests they produce better outcomes for everyone except the bots.