Top 10 Weakest Currencies in the World 2026 Ranked

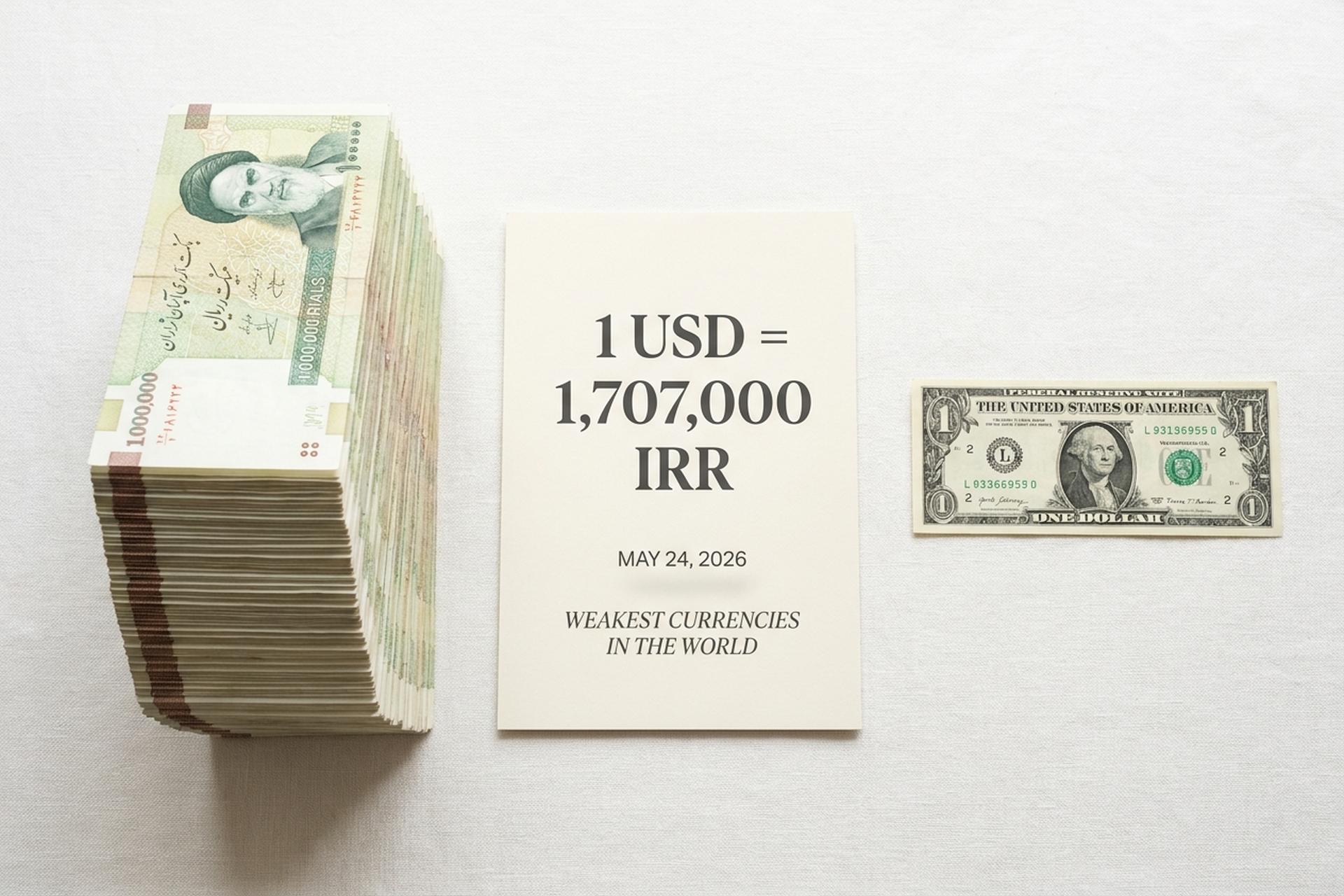

A friend asked me last week which currency was actually weakest right now. I said Iranian rial without hesitating. He pulled out his phone, opened a currency-converter app and laughed — one dollar bought him 1.32 million rials at the official rate. Then I showed him alanchand.com, where the same dollar on May 24, 2026, fetched roughly 1.7 million rials at the parallel street rate. That 30 percent gap between official and parallel is what a weak currency looks like up close.

So here is the actual ranking. This piece walks the ten weakest currencies by their nominal exchange rate to the US dollar in 2026. Each entry carries a current rate, the latest inflation figure, and the named macroeconomic driver pushing it down. The US dollar index closed at 98.96 on May 25, 2026, down roughly 11 percent over the first half of 2025. Even a softer dollar did not rescue the bottom of the table.

After the ranking, three honorable mentions: Argentina, Venezuela, and Turkey. These currencies are weak by dysfunction rather than by nominal value alone, and they belong in their own frame. The closing section is a short reminder that weak does not always mean poor.

What makes a currency the weakest in the world?

Most listicles use the same yardstick. Nominal exchange rate to the dollar. More units per dollar, weaker currency. Clean screen. Misleading screen. Japan's yen trades around 150 to the dollar. Nobody calls Japan weak.

Weimar Germany is the textbook. The mark slid from 320 per dollar in mid-1922 to 4.2 trillion per dollar by November 1923. War reparations. Debt monetization. A Reichsbank that would not stop printing. Modern currency collapses rarely have one cause. They tend to combine several. High inflation, sometimes hyperinflation. International sanctions cutting off access to foreign currencies. Political instability scaring off investors. A central bank that lost its independence. Commodity dependence with limited economic diversification. Foreign-debt overhang. Trade deficits that drain reserves faster than exports refill them.

A country can also depreciate on purpose. Vietnam has kept the dong weak since the 1980s to keep its factories competitive. That is policy, not collapse. The table below mixes both kinds, and the reader has to keep them separate.

Iranian Rial (IRR): the weakest currency in the world

Walk through a Tehran bazaar in mid-2026 and the official price tags mean almost nothing. Vendors quote in dollars, in millions of rials, sometimes in gold. On May 24, the Central Bank of Iran posted 1,317,000 IRR per dollar; on the same day, the parallel rate quoted by alanchand.com was around 1,707,000. That 30 percent premium is not a glitch. It is the operational reality for most Iranian businesses, and it is what I think about when I see the word "weakest" used loosely about other currencies. None of them is in this league.

CPI ran at 62.2 percent year-on-year in February 2026, per Iran International and the IMF DataMapper. The IMF projects 68.9 percent for the full year. Food inflation is closer to 99 percent. The drivers are concentrated: international sanctions after the nuclear deal collapsed, ongoing Middle East tensions, and a wartime risk premium that does not let the rial breathe. The Iran-US negotiations Axios reported in May 2026 are at the "one-page memo" stage. That is the only realistic catalyst for any reversal in the near term, and even optimists do not expect quick relief.

Lebanese Pound (LBP) and the post-2019 collapse

In 2019, a Beirut shopkeeper could swap 1,500 lira for a US dollar at any corner bureau de change. By May 2026, the same dollar costs about 89,500 lira. That is a 98 percent loss in less than seven years, and unlike Iran's split rates, the official and parallel rates have largely converged. This is not the convergence of reform. It is the convergence of capitulation.

What broke was the banking system itself. The cascade began in October 2019, when depositors discovered they could no longer freely access dollar accounts, and it never resolved. The World Bank's 2026 country update puts cumulative banking-sector losses at around $72 billion. Inflation cooled from triple-digit prints in 2023-2024 to a rough 30-50 percent range in 2026 under IMF program pressure. The political instability that prevented an earlier stabilization remains structural, and that is the part the headlines undersell.

Vietnamese Dong (VND): managed weakness by design

Vietnam is the case most "weakest currency" lists muddle. The dong traded at roughly 26,361 per US dollar on May 25, 2026 according to Trading Economics. Inflation sat in the 4 to 5 percent range, far from a crisis number. Vietnam's GDP growth has averaged above 6 percent for two decades. So why is the dong in the bottom ten?

Because the State Bank of Vietnam wants it there. The dong has been kept deliberately weak since the 1980s to keep manufacturing exports competitive against regional rivals. As the country's currency of issue, it remains the official currency for taxes and salaries inside Vietnam, and locals get paid in dong without treating that as a sign of distress. This is a managed currency, not a damaged one. The same logic explains why several large emerging-market economies appear high on these lists while running perfectly healthy growth.

Sierra Leonean Leone after the 2022 redenomination

Pop quiz: is the Sierra Leonean leone the fourth-weakest currency in the world or somewhere in the middle of the pack? The answer depends on which code your source uses. In 2022, Sierra Leone redenominated its currency, knocking three zeroes off the old leone. The legacy SLL priced the old basis at around 22,000 per dollar. The new SLE prices the same value at about 22.85. Different lists rank Sierra Leone differently for exactly this reason.

The Bank of Sierra Leone treats the new SLE as the official quote going forward, and the IMF's 2026 country report sees single-digit inflation ahead. Whether the leone ranks fourth or twentieth in 2026, the structural drivers have not changed: post-conflict economic recovery, a weak export base, limited industrial diversification.

Laotian Kip (LAK): inflation and fiscal stress in 2026

Lao Kip is one of those currencies most Western readers have never seen quoted, yet it sits high on the bottom-ten list almost every year. The kip traded at roughly 21,972 per US dollar in mid-2026 per the Global Economy database. Inflation re-accelerated to 10.2 percent in April, and over the past decade the kip has lost about 172 percent of its value against the dollar.

What is dragging it down right now is fiscal. East Asia Forum flagged in May 2026 that Laos needs a fiscal reset to handle a rising foreign-debt load while protecting social spending. Small developing economies that depend on imports and carry heavy external debt get squeezed first when global financing conditions tighten. Laos sits squarely in that group, with no obvious near-term lifeline.

Indonesian Rupiah (IDR): legacy of the 1997 crisis

Indonesia is the paradox in pure form. The rupiah traded between 17,420 and 17,704 per dollar in May 2026, down roughly 8.97 percent year-on-year per Trading Economics data, while inflation stayed moderate at 3 to 4 percent. This is a G20 economy with a four-digit USD exchange rate. Both facts are true at the same time.

The historical reason is the 1997 Asian Financial Crisis, which triggered a devaluation the rupiah never fully reversed. Recent capital outflows under political uncertainty have kept the floor moving lower. The rupiah looks weak by nominal rate, but the underlying economy continues to grow. Most retail watchers conflate the two and miss the gap.

Uzbekistani Som (UZS) and the post-Soviet currency arc

Trade Uzbekistani som at a Tashkent bank and you will pay somewhere between 11,861 and 13,000 per dollar in May 2026. Interfax reporting from the Uzbek central bank projects inflation to slow toward 7 percent through the year. The som is on every weak-currency list because of its nominal value, but the country has steadily liberalized its FX market since 2017 and the trajectory is constructive.

The deeper driver is the post-Soviet structural inflation that several Central Asian economies inherited at independence in 1991. Uzbekistan exports gold, cotton, and natural gas. The export base is concentrated, the import bill is heavy, and the local currency has never recovered its early-1990s footing.

Guinean Franc (GNF) — resources without diversification

Guinea is the resource-curse case on this list. The franc traded around 8,772 per dollar through 2026, with inflation last printed at 3.7 percent in August 2025. By the standards of the bottom-ten, those numbers are almost calm. Yet the franc stays weak, because the weakness is structural rather than acute.

Bauxite and iron ore leave Guinea as raw material. The value-add accrues elsewhere — in Chinese smelters, in European steel mills, in supply chains that price aluminium and steel in dollars and not in francs. Political instability has compounded the issue. The country has been under military rule since the September 2021 coup, and the foreign investment that left then has not returned at the pace it departed.

Paraguayan Guarani (PYG): South America's outlier

Paraguay belongs in the awkward category of "stable economy, weak currency". The guarani trades between 6,619 and 7,980 per dollar in 2026, while inflation has stayed in the 3 to 4 percent range. Bloomberg reports the central bank held its benchmark interest rate at 5.5 percent in April, which is a deliberately stable monetary stance.

So why is the guarani on this list at all? Mostly because of long historical depreciation against the dollar rather than any current crisis. Counterfeiting has been a documented operational issue in the country. The economy depends on soy and beef exports, which means the guarani follows global commodity cycles more than its own monetary policy.

Malagasy Ariary (MGA): vanilla, climate, and politics

If you have used a bottle of vanilla extract recently, you have been touched by Madagascar's monetary problem. The island grows about 80 percent of the world's vanilla beans, and that single fact explains more about the ariary than any monetary statistic. When vanilla prices collapse — and they do, periodically, savagely — Madagascar's foreign-exchange earnings go with them.

Trading Economics had the ariary between 4,325 and 4,652 per dollar in 2026, with inflation hovering around 7 to 8 percent. Cyclones have repeatedly damaged the agricultural base; the political instability dating back to the 2009 coup never gave the central bank a stable hand to play. So the ariary becomes the cleanest case study on this list of a currency that absorbs natural-disaster shocks and political-cycle volatility at the same time. Not unusual for an island economy. Just unusually concentrated.

| Rank | Currency | Code | Rate per USD (May 2026) | Inflation 2026 | Primary driver |

|---|---|---|---|---|---|

| 1 | Iranian Rial | IRR | ~1,317,000 official / 1,707,000 parallel | 62.2% YoY | Sanctions, war risk |

| 2 | Lebanese Pound | LBP | 89,500 | 30-50% | Banking collapse |

| 3 | Vietnamese Dong | VND | 26,361 | 4.5% | Managed depreciation |

| 4 | Sierra Leonean Leone | SLL / SLE | 22,850 (old) / 22.85 (new) | Single digit | Post-conflict, redenomination |

| 5 | Laotian Kip | LAK | 21,972 | 10.2% | Fiscal stress |

| 6 | Indonesian Rupiah | IDR | 17,420-17,704 | 3-4% | 1997 legacy + outflow |

| 7 | Uzbekistani Som | UZS | 11,861-13,000 | 7% | Post-Soviet structural |

| 8 | Guinean Franc | GNF | 8,772 | 3.7% (Aug 2025) | Political instability |

| 9 | Paraguayan Guarani | PYG | 6,619-7,980 | 3-4% | Nominal anchor |

| 10 | Malagasy Ariary | MGA | 4,325-4,652 | 7-8% | Vanilla, climate, politics |

For context, here is how the bottom of the table compares to the strongest currencies in the world. Three Gulf states with oil-backed pegged regimes anchor the top of the list, each trading at less than half a unit per dollar.

| Bottom 3 (May 2026) | Code | Rate per USD | Top 3 strongest | Code | Rate per USD |

|---|---|---|---|---|---|

| Iranian Rial | IRR | ~1,317,000 | Kuwaiti Dinar | KWD | 0.31 |

| Lebanese Pound | LBP | 89,500 | Bahraini Dinar | BHD | 0.38 |

| Vietnamese Dong | VND | 26,361 | Omani Rial | OMR | 0.38 |

The spread between the strongest and weakest currencies stretches across roughly four million times — a measure of how much exchange-rate regimes diverge across the global market.

Honorable mentions — Argentina, Venezuela, Turkey

Three currencies belong in a separate frame. They are not on the official list above because their weakness is functional rather than nominal, and they tell us something the nominal table cannot.

Argentina first. The peso traded around 1,401 per dollar in May 2026 per Trading Economics, with inflation at 31.8 percent year-on-year in November 2025. That headline number is a seven-year low under President Milei's reform program. Two years ago the peso would have placed near the top of any weakest-currency list, per Funds Society and Michigan Journal of Economics commentary. The trajectory now matters more than the level.

Venezuela tells a different story entirely. The bolívar remains in informal hyperinflation in 2026, but the more revealing data point is that the population stopped using it where possible. CNBC and LiveBitcoinNews put USDT stablecoin transaction volume inside Venezuela at roughly $44.6 billion in 2025. Around 80 percent of oil revenue now routes through stablecoins rather than the official banking system. On paper the bolívar is the official currency. In practice the dollar-pegged stablecoin is the operational one, which is the most interesting non-fiat experiment running anywhere in 2026.

Turkey closes the trio. The lira sits at roughly 38 to 40 per dollar after years of unorthodox monetary policy under President Erdogan. The central bank reversed direction in 2024 and the lira has stabilized somewhat, but the structural devaluation accumulated since 2018 will take a decade to undo. Annual inflation in Turkey was still running near 38 percent in early 2026 per Trading Economics, well above the central bank's official target.

Why a weak currency does not mean a weak economy

Nominal exchange rate is the most-cited and least-informative metric out there. The thread running through this whole list is exactly that gap. Vietnam ran above 6 percent GDP growth for two decades. The dong stayed weak by design. Indonesia is a G20 economy with a four-digit rupiah. Japan's yen sits at 150, nobody complains. What actually matters for citizens is real income. Purchasing-power parity. Inflation trajectory. Growth. Not the raw rate against one foreign currency.

Conclusion: where the weakest currencies stand in 2026

Reading this list together, the 2026 weakest-currencies table is dominated by the same forces that produced the Weimar collapse a century ago. Sanctions hit Iran. A banking implosion hit Lebanon. Climate hit Madagascar. Resource-curse dynamics hit Guinea. The names on the list change. The mechanics do not. Anyone trying to find the next weak currency a year from now should be watching the same handful of pressures wherever they cluster next. The Kuwaiti dinar remains the strongest currency in the world at 0.31 per dollar — roughly four million times the value of the rial — a reminder that the same global market produces both extremes.