Poland Crypto Tax Guide 2026: PIT-38 Filing and Taxation Rules

Sell your crypto in Poland and 19% goes to the government. Flat. No brackets. You sell Bitcoin for zlotys, you owe 19% on the profit. Been that way since 2019.

But here is the thing most people missed. On December 19, 2025, the Sejm passed the Crypto-Assets Act 2.0. Poland now has DAC8 in its law books. What does that mean for you? Every crypto exchange will report your trades directly to KAS (Krajowa Administracja Skarbowa), the Polish tax authority. By mid-2027, KAS gets the data. Your buys. Your sells. Timestamps. Amounts. Everything. And the compliance gap is absurd: roughly 3 million Poles trade crypto, but only about 1% have been paying taxes on gains, CryptoRank reported in 2026.

About 7 million Poles hold cryptocurrency now, 19% of the adult population per Disruption Banking and Statista. More Poles invest in crypto (30.9%) than in stocks (21.4%) or bonds (19%), a Kraken survey found. All of them face PIT-38, the form due April 30 every year. Some owe tax. Some carry forward losses. Most are confused, because Polish crypto tax law is a weird mix. Crypto-to-crypto swaps? Free. Mining rewards? Not taxed until you sell. But the cost deduction rules are tight and the penalties for screwing up are severe.

So here is the full picture. How crypto tax in Poland works, what triggers the 19%, what does not, how to fill out PIT-38, what costs you can deduct, and what changed in 2025 and 2026.

How cryptocurrency is taxed in Poland

Polish law classifies cryptocurrency as a "virtual currency" under the Act on Counteracting Money Laundering and Terrorist Financing. For tax purposes, crypto falls under "income from the disposal of virtual currencies" in the Personal Income Tax (PIT) Act, specifically Article 30b. This is not capital gains in the traditional sense. Poland carved out a separate category for crypto back in 2019, giving it its own rules, its own form section, and its own flat rate.

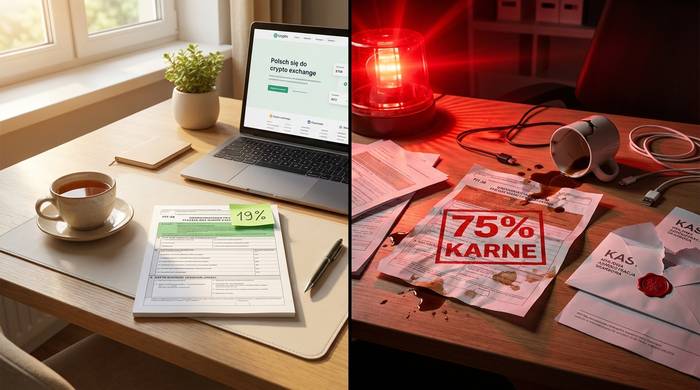

The rate is 19%. Always. Crypto is taxed at a flat 19% regardless of the amount. It does not matter if you made PLN 1,000 or PLN 1,000,000. There is no tax-free allowance in Poland for crypto. Even PLN 1 of profit triggers the obligation to file PIT-38 and pay tax on it. Income from crypto sales is subject to PIT (personal income tax) and must be reported in the annual PIT-38 return. Compare that to Germany, where gains under EUR 1,000 per year are exempt, or France with its EUR 305 threshold. Poland offers no such relief.

The tax applies to the difference between your revenue from selling virtual currencies and your tax-deductible costs. Revenue means what you received in fiat currencies or the value of goods and services you purchased with crypto. Costs means what you spent to acquire the crypto you sold, plus directly related expenses like exchange fees.

Here is the basic formula:

Taxable income = Revenue from crypto sales in a given year - Acquisition costs incurred (current year + carried forward from previous years)

If your costs exceed your income in a given year, the excess costs are carried forward to future years. You do not get a refund. The loss just rolls forward until you generate enough crypto sales revenue to absorb it. There is no time limit on this carryforward for cryptocurrency tax in Poland.

| What counts as revenue | What counts as deductible cost |

|---|---|

| Selling crypto for PLN, EUR, USD | Purchase price of the crypto sold |

| Selling crypto for goods or services | Exchange fees on purchases and sales |

| Settling debts with crypto | Transaction fees directly related to crypto |

| Exchanging crypto for property rights | Costs carried forward from prior years |

One thing Poland does not tax: exchanging one virtual currency for another virtual currency for consideration in the crypto ecosystem. Swap BTC for ETH, rotate into stablecoins, trade tokens on a DEX. None of it creates a taxable event. You do not need to report their crypto-to-crypto trades or pay any tax on them. The Polish tax code only cares when crypto becomes fiat money or buys something in the real world. The difference between the revenue from a fiat sale and your acquisition costs is what gets reported in the PIT-38.

Which crypto transactions are taxable in Poland

People get confused about which crypto moves create a tax bill and which ones are free. Polish tax law draws a clear line, and it is worth knowing exactly where that line sits.

Taxable events in Poland:

- Selling crypto for fiat currency (PLN, EUR, USD, any government money)

- Using crypto to buy goods, services, or property rights

- Settling liabilities or paying debts with crypto

- Buying NFTs with crypto (treated as a purchase of goods)

Non-taxable events:

- Buying crypto with fiat currency

- Exchanging one virtual currency for another (crypto-to-crypto swaps)

- Transferring crypto between your own wallets

- Receiving crypto from mining (taxed only when later sold for fiat)

- Receiving crypto from staking (taxed only when later sold for fiat)

- Receiving airdrops or fork tokens (zero cost basis, taxed on sale)

- Holding crypto without doing anything

- Donating crypto

The crypto-to-crypto exemption is the biggest advantage of the Polish system. Active traders who move between tokens constantly can do so without triggering any tax. The clock only starts when fiat enters the picture. This is identical to how France handles it and very different from the US or UK, where every crypto-to-crypto trade is a taxable disposal.

Mining and staking deserve extra attention. When you receive crypto from mining or staking, that event does not generate any income earned for tax purposes. KAS does not tax you on the receipt. However, the crypto you received has a cost basis of zero, which is a new acquisition with no deductible cost. When you eventually sell those mined or staked coins for fiat, the entire sale price is your taxable income because you had no acquisition cost. You cannot deduct mining equipment or electricity as costs related to financing crypto purchases, because KAS explicitly excludes these from deductible expenses. Cryptocurrency in Poland follows strict rules about what qualifies as income from property rights versus direct disposal income.

PIT-38 tax return: the crypto section explained

PIT-38 is how Poland collects capital gains tax. Since 2019, it has a dedicated Section E just for virtual currencies. You file it between February 15 and April 30 of the following year. Even if no sale was made, knowing this form exists matters for anyone holding crypto.

Open your browser. Go to podatki.gov.pl. Log into Twoj e-PIT (or use the older e-Deklaracje system, both work). Find PIT-38. If crypto was your only capital gains activity, this is the only form you need to report. Stock market gains go in a different section of the same PIT-38 form.

Scroll to Section E. Five numbers. That is all KAS wants from you:

1. How much fiat you received from selling crypto all year

2. How much you spent buying and selling that crypto this year

3. Losses carried forward from your previous PIT-38 filing

4. The result: revenue minus all costs (income or loss)

5. If positive: multiply by 19% and that is your tax bill

| PIT-38 Section E field | What to enter |

|---|---|

| Revenue from sale of virtual currencies | Total PLN received from all crypto sales |

| Costs in current tax year | Purchase price + fees for crypto sold this year |

| Costs from prior years | Losses carried forward from previous PIT-38 |

| Income (or loss) | Revenue minus all costs |

| Tax (19%) | 19% of income, if income is positive |

Costs bigger than revenue? You report a loss. That loss carries forward to the next tax year. No expiration. You plug it into the "costs from prior years" line on your next PIT-38 and it sits there until you sell enough crypto to eat it up. Pretty generous, actually. Germany limits general loss carryforward to five years. Poland does not cap it for crypto.

Miss April 30? Bad idea. KAS imposes penalties. Underreport income? Worse penalties. Do not file at all when you had taxable crypto transactions? That is criminal fiscal liability territory under the Penal Fiscal Code (Kodeks Karny Skarbowy).

Key filing deadlines for the 2025 tax year (filed in 2026):

| Milestone | Date |

|---|---|

| Tax year ends | December 31, 2025 |

| Filing period opens | February 15, 2026 |

| Filing deadline | April 30, 2026 |

| Tax payment deadline | April 30, 2026 |

How to calculate deductible costs and pay tax

The math is simple. Tracking the numbers is not. Poland uses an aggregate method. No FIFO. No LIFO. No matching specific purchases to specific sales. You just add up everything you sold for fiat during the year and subtract everything you spent to buy and sell that crypto.

Here is how it works in practice:

1. Add up every crypto-to-fiat sale during the year. This is your total revenue. Include the PLN value of any goods or services you bought with crypto.

2. Add up every acquisition cost for the crypto you sold. This is the core of tracking your crypto costs and sales. This means what you paid in fiat to buy that crypto, plus exchange fees on both the purchase and the sale. Only costs directly related to acquiring and selling crypto count.

3. Add any costs carried forward from previous years. These are losses from prior PIT-38 filings that you could not deduct because your revenue was too low.

4. Subtract total costs from total revenue. If positive, you owe 19% tax on that amount. If negative, you carry the excess forward.

Here is an example. In 2025, you sold crypto for PLN 50,000 total. Your acquisition costs for the crypto sold were PLN 35,000, plus PLN 1,500 in exchange fees. You also had PLN 5,000 in costs carried forward from 2024.

Revenue: PLN 50,000

Costs: PLN 35,000 + PLN 1,500 + PLN 5,000 = PLN 41,500

Taxable income: PLN 50,000 - PLN 41,500 = PLN 8,500

Tax owed: PLN 8,500 x 19% = PLN 1,615

You report PLN 8,500 as income in Section E of PIT-38 and pay PLN 1,615 by April 30, 2026.

What you cannot deduct matters just as much as what you can. Polish tax law explicitly excludes these expenses:

- Mining equipment and electricity costs

- Costs related to financing crypto purchases (loan interest, credit card fees)

- Crypto-to-crypto exchange costs (since swaps are not taxable, the associated costs are not deductible either)

- Advisory or consulting fees

- Hardware wallet costs

- Internet costs

This is one of the strictest deduction regimes in Europe. Germany lets you deduct virtually all expenses directly connected to crypto income. Poland says no. Only the purchase price of the crypto itself and direct transaction fees qualify.

What changed for cryptocurrencies in Poland in 2025-2026

The 19% rate has not changed since 2019. What changed is everything around it.

December 19, 2025. The Sejm passes the Crypto-Assets Act 2.0. This is Poland's DAC8 transposition, arriving right at the EU deadline (December 31, 2025) after the European Commission had already sent a formal notice about the delay. Late, but done.

What does DAC8 actually do? It turns every crypto exchange into a tax informant. Binance, Kraken, Zonda, and every other platform operating in Poland will now collect your name, address, tax identification number, date of birth, and a record of every transaction you make: buys, sells, swaps, transfers. All of it goes to KAS automatically. Retail payments over USD 50,000 get flagged separately. Transfers to external wallets get logged too.

The exchange of information timeline:

| Milestone | Date |

|---|---|

| DAC8 directive adopted by EU | October 2023 |

| MiCA fully applicable across EU | December 30, 2024 |

| Sejm passes Crypto-Assets Act 2.0 | December 19, 2025 |

| Crypto operator registration deadline | March 31, 2026 |

| Existing user self-certification deadline | October 31, 2026 |

| Account suspension for non-compliant users | December 31, 2026 |

| First data transmission to KAS | Mid-2027 |

| Automatic cross-border exchange | September 30, 2027 |

Then there is MiCA. Poland is killing the old VASP register (managed by KAS) and replacing it with proper CASP licensing under KNF, the Polish Financial Supervision Authority. If you run a crypto exchange in Poland, your old VASP registration dies on June 30, 2026. After that, you need a real CASP license from KNF. Capital requirements: EUR 50,000 to EUR 150,000, depending on what you do. Annual supervisory fee: 0.4% of revenue. Several Polish crypto operators have publicly complained about the cost.

One more number worth knowing. KAS fiscal controls jumped from 12.5% of all controls in 2019 to over 38% in 2024, according to GetSix. The tax authority is getting more aggressive every year, even before DAC8 data starts flowing.

The 19% rate itself? Staying put. No proposal to change it, no holding period exemption like Germany, no tax-free threshold in the pipeline. What you see is what you get.

Penalties, tax obligations and crypto tax reporting risks

KAS is not guessing about crypto anymore. They have been building enforcement capacity since 2020, and DAC8 hands them the raw data starting mid-2027.

Skip your PIT-38? The Penal Fiscal Code (Kodeks Karny Skarbowy) kicks in. How hard it kicks depends on how much you owe and whether KAS thinks you did it on purpose.

Small fish (unpaid tax under PLN 18,000): fines from PLN 430 to PLN 86,000. Big fish (above PLN 18,000): fines from PLN 1,300 to over PLN 30 million. Deliberate evasion? Two years in prison is on the table.

And then there is the punitive rate. KAS can hit undeclared crypto income with a 75% tax rate, according to CryptoRank. Not 19%. Seventy-five percent. That is what happens when they find income you hid. For people running unlicensed crypto businesses, the penalties go further: up to PLN 10 million (about USD 2.5 million) and prison time.

There is a way out if you messed up. File a voluntary correction (korekta) before KAS contacts you. This is huge. A correction filed on your own initiative largely eliminates criminal fiscal liability. KAS treats self-reporters completely differently from people they have to chase down.

One more pain point: late payment interest runs at roughly 14.5% annually as of early 2026, tied to the NBP reference rate. That is among the highest in the EU. Procrastinating costs real money on top of the penalties.

What to do to stay on the right side:

1. Track every crypto-to-fiat sale throughout the year. The date, the amount in crypto, the PLN value received, and the exchange used.

2. Track every purchase and its cost in PLN, including exchange fees.

3. Keep exchange records and screenshots. KAS can request documentation going back six years.

4. Use a crypto tax calculator like Koinly, CoinLedger, or Divly to generate your PIT-38 numbers. Manual tracking with hundreds of trades is error-prone.

5. File by April 30 every year, even if no sale was made. If you only bought crypto, you report zero revenue but still note your costs so they carry forward correctly.

6. If you made a mistake, file a correction immediately. A voluntary correction filed before KAS initiates proceedings largely eliminates criminal fiscal liability.

Getting tax advice from a tax professional familiar with Polish crypto taxation makes sense if you have complex situations: mining income, crypto received as salary, DeFi positions, or crypto inherited from a deceased relative. The rules for these edge cases have limited guidance from KAS. You can also visit your local tax office for basic tax information about PIT-38, though crypto-specific expertise varies. Consult the Polish Financial Supervision Authority (KNF) website for regulatory updates on exchange licensing and the disposal of virtual currencies.