What Is Venmo and How Does It Work? Fees and Crypto

Venmo turned a chore into a reflex. Split a dinner bill, pay back a friend, chip in for a group gift, and a few taps later it is done. "Just Venmo me" is a complete sentence now, and everyone knows what it means. But the app people reach for without thinking is more specific than it looks. It is owned by PayPal, it works only inside the United States, and it is engineered to do one thing brilliantly while quietly capping the rest. Knowing where those caps sit is the difference between using Venmo well and getting caught out by it. Here is what Venmo actually is, what it costs, how its crypto and business sides hold up, and where it simply stops.

What is Venmo and who owns it?

Venmo is a mobile app for sending and receiving money between people, usually small everyday amounts. It launched in 2009, was folded into Braintree, and became part of PayPal when PayPal bought Braintree in December 2013 for around 800 million dollars. That ownership matters, because it means Venmo runs on the same payments infrastructure and rules as its parent. The app started as a way for its two founders to pay each other back by text message — a small idea that scaled into a verb. People now say "Venmo me" the way they once said "Google it," which is a fair measure of how completely one app can swallow a habit.

The scale is large. PayPal reported about 67 million monthly active Venmo accounts at the end of 2025, with more than 100 million accounts active over the trailing year, and roughly 1.7 billion dollars in Venmo revenue for the year. For all that reach, Venmo works in one country. You need a US bank account, a US phone number, and US residency to use it, which is the first limit worth remembering.

One quirk defines the experience: by default, Venmo publishes your payments to a social feed. It hides the dollar amount but shows who paid whom and the caption. It is a payment app with a social network bolted on, and that design choice shapes both its charm and its risks.

How does Venmo work, step by step?

The mechanics are simple. The defaults are where people get caught.

Linking a bank account or card

To start, you connect a funding source: a US bank account, a debit card, or a credit card. Venmo verifies your identity for larger limits, asking for the last four digits of your Social Security number and similar details. Money you receive lands in your Venmo balance, which you can spend directly, move to your bank, or use with the Venmo debit or credit card.

Sending and receiving money

Sending is a matter of picking a person, typing an amount, adding a note, and hitting pay. The recipient gets the money in their Venmo balance almost instantly. Getting it into an actual bank account is where timing splits in two. A standard transfer is free but takes one to three business days. An instant transfer is near-immediate but carries a fee, which we will break down in a moment.

The social feed and privacy

Here is the part that surprises people. Unless you change the setting, your transactions post publicly. Anyone can see that you paid your roommate, with whatever caption you wrote. You can switch your default to private in the settings, and it is worth doing on day one. Just as important: a normal personal payment carries no buyer protection. If you send money to a stranger for a concert ticket and they vanish, Venmo will not refund you. That safety net exists only for the right kind of transaction, which the safety section explains.

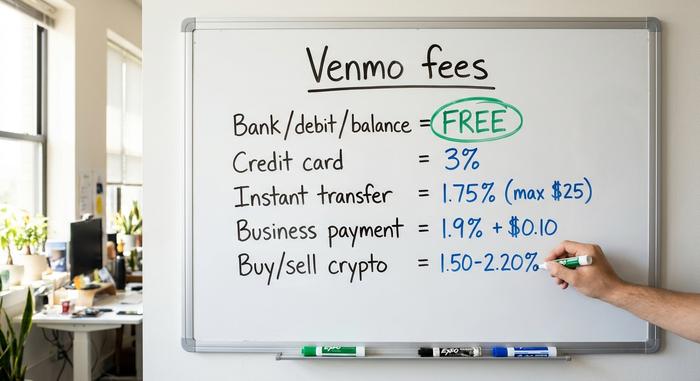

Venmo fees and limits explained

Venmo calls itself free, and for the everyday case it genuinely is. The catch hides in how you move the money. Pay the wrong way or cash out in a hurry, and Venmo quietly takes a slice.

| Action | Fee |

|---|---|

| Send from bank, debit, or Venmo balance | Free |

| Send with a linked credit card | 3% |

| Standard transfer to your bank (1-3 days) | Free |

| Instant transfer to your bank or card | 1.75% (min $0.25, max $25) |

| Receiving a business or goods-and-services payment | 1.9% + $0.10 |

| Buying or selling crypto | 1.50% to 2.20% |

Limits matter as much as fees, and they hinge on one thing: whether you have verified your identity. Skip verification and Venmo caps your weekly sending at $299.99 — fine for dinners, useless for rent. Verify, and the ceiling jumps to as much as $60,000 a week for combined activity, while bank cash-outs top out near $19,999.99 weekly. These numbers come from Venmo's own fee and help pages as of mid-2026, and they move now and then, so check the official page before any big transfer.

The practical takeaway is small but useful. Fund payments from your bank or balance, use standard transfers when you are not in a rush, and you will likely never pay Venmo a cent. Reach for a credit card or an instant cash-out and the meter starts running.

Is Venmo safe, and is your money insured?

Venmo is safe for what it is designed to do, and risky the moment you stretch it past that. The distinction is worth getting right.

Your balance is not a bank deposit, but funds can qualify for FDIC pass-through insurance when held through Venmo's partner banks, generally when you have set up direct deposit or the Venmo debit card. The bigger issue is protection on the payment itself. Venmo offers Purchase Protection only on payments tagged as goods and services, or made to a business profile. A standard personal payment to another user has no such cover, which is exactly why scammers push buyers to send money "as a friend." If you are buying something from someone you do not know, that is the wrong button.

Two more habits help. Keep your feed private so strangers cannot map your social and spending graph, and treat any "accidental" payment or urgent request with suspicion, since both are common scam setups. A typical version runs like this: a so-called buyer overpays for an item and asks you to send back the difference, except the original payment was fraudulent and later reverses, leaving you out the real money you refunded. Slow down on anything that feels rushed or too generous, and you avoid most of it. Venmo settled with the US Federal Trade Commission in 2018 over how it had described its security and handled transaction notifications, a reminder that the app is convenient first and a vault second.

Venmo crypto: buy, sell, and transfer

Venmo added crypto to reach users where they already were. It is a genuinely easy on-ramp. It is also custodial and US-only, which means it is not the same as holding your own coins.

Which coins Venmo supports

Venmo began offering crypto on April 20, 2021, starting with Bitcoin, Ethereum, Litecoin, and Bitcoin Cash. The menu has grown since. By 2026 the app supports around seven assets, adding Solana, Chainlink, and PayPal's own stablecoin, PYUSD. You can buy a few dollars' worth in the same app you use to split rent, which is the whole appeal.

Crypto fees and the custodial catch

Buying and selling crypto on Venmo carries a tiered fee, roughly 1.50% to 2.20% depending on the size of the trade, plus the spread baked into the price. More important than the fee is the structure. Venmo holds the coins for you. You do not control the private keys, you cannot use the crypto across the wider blockchain world from inside the app alone, and only US residents can access the feature. It is crypto with training wheels, fine for dipping a toe, limiting if you want true ownership. The distinction is not academic; if Venmo freezes your account or changes its crypto policy, your coins move at the company's pace rather than yours. Real ownership means the keys sit in your hands, and inside the app they never do.

PYUSD and external transfers

The interesting recent piece is PYUSD, PayPal's dollar-pegged stablecoin. It trades free of Venmo's crypto fee and has offered a yield of around 3.7% on held balances, a rare touch of interest inside a payments app. Venmo also lets you transfer crypto out to external wallets and other exchanges, a feature added after the initial launch, which softens the custodial limit a little. If self-custody is your goal, though, an actual wallet still beats an app that holds the keys for you.

Using Venmo for business payments

For sellers, Venmo is easy to switch on and worth understanding before you do. A business profile lets customers pay you with the app they already trust, and "Pay with Venmo" appears at checkout on many online stores. The cost is a seller fee of 1.9% plus $0.10 per transaction, in the same range as most card processors.

Taxes are the part that trips people up. After years of back-and-forth, the reporting threshold for a 1099-K form returned to the long-standing rule of more than $20,000 and more than 200 transactions, set by the One Big Beautiful Bill Act signed in July 2025. That reverses the much-feared $600 threshold. It does not change what you owe, only when the platform files a form, and your actual tax obligation on business income stands regardless. The other catches are structural: Venmo only reaches US customers, and like any card-based rail it exposes you to chargebacks. A customer can dispute a payment weeks after the fact — and on card-based rails the seller usually eats the loss plus a dispute fee. For a small US shop that is a manageable nuisance; for a high-volume or online seller, it adds up fast.

Venmo vs Cash App, Zelle, and PayPal

Venmo is not the only option, and the right pick depends on what you actually need. Speed, crypto, business tools, and reach pull in different directions.

| App | Owner | Crypto? | Key fee | Best for |

|---|---|---|---|---|

| Venmo | PayPal | Yes (custodial) | 1.9% + $0.10 business | Social P2P in the US |

| Cash App | Block | Bitcoin + stocks | Varies | Crypto and investing |

| Zelle | Bank consortium | No | Free | Instant bank-to-bank |

| PayPal | PayPal | Yes | 2.99% + fixed business | Online checkout, global |

Zelle is the heavyweight for plain transfers, with about 151 million enrolled users and more than a trillion dollars moved in 2024, but it sends money straight between bank accounts with no stored balance and no crypto. Cash App leans into investing. PayPal is the broadest and most international. Venmo's edge is the social, casual feel and deep US adoption, which is exactly why it became the default among friends.

Beyond Venmo: crypto payments for merchants

For a US business taking small in-person or social payments, Venmo is hard to beat. For a seller who ships worldwide or sells online, its limits start to bite: US-only customers, a 1.9% plus $0.10 fee, and exposure to chargebacks. Card fraud is not cheap. Industry research puts the cost of fraud at around $4.61 for every dollar of fraudulent activity, and global chargeback losses were projected to reach roughly $28.1 billion by 2026.

This is where crypto payment gateways enter the picture. Services such as Plisio let a merchant accept Bitcoin, stablecoins, and other coins directly, with no chargebacks because blockchain payments are final, global reach by default, and often lower fees than card rails. The trade-off is real and worth stating plainly: the merchant takes on price volatility and the finality cuts both ways, since a mistaken payment cannot be clawed back. It is not a replacement for Venmo in every shop, but for global or online sellers it solves the exact problems Venmo cannot.

What to remember before you use Venmo

Venmo earned its place as the casual money app of choice in the US, and for splitting costs with people you trust, little beats it. Just hold three things in mind. Its fees hinge on how you pay and cash out, so stick to bank funding and standard transfers to keep it free. It stops at the US border. And its crypto and business features, handy as they are, run on someone else's custody and rails. Used for what it is good at, Venmo is excellent. The only real question is whether what it is good at matches what you actually need.