Crypto Tax Loss Harvesting: The 2026 IRS Guide

Crypto investors get a tax break that stock investors can only dream about. If your shares of a company fall, you can sell them for the loss, but if you buy them back too soon, the IRS throws the loss out. Crypto does not work that way. You can sell Bitcoin at a loss, claim the deduction, and buy it back a minute later while still keeping the loss on your books.

That move is the heart of crypto tax loss harvesting, and it is one of the few genuinely investor-friendly quirks left in the tax code. The mechanics are simple. The catch is that the ground shifted in 2025 and 2026: the rules for tracking cost basis changed, brokers now report your trades to the IRS, and Congress keeps trying to close the loophole. This guide covers how harvesting works, why it is so powerful for crypto, and what the new rules mean for you.

How crypto tax loss harvesting works

There is nothing magical here. Tax loss harvesting turns a paper loss into a real deduction that shrinks your tax bill. You sell an asset that is worth less than you paid, which "realizes" the loss, and then you use that capital loss to offset capital gains elsewhere in your crypto portfolio. An unrealized loss sitting in your wallet does nothing for you. A realized one is money back at tax time.

The order matters. Short-term losses offset short-term gains first, and long-term losses offset long-term gains first, before they cross over. That detail is worth caring about, because short-term gains are taxed as ordinary income at rates up to 37%, while long-term gains top out at 20%. A short-term loss is the more valuable tool, because it kills the more expensive kind of gain.

How much you actually save depends on your tax rate. A harvested loss that cancels a short-term gain saves you at your ordinary income rate, which can reach 37%, while a loss applied to a long-term gain saves you at most 20%. That is why disciplined investors harvest losses against their short-term gains first: the same dollar of loss delivers a bigger tax benefit when it erases the more heavily taxed gain.

Offsetting capital gains and cutting your tax bill

Once your losses wipe out your gains, the benefit does not stop. If you still have losses left over, you can deduct up to $3,000 of them against ordinary income each year, according to the IRS. Anything beyond that does not vanish. It carries forward to future tax years, with no expiration date, until you have used every dollar. Someone who harvested a large loss in a brutal year can keep lowering their tax liability for years afterward.

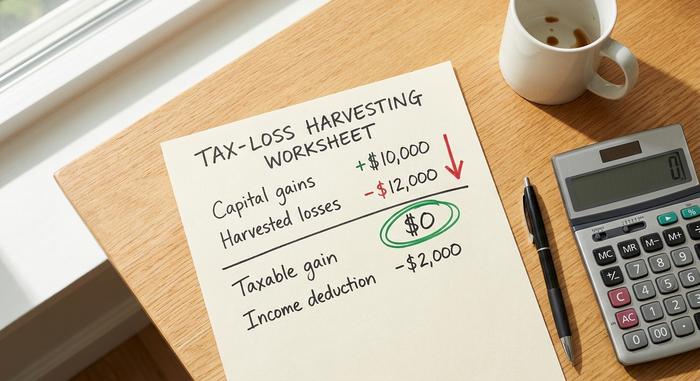

A worked example

Numbers make it concrete. Say you took $10,000 in capital gains this year, then harvested $12,000 in losses on coins that had dropped.

| Item | Amount |

|---|---|

| Realized capital gains | $10,000 |

| Harvested capital losses | -$12,000 |

| Net capital gain | $0 (fully offset) |

| Deduction vs ordinary income | -$2,000 |

| Loss carried to next tax year | $0 |

The gain is erased, and the extra $2,000 comes off your ordinary income. The loss to offset future income is gone here — but in a bigger loss year, the carryforward does the heavy lifting.

The wash sale rule and the crypto loophole

This is where crypto pulls ahead of stocks — and where tax-loss harvesting delivers its sharpest edge. The wash sale rule, found in Section 1091 of the tax code, blocks you from claiming a loss if you buy back the "substantially identical" asset within 30 days. It exists to stop investors from selling purely for the tax break and instantly rebuying. For stocks, it bites hard.

For crypto, it does not bite at all.

Why the wash sale rule doesn't apply to crypto

Section 1091 applies only to "stock or securities." The IRS, in Notice 2014-21, classified virtual currency as property, not a security. The rule applies to traders in shares and bonds; it does not reach property, and crypto is property. Because of that classification, the wash sale rule does not apply to it under current law. That single classification is the whole edge. You can sell a coin to harvest the loss and rebuy the same coin immediately, holding your position the entire time while still booking the loss for tax purposes. A stock investor has to sit out 30 days and risk the rebound. A crypto investor does not.

The bills trying to close the loophole

Do not assume this lasts forever. The wash sale exemption for crypto has a target on its back. The Treasury's FY2025 Greenbook, released in March 2024, proposed extending Section 1091 to digital assets, a change scored at more than $42 billion over ten years. It was not enacted. In July 2025, Senator Cynthia Lummis introduced digital-asset tax legislation that would apply a 30-day wash sale rule to crypto, paired with a small de minimis exemption. A revised version, the PARITY Act, was reintroduced in 2026. As of mid-2026, none of these have passed. I would not bet on that holding forever. The window is open, but it is politically fragile, and that is reason to use it deliberately rather than assume it will be there next year.

Cost basis methods and the 2025 IRS rule

Here is the change almost every older guide still ignores. How you calculate cost basis decides how big your harvested loss is, and the rules tightened in 2025. Under Revenue Procedure 2024-28, you can no longer pool your basis across every wallet and exchange. From January 1, 2025, basis must be tracked wallet by wallet, account by account.

The method still matters. FIFO, or first in first out, is the IRS default and sells your oldest coins first. HIFO, highest in first out, sells your most expensive lots first, which produces the biggest loss to harvest. Specific Identification lets you hand-pick the exact tax lots you sell.

| Method | What it sells first | Effect on harvesting |

|---|---|---|

| FIFO (default) | Oldest coins | Often smaller losses |

| HIFO | Highest-cost coins | Largest harvestable loss |

| Specific ID | Lots you choose | Most control, most record-keeping |

HIFO is still allowed, but now it operates inside each account rather than across your whole portfolio. Whichever method you choose, you have to apply it consistently and keep the cost bases for every lot on record. Good crypto tax software handles this allocation automatically, and a crypto tax calculator that supports per-wallet accounting is close to essential now, because a number that used to be a single pooled figure is spread across every account you hold. Doing it by hand across several wallets is where people make mistakes.

1099-DA reporting and your crypto losses

Harvesting used to happen in the dark. That era is over. Starting with 2025 transactions, custodial brokers report your crypto sales to the IRS on the new Form 1099-DA, which covers gross proceeds first, with cost-basis reporting phasing in for 2026 transactions. When you file your tax return, your reported crypto losses now have to line up with what the broker already sent the IRS.

This does not make harvesting harder; it makes sloppy records dangerous. If your Form 8949 says one thing and your 1099-DA says another, you invite a notice. The practical takeaway is simple: keep clean transaction histories, reconcile them against the forms your exchange issues, and treat the numbers as something the IRS can already see, because now it can. Crypto tax-loss harvesting is still completely legal; it simply happens in plain view, so the records behind every claimed loss have to hold up to a cross-check.

Timing: when to harvest crypto losses

The calendar runs the show. A loss only counts if you realize it by December 31 of the tax year you want it in. Miss the date and the chance is gone until next year.

But waiting for late December is the rookie move. Crypto is volatile, and the best harvesting opportunities show up on sharp mid-year dips, not in a year-end scramble when half the market is doing the same thing. Investors who watch their crypto portfolio through the year can harvest a deep loss in a spring crash, rebuy, and still hold the position when the recovery comes. Treat harvesting as an ongoing tax strategy, not a single December chore.

Risks and limits of tax-loss harvesting

It is not free money, and pretending otherwise gets people burned. Every sell-and-rebuy carries transaction or gas fees, which eat into the benefit on small positions. More important, rebuying resets your cost basis to the new, lower price. That feels fine today, but it means a larger taxable gain later when the asset climbs, so you are partly deferring tax, not erasing it.

There is also market risk if you choose to wait before rebuying. Illiquid altcoins and thinly traded NFTs can be hard to harvest cleanly, because you may not get a fair price on the way out. And while the wash sale rule does not apply, harvesting purely for tax with no real economic change can still draw scrutiny under the broader economic-substance doctrine. Harvest because it fits your portfolio, not as a reflex.

How to report your crypto capital losses

The paperwork is straightforward but unforgiving. Every harvested sale goes on Form 8949, then flows to Schedule D of your tax return, where your crypto capital losses net against your gains and feed the final numbers on your tax report. Each transaction needs a date, a cost basis, proceeds, and the resulting gain or loss.

This is where crypto tax software or a crypto tax calculator earns its fee, pulling your trades and computing basis across wallets under the 2025 rules. Still, you own the numbers. Reconcile the software's output against your 1099-DA before you file, because the IRS will.

Crypto tax-loss harvesting in the UK

A quick look abroad shows how good US investors have it. The United Kingdom already shut this door. HMRC's "bed and breakfasting" rule disallows the loss if you sell a token and rebuy the same one within 30 days, the same idea the US applies to stocks but not crypto. British investors also work with a 2025/26 capital gains tax annual exempt amount of just £3,000, with CGT charged at 18% or 24%. Same strategy, far less room.

| Feature | United States | United Kingdom |

|---|---|---|

| Wash sale on crypto | Does not apply | 30-day rule applies |

| Rebuy same asset | Immediately, keep the loss | Wait 30 days or lose it |

| Annual income offset | $3,000 | £3,000 exempt amount |

| Capital gains rate | 0-20% long-term | 18% or 24% |

For Americans, the open wash sale gap is a real, and possibly temporary, advantage.

The bottom line on crypto tax loss harvesting

The loophole that makes crypto tax loss harvesting so powerful is real and unusually generous, but it is shrinking from two directions at once. The rules around cost basis and reporting tightened in 2025, and Congress keeps drafting bills to kill the wash sale exemption outright. None of that changes the core move: sell into losses, offset your gains, deduct $3,000 against income, and carry the rest forward. What changed is the discipline required around it. Track basis wallet by wallet, keep records that match your 1099-DA, and harvest on real dips rather than year-end panic. The bigger question is how long the US keeps handing crypto investors an edge that stock investors never get. Would you bet on it lasting?