Wrong UPI Transaction Complaint: How to Get Money Back

So you've just realized the payment went to the wrong person. Take a breath. UPI processed over 100 billion transactions in India in 2023, and mistakes happen constantly — a single mistyped character in a UPI ID is enough. The wrong UPI transaction complaint process isn't complicated, but most people don't know where to start, or worse, they wait too long.

This guide lays out the steps plainly: what to do in the first hour, how to file a complaint through your app or the NPCI portal, where to escalate when the bank stops responding, and the NPCI complaint number you'll want saved on your phone. The escalation roadmap here goes further than most guides do — all the way to the RBI Banking Ombudsman if it comes to that.

What Counts as a Wrong UPI Transaction?

UPI, short for Unified Payments Interface, is operated by NPCI (National Payments Corporation of India) and built for speed. The moment you enter your PIN, the money is gone. That's what makes a mistake so stressful: there's no pending window, no cancel button, no grace period.

Wrong UPI transactions usually fall into one of these categories:

- Sent to the wrong UPI ID — a typo in the recipient's VPA (Virtual Payment Address) sends money to a complete stranger

- Sent the wrong amount — ₹10,000 instead of ₹1,000, or an accidental tap on "send"

- Duplicate payment — the same bill or person paid twice

- Transaction failed but money was debited — your account shows a debit but the recipient got nothing; these typically auto-reverse within 3–5 business days, though some need a manual push

Each type has a slightly different resolution path. The first-hour actions, though, are identical across all of them.

First Steps After a Wrong UPI Transfer

The window right after a wrong UPI transfer is your best shot at recovery. If the recipient hasn't touched the funds yet, resolution is significantly more likely.

- Screenshot the transaction receipt right away. Open the UPI app, find the payment, and capture the full details screen. This screenshot is your primary evidence for every step that follows.

- Write down the key details: UTR (Unique Transaction Reference) number, exact amount, date and time, your UPI ID, and the receiver's UPI ID or mobile number.

- Try reaching the recipient directly if you know who they are. A straightforward message explaining the mistake gets money back more often than people expect.

- Don't share your UPI PIN or OTP with anyone. When word gets out that someone sent money by mistake, scammers appear fast, posing as bank agents who can "reverse" the transfer. No real bank or NPCI representative asks for your PIN. Ever.

- Call 1930 immediately if fraud is involved. That's the national cyber crime helpline. Early reports give authorities a chance to freeze the fraudster's account before the money moves.

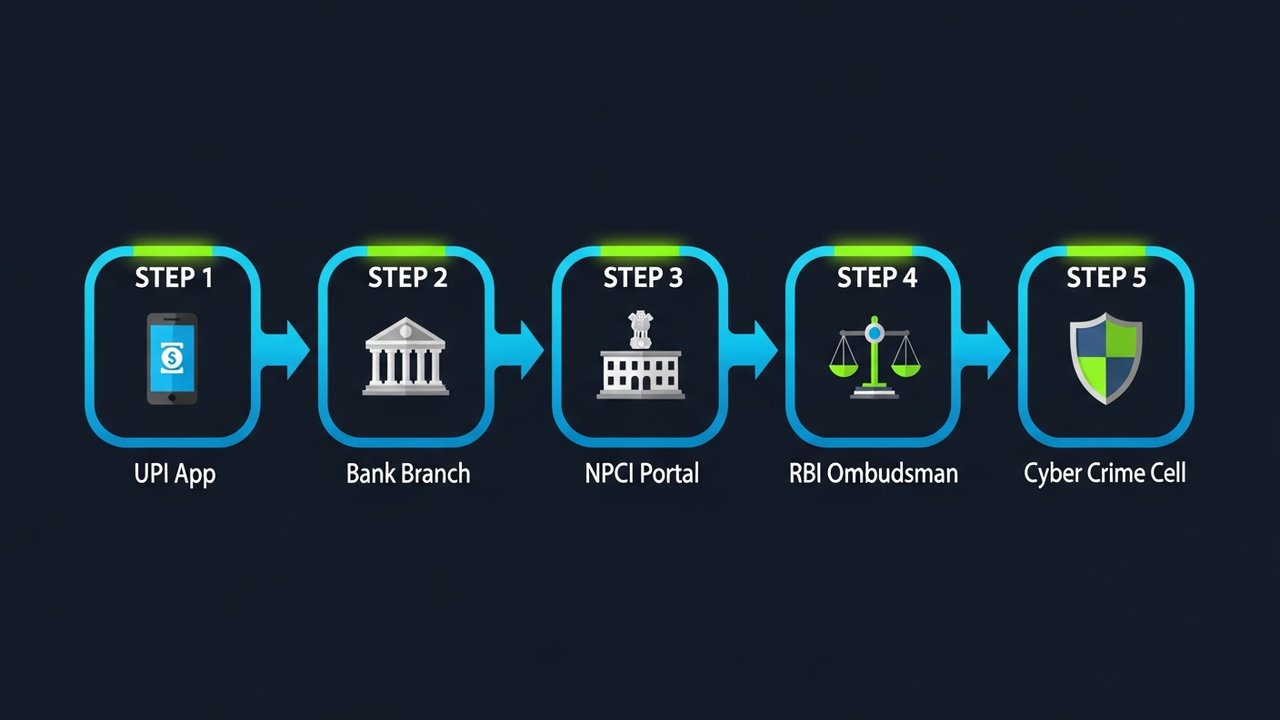

How to Raise a Wrong UPI Transaction Complaint

Once you have your evidence together, it's time to raise a formal wrong UPI transaction complaint. Three channels are available: your UPI app, the NPCI dispute portal, or your bank branch. Start with the app — it's the fastest and leaves a digital trail automatically.

Through Your UPI App (Google Pay / PhonePe / Paytm / BHIM UPI)

Every major UPI app has a dispute or help section built in. Labels differ by app, but the path is roughly the same across all of them.

Google Pay:

1. Open the app and tap your profile icon → Help & feedback

2. Under "Payments & transactions," select the transaction in question

3. Tap Report a problem → choose the relevant reason (e.g., "Sent to wrong person")

4. Submit your complaint and note the ticket/reference number

PhonePe:

1. Go to Transaction History → tap the specific payment

2. Scroll down and tap Need help? → Report an issue

3. Select the issue type and submit

Paytm:

1. Open Passbook → tap the transaction

2. Tap Raise a dispute and follow the on-screen form

BHIM UPI:

1. Go to Transaction History → select the payment

2. Tap Raise Complaint → fill in the details and submit

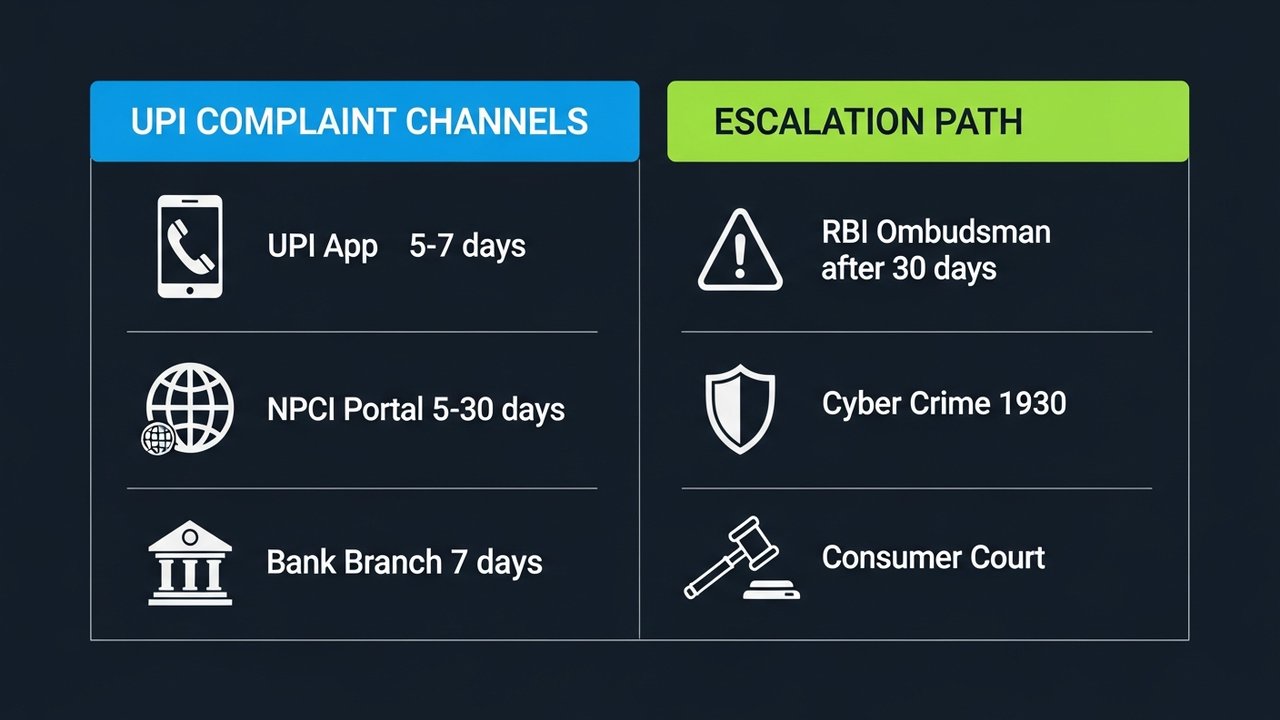

You'll get a complaint reference number after submitting. Save it somewhere. The app usually acknowledges within 24 hours and targets resolution within 5–7 business days.

Through the NPCI Dispute Redressal Portal

If the UPI app complaint stalls, go directly to the NPCI dispute redressal mechanism at npci.org.in/dispute. This is the official portal of the National Payments Corporation of India.

- Go to npci.org.in → What We Do → UPI → Dispute Redressal Mechanism

- Select Raise Complaint

- Choose the complaint nature: "Incorrectly initiated transaction" or "Amount deducted but not credited"

- Enter your transaction details: UTR number, bank name, amount, date, and both UPI IDs

- Attach your transaction screenshot

- Submit and record the NPCI complaint reference number

NPCI typically investigates within 5–30 business days depending on the complexity of the case.

Through Your Bank Branch

For larger amounts, or if you prefer a paper trail, visiting your bank branch is worth the trip.

- Visit the branch where your UPI-linked account is held

- Ask for the UPI/Digital Payment Dispute form — or just write a simple application

- Include: your account number, UTR number, transaction amount, date, and the receiver's UPI ID

- Submit to the branch manager and get a written acknowledgment with a complaint reference number

- Follow up in 7 business days

One thing worth knowing: recovery chances jump noticeably when the sender and receiver bank with the same institution. The bank can coordinate the return directly without looping in NPCI.

NPCI UPI Complaint Number and Contact Details

Keep these contacts somewhere accessible. Filing through more than one channel at the same time is fine — it often moves things faster.

| Channel | Contact / URL | Availability |

|---|---|---|

| NPCI Toll-Free Helpline | 1800-120-1740 | 24×7 |

| NPCI Dispute Portal | npci.org.in/dispute | Online, 24×7 |

| Your UPI App Support | In-app Help / Raise Dispute section | 24×7 (response within 24 hrs) |

| Bank Customer Care | Listed on your bank's website/passbook | Business hours (some 24×7) |

| RBI Banking Ombudsman | bankingombudsman.rbi.org.in | Online, 24×7 |

| Cyber Crime Helpline | 1930 / cybercrime.gov.in | 24×7 (for fraud cases) |

When you call the NPCI toll-free number 1800-120-1740, have your UTR number, transaction amount, and registered mobile number ready. The IVR asks for these right at the start.

How to Check Your UPI Complaint Status

You don't have to sit and wait after filing. Tracking your wrong UPI transaction complaint status is straightforward, and following up proactively often makes the difference between a case that moves and one that doesn't. Knowing where to check means you can raise a complaint follow-up before any deadline lapses.

- Via your UPI app: Go to Help → My Complaints (or equivalent). Most apps show real-time updates: "Under investigation," "Resolved," or "Closed."

- Via NPCI portal: Visit npci.org.in/complaint-status, enter your complaint reference number and registered mobile number.

- Via bank: Call your bank's customer care with your complaint number and ask for the current status and expected resolution date.

- Via email: Some banks handle dispute tracking through email — check your bank's support page for a dedicated dispute inbox.

If nothing has changed after 5 business days, call the NPCI toll-free number and quote your UTR and complaint reference together. Banks and UPI apps are required under RBI guidelines to acknowledge disputes within 3 business days and resolve them within a set window — following up when they miss that is your right, not an imposition.

What If the UPI Dispute Is Not Resolved?

Most wrong UPI complaints get sorted at the app or bank level. But when they don't, there's a full escalation path with legal weight behind each step.

- Day 1–5: Follow up with your UPI app. No update after 5 business days? Ask for escalation to a senior support tier or call the app's helpline directly.

- Day 5–15: Take it to your bank. Visit the branch or call customer care. Ask to escalate to the bank's grievance officer — every scheduled commercial bank in India must have one, per RBI rules.

- Day 15–30: File with NPCI independently. If the bank hasn't closed the dispute redressal mechanism request within 15 days, submit your own complaint through the NPCI portal.

- After 30 days: RBI Banking Ombudsman. Thirty days without satisfactory resolution from your bank? File at bankingombudsman.rbi.org.in. No lawyer needed, no fee. Banks are legally obligated to respond.

- Fraud scenarios: Cyber Crime Cell. If someone tricked you into sending the money, file an FIR at cybercrime.gov.in or your nearest cyber crime police station. The sooner you do it, the better the odds of freezing the account before the money disappears.

- Consumer court. Bank or app negligence that caused you financial harm can be taken to consumer court under the Consumer Protection Act. You'll need documentation from every previous step, so keep everything.

Document everything from day one. Screenshots of app complaints, written bank acknowledgments, email confirmations — all of it. A formal written request to the bank's grievance officer shifts the complaint's legal status and puts the bank on the clock: 30 days to respond, no exceptions.

Tips to Prevent Wrong UPI Transactions

Most wrong UPI transaction errors are preventable. A few small habits remove most of the risk:

- Check the name before confirming. UPI apps display the account holder's name when you enter an ID. Glance at it before you enter your PIN. Takes two seconds, saves hours of grief.

- Read the amount twice. For anything above a few hundred rupees, type it, pause, and read it again before proceeding.

- Save frequent payees. Pre-verified UPI IDs stored as favorites eliminate mistyping entirely for repeat payments.

- Send ₹1 first with new recipients. A test payment to a vendor or freelancer you've never paid before confirms the ID is right before the real amount follows.

- Enable transaction notifications. Instant SMS or push alerts let you catch a mistake within seconds, while there's still time to act.

- Don't pay in a hurry. The majority of UPI errors happen when people are distracted or rushing. Treat every payment as something that takes five focused seconds.

- Set a transaction limit. Your bank lets you configure per-transaction and daily UPI limits. A sensible cap reduces the damage any single mistake can do.

A Note for Merchants: Consider Crypto Payments

If your business accepts UPI regularly, wrong-transfer disputes are an occupational hazard. Blockchain payments work on a different logic: a transaction gets validated against a wallet address before it broadcasts. There's no "wrong ID sent by mistake" scenario in the same way mistyped VPAs create one.

Understanding how a cryptocurrency payment gateway handles payments makes clear why dispute rates are structurally lower. As digital payments drive business growth across India, a growing number of merchants treat crypto as a low-fee complement to UPI rather than a replacement. If you're running significant volume, reviewing the best crypto payment gateways is worth your time.

Plisio accepts crypto payments with low fees, multi-coin support, and a clean API. Visit Plisio to see how it fits a merchant setup.

Filing a wrong UPI transaction complaint is manageable when you work through the right channels in the right order. The steps above cover everything from the first hour through the RBI Ombudsman, if it ever comes to that.