UK Crypto Tax: HMRC Rules, Rates and How to Pay

HMRC already knows more about your crypto than you probably think. In the 2024/25 tax year it sent roughly 65,000 "nudge" letters to suspected crypto holders, more than double the year before. Around 8% of UK adults now own some crypto, about 4.5 million people, according to the FCA's 2025 consumer research. So UK crypto tax is no longer a niche worry for a few traders. It is a mainstream tax return obligation, and the rules are about to get a lot harder to ignore.

Here is the thing most people get wrong from the start. There is no separate "crypto tax" in Britain. Your coins are taxed under the same two systems that govern shares and rental income: Capital Gains Tax and Income Tax. What is changing in 2026 is not the rates. It is how much HMRC can see.

Does HMRC tax crypto in the UK?

Yes, and the way it does it surprises people. HMRC does not treat crypto as money. It treats cryptocurrency in the UK as property — an asset you hold and dispose of, set out in its Cryptoassets Manual. That single decision shapes everything else.

Because crypto is an asset, selling it or swapping it can trigger Capital Gains Tax on the profit. And because some crypto arrives as a reward for doing something, like staking or mining, that crypto can be taxed as income the moment you receive it. Most holders only ever meet the first system. People who earn rewards meet both.

There is no special crypto rate, no crypto allowance, and no separate crypto return. You report it inside the ordinary Self Assessment system. The hard part is not the tax in the UK itself. It is knowing which of the two systems applies to each thing you did, because the answer changes the bill.

Capital gains tax on crypto gains

For most crypto investors, Capital Gains Tax is the whole story. You bought a coin, it went up, you sold. The profit is a gain, and above a certain point the gain is taxable. Simple enough until you realise how often you "dispose" of crypto without ever touching your bank account.

CGT rates and the £3,000 allowance

Since 30 October 2024, crypto gains are taxed at 18% if you are a basic-rate taxpayer and 24% if you are a higher or additional-rate taxpayer, per the GOV.UK Capital Gains Tax rates. That makes 2025/26 the first clean full year at these numbers, with no mid-year split to untangle.

Before any tax applies, you get a tax-free allowance. For 2025/26 and 2026/27 the annual exempt amount is £3,000. Worth remembering how fast that has shrunk: it was £12,300 back in 2022/23. A lot more ordinary investors fall into the net now than did three years ago.

What counts as a disposal

This is where people trip. A disposal is not just cashing out to pounds. You make a disposal when you sell crypto for GBP, swap one crypto for another, spend crypto on goods or services, or give it away to anyone other than your spouse or civil partner. That crypto-to-crypto swap is the silent one. Trade Bitcoin for Ethereum and you have disposed of the Bitcoin, even though no money hit your account.

What is not a disposal: buying crypto with pounds, holding it, and moving it between your own wallets. Those are free.

Working out your cost basis (share pooling)

To find the gain you subtract your cost from your proceeds, and HMRC makes you calculate the cost a specific way. It is called share pooling. Three rules apply in order: the same-day rule first, then the 30-day "bed and breakfasting" rule, and finally the Section 104 pool, which averages the cost of everything else you hold of that token. If you have traded the same coin many times, doing this by hand is painful, which is exactly why most people use software. I would not try to reconstruct an active year any other way.

Income tax on crypto income and rewards

What catches earners off guard is that some crypto is taxed twice over its life. Once as income when it lands, and again as a capital gain when you later sell it.

If you receive crypto from mining, staking, or DeFi lending rewards, HMRC usually treats it as miscellaneous income. You owe Income Tax on its pound value on the day you received it, under guidance like CRYPTO61211. The same applies if an employer pays you in crypto. Income Tax in the UK runs at 20% for basic-rate earners, 40% for higher-rate, and 45% above that, after the £12,570 personal allowance, which is frozen until April 2031.

Airdrops are the exception that proves the rule. If you did nothing to earn an airdrop, it usually falls outside Income Tax and is only assessed for CGT when you dispose of it. If you had to perform a service to get it, it is income. The trigger is whether you earned it.

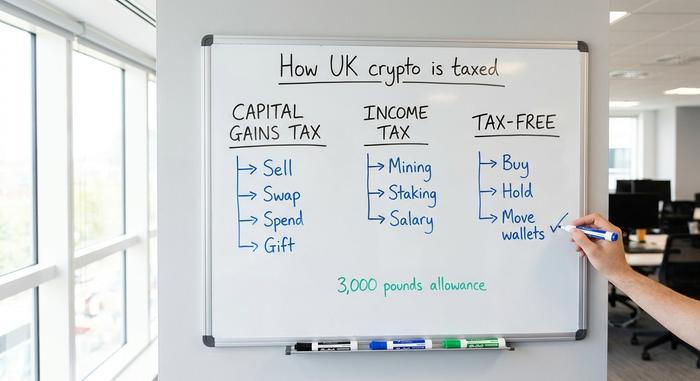

How different crypto transactions are taxed

Crypto throws up a long list of actions, and each one has its own answer. Rather than bury them in prose, here is the lookup table.

| What you did | How it is taxed |

|---|---|

| Buy crypto with GBP | Not taxed |

| Hold crypto | Not taxed |

| Move between your own wallets | Not taxed |

| Sell crypto for GBP | Capital Gains Tax on the gain |

| Swap one crypto for another | Capital Gains Tax on the gain |

| Spend crypto on goods or services | Capital Gains Tax on the gain |

| Gift to spouse or civil partner | Not taxed (no gain, no loss) |

| Gift to anyone else | Capital Gains Tax on the gain |

| Donate to a registered charity | Usually not taxed |

| Mining, staking, lending rewards | Income Tax at receipt, then CGT on disposal |

| Salary paid in crypto | Income Tax (and National Insurance) |

| Unsolicited airdrop | CGT only, on later disposal |

| Lost or stolen crypto | Not a disposal; a claim may be possible |

Keep this near you when you reconstruct your year. Most underpayments come not from hiding gains but from never realising a swap or a payment counted at all.

How to report crypto taxes to HMRC

This is the section other guides skip, and it is the one that actually gets you over the line. You report crypto by filing a Self Assessment tax return, and as of recently there is a dedicated place to do it.

The SA108 capital gains pages and crypto boxes

Capital gains go on the SA108 form, which sits alongside your main SA100 return. For the 2024/25 return onwards, HMRC added dedicated cryptoasset boxes, numbered 13.1 to 13.8, in the SA108 capital gains summary. They continue for 2025/26. You enter your number of disposals, total proceeds, allowable costs, and the resulting gains in those boxes. Crypto income, by contrast, goes in box 17 of the SA100 as other taxable income. Knowing the exact box saves you the guesswork that trips up first-time filers.

When you must report and the deadline

If you have never filed before, you must register for Self Assessment by 5 October after the tax year ends. The online return and any tax owed are both due by 31 January. You need to report crypto if your total proceeds for the year exceed £50,000 or your gains exceed the £3,000 allowance. Note that proceeds, not profit, is the trigger for one of those tests, so a busy trader can cross it without making much money at all.

If you already have unpaid crypto tax

Missed some past years? HMRC runs a dedicated Cryptoasset Disclosure Service for exactly this. Coming forward voluntarily almost always costs less than waiting for a letter. Which brings us to why waiting is now a bad bet.

New CARF rules to report crypto from 2026

For years the quiet assumption behind crypto tax non-compliance was simple: they will never know. From 1 January 2026, that assumption is finished.

Under the Cryptoasset Reporting Framework (CARF), UK crypto platforms must start collecting your data from the start of 2026, including your name, National Insurance number or tax reference, and your transaction details. Around 50 UK providers fall in scope. The first reports flow to HMRC in 2027, and providers face penalties of up to £300 per user for inaccurate or missing information, so they have a strong reason to collect it properly.

The effect is straightforward. HMRC will be able to cross-check what the exchanges report against what you declared on your SA108. Set that next to the 65,000 nudge letters already going out, and the direction is obvious. The data is coming to them automatically, so the safe move is to get your filing right before it does.

How much tax will you pay on crypto?

Numbers make this real. Say you sold crypto during the year for £20,000 in total proceeds, and your original cost was £12,000. Your gain is £8,000. Subtract the £3,000 allowance and you have £5,000 of taxable gain. What you pay depends on your income tax band.

| Your band | CGT rate | Tax on £5,000 gain |

|---|---|---|

| Basic rate | 18% | £900 |

| Higher or additional rate | 24% | £1,200 |

That is the core of it. The rate is set by your overall income, so a gain that pushes you from the basic band into the higher band can be taxed partly at each rate. If you are close to a threshold, the timing of when you sell genuinely matters.

Inheritance tax on crypto assets

Crypto does not escape your estate. When you die, your crypto assets are valued at the date of death and counted toward Inheritance Tax, charged at 40% on the part of an estate above the £325,000 nil-rate band. The practical danger is unique to crypto, though. If your heirs cannot find your private keys, the coins are valued for tax but lost in reality. Tell someone you trust where the keys are, or the taxman counts an asset your family can never actually claim.

How to legally reduce your crypto tax

None of this means paying more than you owe. There are legitimate levers that can meaningfully lower your tax bill, and using them is just sensible planning, not avoidance.

Use your £3,000 allowance every year, since it does not roll over. Report your losses too: capital losses offset gains, and once registered they carry forward for years, with a negligible-value claim available for coins that have effectively died. Transfers between spouses happen at no gain and no loss, which can double a couple's allowances and shift a gain to the lower-rate partner. And because the allowance resets each tax year, spreading large disposals across 5 April can keep more of the gain inside the tax-free band. Donating crypto to a registered charity is generally free of CGT as well.

Crypto tax tools and record-keeping

HMRC puts the record-keeping burden squarely on you, and it keeps no running tally on your behalf. You are expected to keep the date and pound value of every transaction, the type of asset, the number of units, and your pooled cost records. Do that across several wallets and exchanges and it becomes a real job.

This is why a crypto tax calculator is close to essential for active users. Tools like Koinly, CoinTracking, or Recap connect to your exchanges, track crypto across wallets, apply the share-pooling rules automatically, and produce a figure you can drop into the SA108 boxes. They cost money, but far less than getting the pooling wrong.

Getting your UK crypto tax right

UK crypto tax did not suddenly get harsher. It got visible. The rates are fixed, the £3,000 allowance is what it is, and the SA108 now has a box with your name on it. What changed is that from 2026 the exchanges start handing HMRC the receipts. So the real question is no longer whether they will find out. It is whether your return will already say the right thing when they look. File it, use your allowances, keep your records, and you never have to find out the hard way.