NOPAT: How to Calculate Net Operating Profit After Tax

Hand the same income statement to two analysts and ask each for the company's NOPAT. There is a decent chance you get two different numbers back. Not because one of them made a mistake, but because they picked different tax rates. That small choice is the part most explainers skip, and it is exactly the part that decides whether your figure is useful or misleading.

NOPAT, or net operating profit after tax, measures the profit a business earns from its core operations once taxes are taken out, as if the company carried no debt at all. It is one of the few numbers in finance that you cannot simply copy off a filing. You have to build it. By the end of this guide you will be able to calculate NOPAT two different ways, pull the inputs from a real company's income statement, and know which tax rate to use for the job in front of you.

What Net Operating Profit After Tax Means

NOPAT answers one narrow question. How much would this company's operations earn, after tax, if it carried no financing at all? Picture the business with the loans gone, the interest gone, and the one-off gains and losses that have nothing to do with daily operations gone too. What is left is the after-tax profit of the core operations. That is NOPAT.

That "as if debt-free" framing is the whole point, and it is what separates NOPAT from ordinary profit after taxes. Two companies can run identical operations and report very different net income simply because one borrowed heavily and the other did not. NOPAT erases that difference so you can compare the operating engines directly.

So interest expense is out, because interest is a financing cost rather than an operating one. Investment gains and other non-operating income are out too. And here is the catch most beginners trip on: NOPAT is not a line on any income statement. EBIT is printed there, net income is printed there, the tax expense is printed there. Net operating profit after tax is the one figure you assemble yourself from those pieces. Go looking for it in a filing and you will come up empty, which is exactly why the calculation is worth learning.

The NOPAT Formula and How to Calculate It

Two formulas, one number. Get in the habit of running both and checking that they meet in the middle. When they don't, you mislabeled something along the way, usually an interest or non-operating line that wandered into the wrong bucket. That reconciliation is the sanity check most people skip, and it is the one that catches the embarrassing errors.

| NOPAT formula | Inputs | What it strips out |

|---|---|---|

| EBIT × (1 − tax rate) | Operating income (EBIT), tax rate | Interest, taxes, non-operating items already gone |

| (Net income + interest expense + tax adjustments + non-operating items) × (1 − tax rate) | Net income, interest expense, non-operating income, tax rate | Adds back financing and one-offs, then re-taxes |

Method 1: starting from operating income (EBIT)

Start here: NOPAT = EBIT × (1 − tax rate). EBIT, earnings before interest and taxes, is what most statements simply call operating income, which is revenue after deducting cost of goods sold and operating expenses, before any interest or tax touches it. Multiply that operating income by one minus the tax rate. You have now taxed the operating profit on its own, without letting the company's debt load shrink the bill.

Method 2: building up from net income

If you only have the bottom line, you can work upward. Take net income, add back the interest expense, add back reported taxes and any non-operating items, which rebuilds operating profit, then apply the tax rate. The reason you add interest back on an after-tax basis matters: interest is tax-deductible, so borrowing creates a "tax shield" that lowers the real cost of debt. NOPAT deliberately ignores that shield, because it wants the operating result free of financing effects.

Which tax rate should you actually use?

Here is the question competitors tend to wave away. The simplest version uses the US statutory corporate rate, a flat 21% that the IRS has applied to tax years beginning after December 22, 2017, following the Tax Cuts and Jobs Act. But most companies do not actually pay 21%. Their effective tax rate, the figure you can back out of the income statement by dividing tax expense by pre-tax income, is often lower thanks to credits and foreign earnings.

My take, and it lines up with how practitioners treat the tax-rate choice: use the effective tax rate when you are comparing how profitable two businesses already are, because it reflects taxes they really pay. Use a normalized statutory or marginal rate when you are forecasting future cash flows in a discounted cash flow model, because today's tax quirks rarely last. The choice is not academic. It can move the NOPAT figure by billions, as the next example shows.

A Real NOPAT Example from Apple's Income Statement

Almost every NOPAT tutorial reaches for an invented company with round numbers, a tidy 50 dollars of operating income and a clean 30% tax rate. Real filings are messier, and the mess is instructive. So let's use Apple's actual fiscal 2024 results instead of a fictional one.

Pulling operating income from the filing

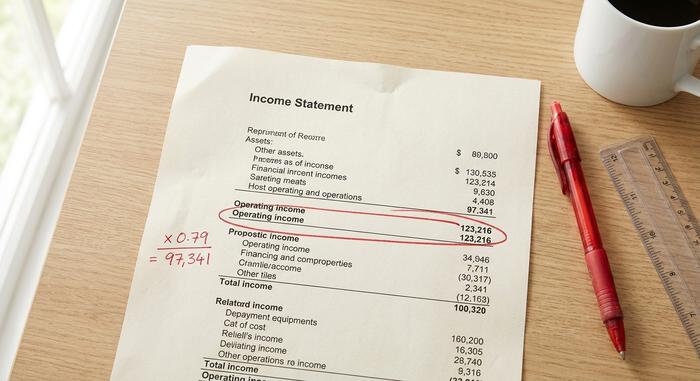

In its fiscal 2024 results, reported to the SEC, Apple posted operating income of $123,216 million (as of its September 2024 year-end). That is the EBIT figure, sitting on the income statement after cost of sales and operating expenses but before the company's interest and tax lines. This is the only number you need to fish out of the document for Method 1, which is part of NOPAT's appeal once you know where to look on the income statement.

Applying the tax rate to get NOPAT

Now apply the tax rate, and watch the choice bite. At the statutory 21%, NOPAT is $123,216 million × 0.79, or roughly $97,341 million. Use Apple's lower effective tax rate of about 17% instead, and NOPAT climbs to about $102,269 million. Same operating income, same company, same year, and the two NOPAT figures differ by nearly $4.9 billion purely because of which tax rate you trusted.

| Step | Line item | Value (Apple FY2024) |

|---|---|---|

| 1 | Operating income (EBIT) | $123,216M |

| 2a | Tax rate (statutory) | 21% |

| 3a | NOPAT = EBIT × (1 − 0.21) | ≈ $97,341M |

| 2b | Tax rate (effective) | ≈ 17% |

| 3b | NOPAT = EBIT × (1 − 0.17) | ≈ $102,269M |

Neither number is "wrong." They answer slightly different questions. That gap is the single best argument for understanding the tax-rate decision instead of plugging in 21% on autopilot.

NOPAT vs Net Income vs EBIT Compared

These three numbers get muddled constantly, and one of the most common search questions is whether NOPAT and EBIT are the same thing. They are not. EBIT is a pre-tax figure; NOPAT is EBIT after tax. Net income — the net profit figure at the bottom of every income statement — is the true bottom line: after interest, after the taxes actually paid, and after every one-off item. Here is the whole picture in one place, which is something most write-ups never put in a single table.

| Question | EBIT | NOPAT | Net income |

|---|---|---|---|

| Includes interest expense? | No | No | Yes |

| Reflects taxes? | No (pre-tax) | Yes (operating only) | Yes (as actually paid) |

| Capital-structure-neutral? | Yes | Yes | No |

| A line on the income statement? | Usually (operating income) | No, you build it | Yes |

| Best used for | Operating performance, pre-tax | Comparing operating engines after tax | Earnings to shareholders |

Read down the columns and the order makes sense. EBIT is operating profit before tax. NOPAT taxes that profit, so you see what the core business actually keeps. Net income then piles debt and everything else back on top. Why not just use net income, or any plain income-after-taxes figure? The third row answers that. Net income is not capital-structure-neutral, so it blends operating skill with financing choices you may not care about.

Why Analysts Use NOPAT as a Profit Metric

It comes down to comparability. Take two retailers with the same stores, the same margins, the same day-to-day operations. One is debt-free; the other borrowed heavily to expand. Their net income will split apart because of interest, even though the businesses are twins underneath. NOPAT drags them back onto level ground. That is why analysts lean on it to judge operational efficiency instead of financing strategy.

Real filings show the same effect. Microsoft reported operating income of about $109,433 million in its fiscal 2024 10-K; taxed at its roughly 18% effective rate, that works out to a NOPAT close to $89.5 billion. Set that beside Apple's NOPAT from earlier and you are comparing two operating engines on the same after-tax footing, with neither company's borrowing or share buybacks getting in the way. Net income alone would never let you do that cleanly, because the financing choices would bleed into the comparison.

---

That comparability is also why NOPAT feeds the NOPAT margin, calculated as NOPAT divided by revenue, a ratio most explainers skip entirely. It tells you how many cents of after-tax operating profit a company squeezes from each dollar of sales, with the debt noise removed. I find it more honest than net margin when you are stacking competitors against each other, because it isolates business performance from capital structure choices rather than rewarding a company simply for borrowing less. NOPAT keeps the focus on the profitability of the business itself and, ultimately, on the value created for the shareholder.

NOPAT in ROIC, EVA, and Free Cash Flow

NOPAT is rarely where the analysis ends. It is usually an input, the raw material for the metrics that actually move investment decisions. Three of those uses matter most.

NOPAT and return on invested capital (ROIC)

The headline use is return on invested capital. ROIC equals NOPAT divided by invested capital, the total of debt and equity put to work in the business. As Aswath Damodaran of NYU Stern lays out in his work on return measures, NOPAT is the correct numerator precisely because it is pre-financing: you are measuring the return the operations earn on all the capital, regardless of how that capital was raised. Pair an after-tax operating profit with the capital that produced it and you get a clean read on whether the company creates value.

Economic value added (EVA)

NOPAT also anchors economic value added. EVA equals NOPAT minus a capital charge, written as NOPAT − (WACC × invested capital). The idea, popularized through Stern Stewart and detailed in Damodaran's lectures, is simple: capital is not free, so subtract the cost of every dollar invested. If NOPAT clears that hurdle, the company added value in the period; if not, it destroyed value even while reporting an accounting profit.

Unlevered free cash flow and DCF

Finally, NOPAT is the seed of unlevered free cash flow, the cash measure used in most discounted cash flow valuations. You start from NOPAT, add back non-cash charges, then subtract reinvestment in working capital and capital expenditure to get the cash flows available to all investors. A DCF uses NOPAT rather than net income for the same reason ROIC does: it wants the free cash flow of the business before the financing decision, so the capital structure can be valued separately.

What NOPAT Leaves Out: Capital Structure and More

NOPAT's greatest strength is also its blind spot. By ignoring the amount of debt a company carries, it gives you clean comparability, but it also throws away the genuine tax benefits of borrowing, since interest really is deductible and really does lower a levered firm's tax bill. It leans on a chosen tax rate, so two analysts can publish different NOPATs for the same company without either being dishonest. And because it is not a GAAP figure, it tells you nothing on its own about capital expenditure or the cash a business consumes to keep growing. A capital-hungry manufacturer and an asset-light software firm can post the same NOPAT while reinvesting wildly different amounts to stay alive, and the metric will not warn you. That is why NOPAT almost never travels alone: analysts pair it with invested capital, reinvestment, and cash flow before drawing conclusions. NOPAT is a starting point, not a verdict.

The Bottom Line on Calculating NOPAT

NOPAT strips financing out of profit so you can see the operating business on its own terms, and it is only as good as the tax rate you feed it. Pick that rate to match the task: the effective rate when you are comparing companies as they are today, a normalized statutory rate when you are forecasting what they might earn tomorrow. Run both formulas, make them reconcile, and treat the result as the first question rather than the last. So the next time two analysts hand you different NOPAT numbers for the same firm, you will know exactly which lever they pulled, and which one you would have pulled instead.