Copper Price Prediction 2026–2030

Global copper dynamics have shifted from cyclical pricing to structural scarcity. Driven by electrification mandates, renewable energy scaling, and constrained mine supply, copper has moved into a multi-year high-demand environment with limited production acceleration. This forecast outlines concrete price expectations through 2030, integrating supply disruptions, reserve strain, trade conditions, and inventory tightening across the copper market.

Copper price, copper market and 2025 rally

The copper price environment entering 2025 represents a structural shift rather than a cyclical commodity upswing. The London Metal Exchange (LME) continues to report a high trading band, with copper near US$5.37 per pound and around US$11,145 per tonne in late‑2025. This pricing reflects tight inventory pressure, a rally in electrification, and ongoing supply disruptions affecting refined copper availability. The copper market now functions as a strategic foundation for global infrastructure rather than a basic materials segment.

Copper has become the central metal in the renewable energy transition. Every megawatt of new solar buildout, offshore wind cable expansion, and transmission‑line reinforcement adds incremental copper demand at an accelerating pace. This surge is supported by China’s utility reinforcement plans, North American grid hardening, and EU charging networks. The 2025 rally is therefore not a momentary spike but the result of tightening stockpile levels, confirmed mine disruption, and a shortage in refined copper processing.

Copper price and inventory metrics

|

Metric |

Value |

Market signal |

|

Copper price (per pound) |

US$5.37 |

Elevated and supply‑driven |

|

Copper price (per tonne) |

US$11,145 |

High vs 10‑year average |

|

LME stockpile |

Historically low |

Tighter inventory trend |

|

Rally effect |

Sustained, not peak |

Structural demand base |

2025 pricing aligns with deeper structural transformation. EV requirements alone are forecast to double copper consumption volume by 2027, while grid‑scale battery adoption adds a parallel consumption vector. These trends increase raw material strain on existing production streams and limit relief options in the near‑term.

Copper Price Prediction 2025–2030

The current price forecast places copper between US$10,500–13,000 per tonne in 2026, assuming continued electrification speed and ongoing mine delays. Analysts highlight that copper to average above historic norms through 2027 and 2028 due to supply squeeze conditions and rising reserve depletion.

Meanwhile, 2029 and 2030 are expected to stabilize at high pricing levels, not as cooling phases but as a plateau of future structural balance. Longer‑term structural constraints remain unchanged: high demand, insufficient mine turnaround, and slow‑moving procurement cycles.

Copper price forecast for 2025–2030

|

Year |

Average price forecast per tonne |

Price range per tonne |

Price per pound (approx) |

Key driver |

|

2025 |

US$11,000 |

US$10,800–11,300 |

US$5.00–5.40 |

Structural tightness, energy buildout |

|

2026 |

US$12,200 |

US$11,700–13,000 |

US$5.50–5.90 |

Electrification momentum, mine disruption |

|

2027 |

US$12,500 |

US$12,000–13,400 |

US$5.70–6.10 |

Reserve strain, delayed new capacity |

|

2028 |

US$11,600 |

US$11,100–12,400 |

US$5.15–5.65 |

Limited new ramp, not reversal |

|

2029 |

US$11,950 |

US$11,500–12,700 |

US$5.35–5.75 |

EV and power-grid reinforcement |

|

2030 |

US$13,100 |

US$12,600–13,900 |

US$5.90–6.25 |

Accelerated renewable energy investment |

Trade dynamics and investment positioning in copper

Investment flows toward copper futures, miners, and low‑carbon ETF commodities reflect bullish positioning. Global infrastructure packages favor copper because no other metal offers equivalent conductivity, longevity, and scaling in high‑voltage conditions. Investor exposure continues to build as portfolio managers seek leverage tools to manage energy transition volatility.

The future of copper pricing is no longer exclusively tied to cyclical industrial use. Instead, it sits at the heart of longer‑term structural electrification goals. The margin space created by 2025 pricing uplift allowed producers to reinvest, but reserve expansion remains slow relative to demand cycles.

Copper futures remain heavily traded, with buyer demand exceeding available refined volumes. This imbalance supports continued bullish outlook and reinforces the role of copper in multi‑asset portfolios.

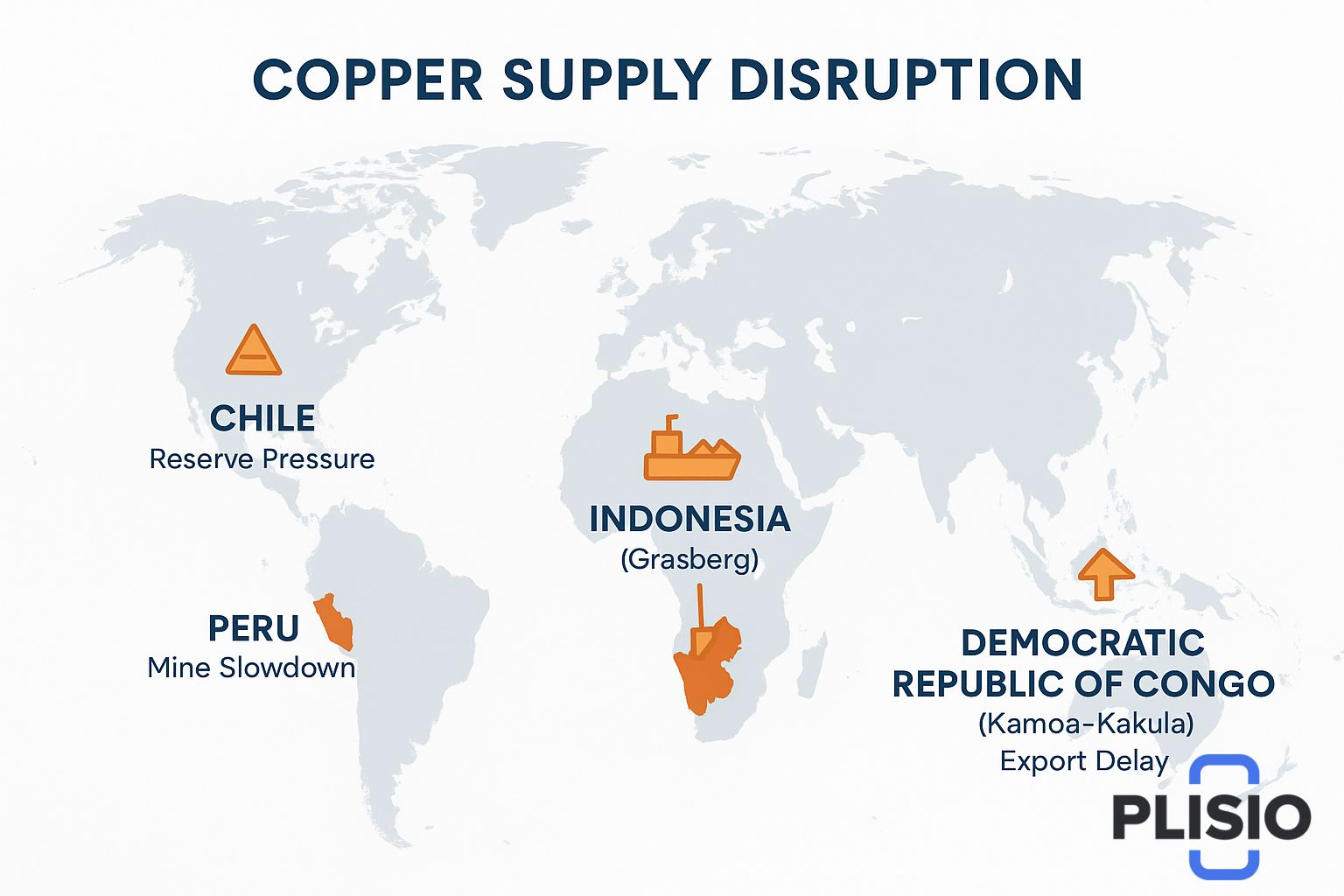

Supply disruptions, mine tension and reserve constraints

The worldwide copper map is defined by disruption: Chile, Peru, and the Democratic Republic of Congo each faced export turbulence and processing underperformance. Indonesia, especially via Grasberg in Indonesia, experienced repeated disruption windows. Kamoa‑Kakula output expanded but still trails aggregate demand.

Quebrada Blanca remains symbolic of project timeline friction: expansions exist, but regulatory pace yields delay. Forecast disruption risks into 2026 include labor negotiation cycles, stricter permitting, and environmental compliance.

Supply disruptions have reclassified copper as a raw material under strategic supervision rather than standard extraction. The export map shows tighter logistics, rising freight risk, and competition for smelting slots. These factors contribute to the 1.4 million‑tonne deficit hazard identified by multiple analyst groups.

Insight, structural outlook and future shortage conditions

Stockpile levels across LME storage continue marking new statistical lows. These numbers indicate tightening, not stabilization. Inventory signals reflect steady demand patterns, not excessive consumption. Longer‑term structural constraints tie copper scarcity to time: mine cycles require 7–12 years to reach refined output, and electrification deadlines do not wait.

The outlook for 2027, 2028 and 2029 anticipates a constrained high band. Renewable energy platforms use copper at exponentially greater intensity than legacy fuels. The shortage remains a functional engineering truth, not economic hype.

Raw pricing and refined capacity ensure copper remains a future‑secure asset. Import and export fluctuations contribute to global spread volatility, yet demand growth trends overpower softening variables.

Conclusion: 2030 vision and bull continuation arc

Copper enters 2030 as the decisive future conductor of electrification. Even if new mines accelerate, depletion and reserve access limit relief. Pricing may stabilize but not retreat, holding a plateau above late 2010s norms.

High capital expenditure, persistent electrification policy, and grid overhaul mean copper remains the central investment material of the coming decade. The rally of 2025 becomes the structural base, not the ceiling. LME screens show tightness, global production lags, and a supply chain under full transition pressure.

The prediction outlook remains bullish. Copper retains strategic status, and mine development advances too slowly to counter demand growth through 2030.