Withdraw Money from Robinhood: Banking, Trade, Desktop

Pulling cash out of Robinhood is straightforward most of the time and frustrating the rest of it. The app shows several different "cash" numbers, the SEC moved settlement to T+1 in May 2024, and a fresh ACH deposit can sit unwithdrawable for almost a week. None of that is documented well in one place. This guide is.

What you will find below: a step-by-step guide to every working way to withdraw money from Robinhood in 2026, the actual fee schedule by payment method, the daily and weekly transfer limits Robinhood publishes, the differences between iOS, Android, and desktop, the rules for crypto withdrawals, the list of reasons Robinhood blocks transactions, and a short FAQ at the end. Numbers are current to the April 2026 Robinhood Financial fee schedule.

Can you withdraw money from Robinhood?

Yes. Any verified Robinhood account can move money from your Robinhood account to a linked bank, to a debit card via instant transfer, to an external crypto wallet for crypto holdings, and (if you are closing the account) to another broker via ACATS. The withdrawal option you pick depends on your account type and how fast you need the money to land.

The only condition is that the cash you want to send out has to be withdrawable. That is not the same as the balance you see on the home screen. Cash sitting in unsettled trades, in pending deposits, or reserved by an open Good-Til-Cancelled order is not withdrawable until those statuses clear. The app shows a separate Withdrawable cash number on the Transfers screen, and that is the figure to trust.

If you just sold a stock that morning, the proceeds settle the next business day under T+1 rules. The cash will trade immediately, but it cannot leave Robinhood until settlement.

What you need to withdraw money from Robinhood

Three things, in this order:

- A verified Robinhood account, with identity checks done and no holds. Open the app and check Account Settings if you are not sure.

- A linked bank account, a debit card, or a Robinhood Wallet address (for crypto). Each one supports a different withdrawal type.

- Some cash available to withdraw, not just buying power. Margin balances, unsettled proceeds, and recently deposited funds on hold do not count.

Banking links break in the middle of a withdrawal more often than they break beforehand, so verify the bank account a few days in advance. A small test transfer of $1 confirms that routing and account numbers are correct without committing to a real amount.

Robinhood withdrawal limits in 2026

Robinhood publishes a clear ladder of transfer limits for standard bank transfers (ACH out) and applies it cumulatively across the brokerage, retirement, and spending accounts.

| Limit | Standard ACH out |

|---|---|

| Daily | $50,000 |

| Rolling 5 business days | $100,000 |

| Monthly | $250,000 |

The daily counter resets at 7 PM ET on business days. If you missed it on a Friday afternoon, you can still queue another transfer that night for processing first thing Monday. For larger amounts, splitting across multiple business days is the simplest path. For one-time large transfers, an outbound wire (separate flow) usually moves same-day.

A "$5 million in 5 business days" figure circulates on third-party blogs. It does not appear in current Robinhood Help Center documentation, so treat it as outdated. The published limits are what apply.

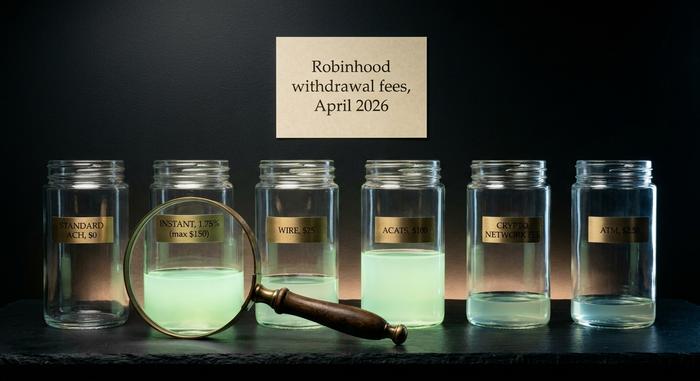

Does Robinhood charge a fee on withdrawals?

Most withdrawals are free. The exceptions are documented in Robinhood's Money Fee Schedule.

| Method | Fee | Notes |

|---|---|---|

| Standard ACH to bank | $0 | Default option, takes a few business days |

| Instant withdrawal | 1.75% (min $1, max $150 per transfer) | To debit card or RTP-eligible bank |

| Outgoing domestic wire | $25 | Same-day for large amounts |

| ACATS (account transfer to another broker) | $100 | Full or partial; per account |

| Crypto withdrawal to external wallet | $0 Robinhood fee | Network/gas fee paid in the asset itself |

| ATM withdrawal (Cash Card) | $2.50 plus operator fee | Free at 90,000+ Allpoint network ATMs |

Standard ACH is the right default for almost everyone. The 1.75% instant fee, with its $1 minimum fee, is reasonable for small amounts and brutal for large ones. A $10,000 instant withdrawal costs $150 and arrives in minutes. The same $10,000 by ACH costs nothing and arrives in 3 to 5 business days. Pick the withdrawal option that matches what your portfolio actually needs, not the fastest one available by default.

How to withdraw on iPhone, Android and desktop

The flow is consistent across all three. Menu labels differ slightly.

On iPhone

1. Open Robinhood and tap the account icon in the top corner.

2. Open the menu and tap Transfers.

3. Tap Transfer money and choose to send from Robinhood to your linked bank.

4. Enter the amount you want to withdraw. If you see a fee shown next to the amount, you have selected instant. Standard transfers do not show a fee.

5. Review the destination, the timing estimate, and any fee, then submit.

On Android

1. Open the app and tap the account icon.

2. Tap the menu, then tap Transfers.

3. Choose Transfer money and select your bank as the destination.

4. Enter the amount and pick standard or instant.

5. Review and submit.

On desktop

1. Sign in at robinhood.com on a browser.

2. Go to Transfers from the account area.

3. Pick the option to send money out to your linked bank.

4. Enter the amount, confirm the withdrawal method, and review any fee.

5. Submit and watch the status in your transfer history.

The destination bank and the timing estimate are the two things to double-check before submitting. Wrong-bank mistakes are the single biggest cause of stuck transfers.

Bank transfer vs instant withdrawal: which to use

The choice comes down to two questions: how fast do you need the money, and how much are you willing to pay for speed?

| Situation | Best option |

|---|---|

| You can wait 3-5 business days | Standard ACH (free) |

| You need money within an hour | Instant withdrawal (1.75% fee) |

| You are sending more than $50K | Wire transfer or split across days |

| You are funding an emergency | Instant if covered, otherwise call your bank for a same-day pull |

| You sold a stock today | Wait until T+1 settlement, then standard ACH |

A useful rule: instant only makes sense if the dollar value of the time saved is greater than the fee. Below $1,000 the fee is small enough to not matter much. Above $5,000 the math turns against instant fast.

How long does a Robinhood withdrawal take?

When you withdraw money from Robinhood, the timing depends on the transfer rail you picked. Typical numbers in 2026:

- Standard ACH to bank. Robinhood initiates within one business day. Receiving banks post within 1 to 4 business days after that. End-to-end you should see funds in 2 to 5 business days.

- Instant withdrawal. Usually under an hour, often within 5 minutes.

- Wire transfer. Same business day if submitted before the cutoff (typically early afternoon ET).

- ACATS to another broker. 5 to 7 business days.

- Crypto to external wallet. Minutes for fast networks (SOL, XRP, ETH on optimized days), up to an hour for BTC during congestion.

Weekends and bank holidays do not count as business days. A standard ACH submitted late Friday will not start moving until Monday morning. If you need money by Monday, send it before Thursday close.

Withdrawing crypto from Robinhood to a wallet

Robinhood enabled external crypto wallet withdrawals in 2022 and now supports roughly 30 assets. The list shifts over time, but core coins like BTC, ETH, SOL, XRP, LTC, BCH, DOGE, ETC, ADA, MATIC, USDC, AVAX, SHIB, LINK, UNI, AAVE, and COMP are supported.

Steps:

1. Open the coin's page in the Robinhood app.

2. Tap Send, paste the external wallet address, or scan the QR code from your wallet.

3. Enter the amount. Robinhood shows the estimated network fee, which is paid in the asset itself.

4. Confirm with two-factor authentication.

5. Wait for blockchain confirmations. BTC usually clears in 10 to 60 minutes, ETH in 1 to 5 minutes, SOL nearly instantly.

Robinhood does not charge its own fee for crypto withdrawals. You only pay the network gas fee, which is deducted from the amount you send. Sending 100 USDC on Ethereum uses up the gas in ETH from your Robinhood balance, not from the USDC itself for that token.

A few traps. Robinhood validates by address format, so a Bitcoin Taproot address (`bc1p...`) may not work in some flows; SegWit (`bc1q...`) and legacy formats (`1...` and `3...`) do. ERC-20 tokens must go to an Ethereum-network address; sending USDC to a BSC-network address loses the funds. New crypto purchases are sometimes locked for up to 5 business days before they can be withdrawn externally, the same hold logic as cash deposits.

The daily crypto withdrawal cap is roughly $5,000 worth for most accounts, rising with verified history.

Why your withdrawal might be blocked

If you cannot withdraw money from Robinhood right now, it is almost always one of a short list of well-defined reasons. Knowing the list saves a lot of frustrated app reloads.

- Recent sale not settled. Stock or option proceeds need T+1 to clear before that withdrawal amount is withdrawable.

- New deposit hold. ACH deposits are held up to 5 business days from the post date.

- You hit your daily limit. $50K standard ACH out per day, resets at 7 PM ET.

- Open GTC order reserves cash. The order holds buying power until you cancel it.

- Bank verification expired. Routing or account number changed, micro-deposits failed.

- Margin debit. Robinhood Gold users with negative cash cannot withdraw until cash goes positive.

- Day-trade call or PDT restriction. Pattern Day Trader rules can lock funds for 90 days.

- Reversed deposit. A bounced ACH freezes Instant Deposit and lengthens future holds.

The fastest diagnosis is the Withdrawable cash number on the Transfers screen. If that figure is lower than your account balance, one of the holds above is in play.

Withdrawable cash, cash balance and buying power

Robinhood shows three different cash-like numbers. They are not interchangeable.

- Buying power is what you can use to buy stocks, options, or crypto right now. On margin, it can include borrowed money.

- Cash balance is the cash sitting in your account, including unsettled deposits and unsettled sale proceeds.

- Withdrawable cash is the only one that can leave the platform. Settled, free of holds, free of pending orders.

For day-to-day use, focus on withdrawable cash when you plan to move money out and on buying power when you plan to trade. Mixing them up is how people end up confused that "their money is missing."

For a Robinhood Gold account using margin, the gap widens. Buying power can be 2x the cash balance. Withdrawable cash can be lower than both, since margin debit and outstanding equity loans block withdrawals. Depending on your account type, what shows as "cash" in one screen may not be the same amount of cash you can move out.

Robinhood Gold, banking and full account closure

Robinhood Gold ($5/month or $50/year) does not change the standard withdrawal mechanics, but it expands instant deposit limits, gives access to higher uninvested-cash yield, and unlocks Robinhood Banking. Brokerage operations are run by Robinhood Financial LLC; cash management and asset routing involve Robinhood Asset Management, with sweep banking through partner banks. Each affects which corporate entity is on the receipt side of a transfer.

Robinhood Banking launched in March 2025 for Gold members. It provides up to $2.5 million in FDIC insurance through a partner-bank sweep network, an introductory 4%+ APY on cash, and physical cash delivery in select cities. Banking withdrawals run on the same ACH and instant rails as the brokerage account, so the timing rules and limits behave the same way.

To close an account fully and move everything out:

- Cash-only exit. Sell all positions, wait for T+1 settlement, send all cash by standard ACH (free), and request closure under Account → Help → Close account.

- Transfer to another broker. ACATS the positions to Fidelity, Schwab, or another broker. Fee is $100 per account. Many receiving brokers reimburse this for transfers above $5K to $25K, so ask your new broker first. Crypto cannot be ACATS'd; sell or send to an external wallet first.

- After closure. Tax forms (1099-B for stocks, 1099-DA for crypto starting with 2025 reporting, 1099-INT for cash interest) still arrive next January even if the account is closed.

Tips and safety when you withdraw money from Robinhood

A handful of practical rules that prevent most issues.

- Verify the linked bank a few days before you need to use it. Re-linking mid-withdrawal slows everything down.

- Send a small test transfer ($1 to $5) before a large move. Cheap insurance.

- Avoid Friday afternoons. ACH cutoff plus weekend means a 4-day delay.

- Do not withdraw immediately after selling. Wait for T+1 settlement.

- Watch the 7 PM ET reset if you are pushing daily limits. A larger withdrawal split across two days lands cleaner than one rejection.

- Turn on two-factor authentication. The single biggest fraud loss vector is account takeover, not Robinhood itself.

- Double-check the destination on every transfer. Robinhood does not unwind a wire to the wrong account easily.

A short word on security. Robinhood is SIPC-insured for cash and securities up to $500,000 per account, with the Cash Sweep program adding pass-through FDIC coverage on uninvested cash held at partner banks. Crypto is not SIPC-protected. Robinhood Banking is FDIC-insured through its sweep network. Account-level security is real; behaviour-level security is on you. If you were inactive for 30 days or more before initiating a large transfer, expect an extra verification check. Same applies right after you change a password or add a new bank link.