Robert Kiyosaki Net Worth: Rich Dad, Poor Dad, Real Math

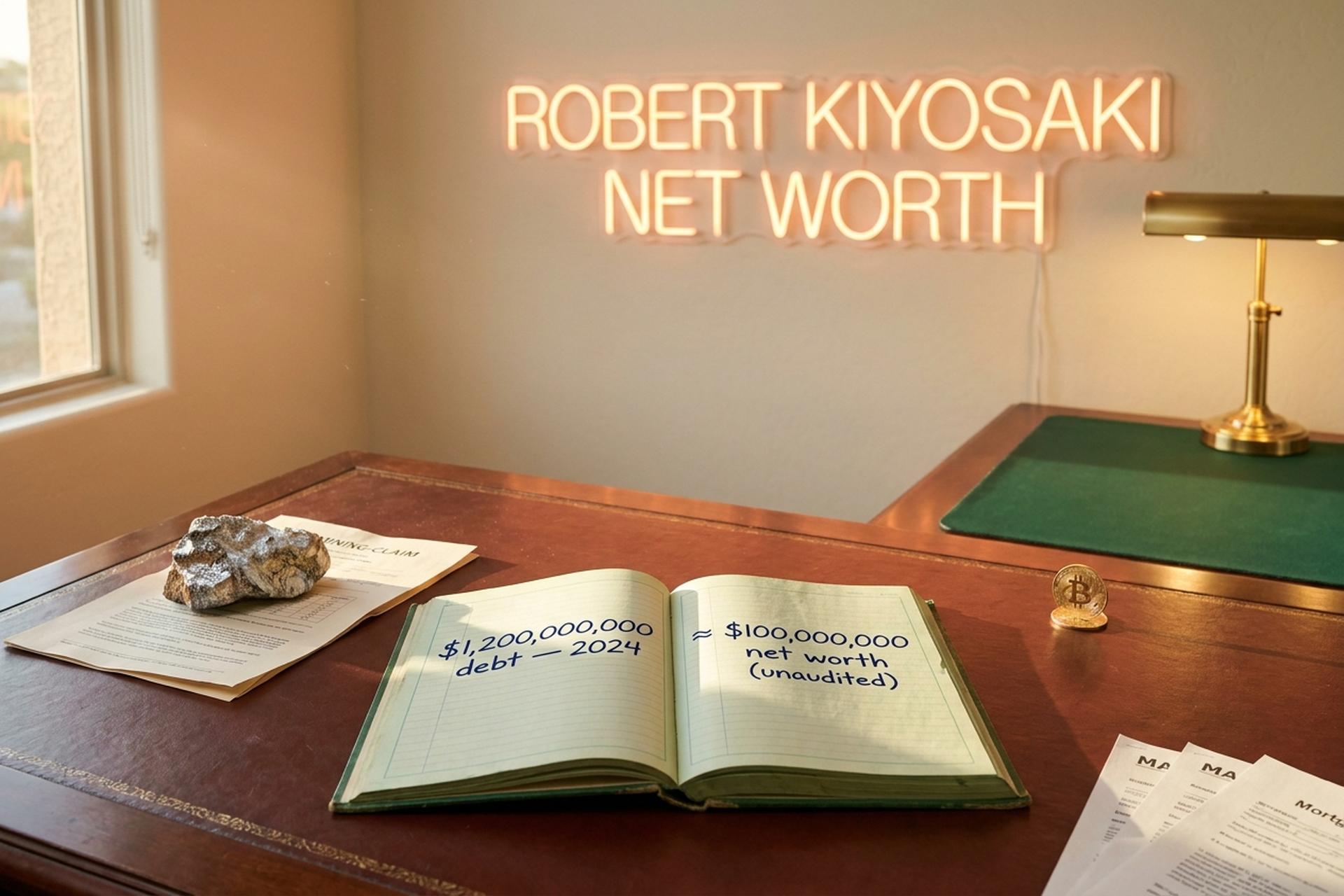

Robert Kiyosaki tells anyone who will listen that he is personally $1.2 billion in debt. He said so in a January 2024 Fortune interview, repeats it on his radio show, and has built half his recent social-media career around that single phrase. The other half rests on the claim that he is worth roughly $100 million. Both numbers come from him. Neither has been audited. And that — more than any single figure — is the most honest starting point for anyone trying to pin down Robert Kiyosaki net worth: the Rich Dad Poor Dad author and personal finance educator is the source, the brand, and the marketing department for his own balance sheet.

How Much Is Robert Kiyosaki's Net Worth in 2026?

Celebrity Net Worth puts his 2026 estimated net worth at $100 million. That is the number Yahoo Finance, MoneyWise, CoinGape and most other aggregators end up quoting. The ranges drift between $80 million and $120 million depending on how each estimator handles his real-estate debt. No audited figure exists. His companies are private. His real estate is mortgaged against the $1.2 billion debt load he keeps citing. His bullion and Bitcoin positions move daily. The $100M number, read honestly, is a vibe, not a balance sheet.

| Source | Net worth estimate | Method |

|---|---|---|

| Celebrity Net Worth | $100 million | Aggregated, not disclosed |

| Yahoo Finance / MoneyWise | $100–$120 million | Cites Celebrity Net Worth |

| Capitalism.com | $80 million (post-bankruptcy) | Older estimate |

| Wikipedia | "Estimated $100 million" | Cites Celebrity Net Worth |

Where the Rich Dad Fortune Actually Comes From

The Kiyosaki brand sells real estate, but the Kiyosaki bank account was built mostly on intellectual property and seminars. Rich Dad Poor Dad, self-published in 1997 and co-authored with Sharon Lechter, has sold more than 44 million copies worldwide by 2025, up from 40 million in 2017 and 32 million in 2014. It spent more than six years on the New York Times bestseller list. The Rich Dad Company, founded as Cashflow Technologies, Inc. in 1997, owns the brand, the licensing, the seminar pipeline, and the CASHFLOW board game that he and his wife Kim built the year before.

Royalties drive most of the headline cashflow. Court filings later showed that Rich Global LLC, one of the sub-companies that ran the seminar partnerships, earned roughly $45 million in Rich Dad seminar royalty income between 2007 and 2010, according to a Wall Street Journal account cited by ABC News. That single window is the cleanest public glimpse we have at the brand's earning power, because the rest sits inside private corporate structures with no SEC filings.

Around the books, Kiyosaki assembled a layered media business. He has authored more than 30 books in the Rich Dad series, including Cashflow Quadrant (2000), Rich Dad's Guide to Investing, Why the Rich Are Getting Richer, and Increase Your Financial IQ, plus two collaborations with Donald Trump tied to the 2016 presidential elections era: Why We Want You to Be Rich (2006) and Midas Touch (2011), the latter framed as a business ventures playbook for entrepreneurs. Some flopped. His 2024 release, Save Our Scruples, was reviewed harshly and barely registered on sales charts. The broader Rich Dad financial education catalogue, on the other hand, keeps moving steadily, decade after decade.

The seminar tier was, until the 2012 bankruptcy of Rich Global, where the real money sat. A starter event was sometimes free; the upsell to a multi-day workshop runs from $1,299 to over $10,000, and Wikipedia notes that the most premium offerings have been priced at $12,000 to $50,000 per attendee. Kiyosaki himself has functioned as the headline draw, equal parts educator, motivational speaker, and financial commentator, but the licensing structure means that Rich Dad Company collects revenue whether he personally appears or not.

Add the Cashflow game licensing, podcast advertising on the Rich Dad Radio Show, and Kim Kiyosaki's parallel Rich Woman franchise, and the picture clarifies. Kiyosaki's net worth is not the residue of a real-estate empire; it is the residue of a personal-finance media business that uses real estate as the brand promise.

| Income stream | Status | Notes |

|---|---|---|

| Rich Dad book royalties | Largest single contributor | 44M+ copies of RDPD; 30+ titles |

| Seminars and licensing | Historically huge | $45M in 2007–2010 alone (Rich Global) |

| CASHFLOW game | Steady | Co-created with Kim Kiyosaki in 1996 |

| Real estate cash flow | Significant but levered | Self-reported 7,000–15,000 units |

| Mining, oil, BTC | Volatile | Disclosed publicly; quantities mostly vague |

Real Estate, Gold, Silver, and Bitcoin Investments

Kiyosaki's portfolio philosophy is consistent. The numbers attached to it are elastic. He owns rental real estate spread across Scottsdale, Virginia, Georgia, Colorado and Nevada, and he has talked about that portfolio in interviews for two decades. The count keeps drifting upward. He has cited 6,500 rental units, then 7,000, then 12,000, and most recently 15,000 (Yahoo Finance, 2024). None of those figures appears in a public registry. The way the number escalates across interviews is a credibility flag worth naming directly. I'm not convinced the largest count is the literal one.

His first property, he says, was a four-unit building in Hawaii bought at age 26 for $45,000. The $1,000 down payment, by his own telling, went on a credit card. That is the story he uses on stage to demonstrate the use of other people's money. He scaled into a 12-unit complex bought at $300,000 and sold at $495,000, then a 30-unit building that generated $5,000 a month and sold for $1.2 million. Those numbers are checkable in old interviews. The 15,000-unit total is not.

Precious metals get even fuzzier. Kiyosaki says he started "stacking silver" in 1965 and considers it the lowest-risk, highest-upside trade available. Ounces? Never disclosed. What is verifiable is that he owns mining stakes, not only paper bullion. In a March 2024 post on X he wrote: "I own gold and silver mines… I also own oil wells." He took Utah's Trixie Mine public in July 2023. He previously owned a silver mine in Argentina, since sold to Yamana Gold.

Bitcoin is the position with the cleanest paper trail. On X in November 2024 he disclosed owning 73 BTC and said he wanted to reach 100. A year later, in November 2025, he posted that he had sold $2.25 million worth of Bitcoin near $90,000 per coin and rotated the proceeds into private businesses. He framed it as taking profits rather than walking away. The math: roughly 25 BTC sold, with the holding probably closer to 48 BTC today, though the precise post-sale balance is unconfirmed. Kiyosaki has also said he stopped buying around $6,000 a coin. That aligns with a late-2017 entry. Not the Satoshi-era myth that sometimes attaches to his brand.

| Asset class | Claimed position | Verifiability |

|---|---|---|

| US rental real estate | 15,000 units (2024 claim) | Self-stated; not audited |

| Bitcoin | 73 BTC (Nov 2024); ~48 BTC after Nov 2025 sale | Self-disclosed via X |

| Gold and silver bullion | Undisclosed quantities | Self-stated only |

| Mining stakes | Trixie Mine (Utah, public July 2023); ex-Argentina silver mine | Yes, public filing |

| Oil wells | Owned (March 2024 statement) | Self-stated |

| Personal debt (acquisition vehicle) | $1.2 billion | Self-stated, Fortune Jan 2024 |

The Crypto Pivot: From Rich Dad to Bitcoin Bull

The crypto pivot is recent. It is verbal, not foundational. Kiyosaki's argument runs roughly as follows: Bitcoin sits outside the Fed, the Treasury, and Wall Street, so it works as a hedge against what he calls the "fake money" system. His price forecasts have multiplied since 2023, posted on X to more than a million followers.

The track record on those forecasts is uneven. His June 5, 2024 tweet (status 1798476195232973066) predicted Bitcoin at $350,000 by August 25, 2024. BTC traded near $60,000 on that date. The $100,000 call for June 2024 was directionally right but arrived around December, six months late. The $250,000 by end-2025 target did not happen. The $1 million by 2030 line is unfalsifiable until then. On silver, he tweeted in April 2025 that the metal would reach $70. It did. He then raised the bar to $200 by 2026 (BusinessToday, November 25, 2025). The "Biggest Crash in History Starting" post that same month (status 2031201177808056686) was the loudest version of an apocalyptic stance he has been amplifying for years.

So: often directionally right, routinely wrong on timing. That matters when timing is what an investor is paying for. Followers who acted on his August 2024 deadline locked in losses that the December rally did not undo.

The Rich Global Bankruptcy and Seminar Money Trail

The 2012 bankruptcy is the part of the Kiyosaki story that defenders skip and critics over-state. Both miss the detail. Rich Global LLC, a sub-company licensed to run Rich Dad live seminars in partnership with The Learning Annex, filed Chapter 7 in Wyoming on August 20, 2012. A U.S. District Court ruling by Judge Shira Scheindlin had earlier confirmed a judgment of $23,687,957.21 against Rich Global, over a revenue-share dispute tied to a 2002 Madison Square Garden seminar. Rich Global listed roughly $26 million in liabilities against $1.8 million in assets at filing. CEO Mike Sullivan publicly described the entity as having been "dormant for years."

The detail that matters: Rich Global was the entity that went bankrupt, not Robert Kiyosaki personally, and not the parent Rich Dad Company. The parent company kept its brand, its book royalties, and its broader licensing structure intact. The entity that took the hit was a designated licensing arm. So when commentators describe Kiyosaki as having "gone bankrupt," they conflate a sub-company default with personal insolvency. What the filing does show, and what Kiyosaki's own debt philosophy makes uncomfortable to digest, is that the same company that paid out $45 million in royalties between 2007 and 2010 walked into bankruptcy with $1.8 million in recoverable assets two years later.

Critics, John T. Reed, and the Financial Advice

John T. Reed is the critic to start with. A real-estate writer with no obvious axe to grind, he posted a multi-part teardown of Rich Dad Poor Dad on his own site. His central charge is that the mentor figure may not exist. He notes that Kiyosaki's 1992 book dedicates the phrase "best teacher I ever had" to his biological father, Ralph, while the 1997 book reassigns that same phrase to the unnamed Rich Dad. He accuses the book of nudging readers toward questionable tax and securities tactics. A Honolulu Star-Bulletin investigation could not pin down the real Rich Dad either. Later coverage floated businessman Richard Kimi as a possible match. None of that has been confirmed.

The TV networks weighed in too. CBC Marketplace ran a 2010 investigation in Canada documenting seminar upsell tactics that delivered very little. CBS News carried an Allan Roth piece the same year. Class-action complaints by attendees who said they did not get rich as promised settled.

The cleanest illustration of the disagreement is personal-finance commentator Dave Ramsey. Ramsey wants you debt-free. Kiyosaki wants you debt-rich, as long as the debt buys assets that pay you. Both built huge brands. Only one of them has filed a corporate Chapter 7.

Cashflow Quadrant and Kiyosaki's Debt Doctrine

The Cashflow Quadrant, introduced in his 2000 book, is the framework most students of Kiyosaki actually take with them. It splits income into four categories and asks readers which side they want to live on:

- E (Employees): earn by working for someone else

- S (Self-employed): work for themselves and trade time for money

- B (Business owners): own systems that earn whether they show up or not

- I (Investors): earn from invested capital

The argument behind the quadrant, that moving from the active-income left side to the passive-income right side is the path to financial independence and the entrepreneurship route used to build wealth, is the durable contribution. Financial literacy, in Kiyosaki's framing, is the prerequisite for any of those moves. The debt doctrine, by contrast, is contested: "good debt" buys assets that pay you, "bad debt" pays for liabilities. Whether the average reader can execute the first without first becoming the second is the point critics keep returning to.

For all the noise, the headline number, Robert Kiyosaki net worth at around $100 million, remains a guess made up of guesses. The provable parts are the 44 million books, the brand, the bankruptcy of one of his sub-companies, and a $1.2 billion debt balance he has chosen to publicize. The unprovable parts are the rental count, the bullion stack, and most of the future price targets. The reasonable question is whether to take financial advice from someone whose own balance sheet you cannot verify, and to weigh that against the parts of his thinking, the quadrant and the asset-vs-liability framing, that have helped readers think more clearly about their own money for nearly thirty years.