How to Buy Bitcoin Anonymously with a Credit Card

The short answer: you probably cannot. Not truly anonymously. A credit card has your name, your bank, your address, and a transaction record that lives on servers you do not control. Attaching that to a Bitcoin purchase creates a trail. Period. Anyone who tells you otherwise is selling something.

The longer answer: you can get close. Reduced KYC platforms, prepaid cards bought with cash, P2P marketplaces, and crypto swap services can limit how much personal information you expose when you buy bitcoin. None of them make you invisible. But some of them make you harder to trace. In a world where EU's MiCA regulation now mandates KYC for every crypto transaction through regulated providers, and 85 of 117 FATF jurisdictions have passed or are passing Travel Rule legislation, "harder to trace" is the realistic goal.

This guide covers every method that still works in 2026, what it costs, what the risks are, and why buying bitcoin anonymously with a credit card is getting harder every year. I also need to be direct about something: Bitcoin itself is pseudonymous, not anonymous. Every transaction you make is recorded on a public ledger forever. If your identity gets linked to a wallet address once, your entire transaction history becomes visible. Keep that in mind.

Why people want to buy bitcoin without verification

Privacy is not the same as criminality. Most people who want to buy btc without verification have straightforward reasons.

Some live in countries where buying crypto can attract unwanted government attention. Some freelancers earn in crypto and do not want every purchase linked to their real name. Some people just believe their financial transactions are nobody's business. That is a legitimate position. The right to financial privacy exists in many legal frameworks even if the infrastructure to exercise it is shrinking.

Others want to avoid the data breach risk. Every exchange that collects your passport, selfie, and proof of address creates a database that hackers target. Ledger's customer database leak in 2020 exposed 272,000 customer records including physical addresses. People received death threats. The KYC data that exchanges collect is a liability, and some crypto users prefer not to create that liability in the first place.

Then there are the people trying to evade taxes or launder money. They exist. Regulators know they exist. That is why KYC requirements keep tightening. The actions of bad actors are the reason everyone else faces more verification. Fair or not, that is the reality.

Methods to buy bitcoin anonymously with a credit card

Here is every method that offers some level of reduced identification, ranked from most to least practical.

Reduced-KYC swap services for small amounts

Several crypto swap services allow credit card purchases under small thresholds without full identity verification.

| Platform | KYC threshold | Credit card support | Max without ID |

|---|---|---|---|

| Changelly | None under $150 | Yes (direct) | $150 per transaction |

| ChangeHero | None under $700 | Yes (direct) | Up to $700 |

| MoonPay (Level I) | Email + phone only | Yes | $150/month, $50 per purchase |

I tested Changelly myself. Email, card number, wallet address. Done in under three minutes. No selfie. No passport. Bitcoin arrived in my wallet about 15 minutes later. The fee was roughly 4% all-in, which stings but works.

The catch nobody mentions: your credit card is not anonymous. Your bank sees "Changelly" on the statement. The swap service logs your email and IP. You skipped the passport upload, sure. But the paper trail is shorter, not gone. For small amounts where you just do not want your face in another exchange's database, this is the most practical path forward.

No-KYC exchanges with third-party card processors

A handful of exchanges let you sign up with just an email and purchase bitcoin through integrated payment processors.

| Exchange | Signup requirement | Card processor | Withdrawal limits |

|---|---|---|---|

| MEXC | Email only | Third-party (Simplex, etc.) | 10 BTC/day |

| BingX | None required | Third-party | Generous |

| PrimeXBT | None by default | Third-party | $20,000/24h |

Here is what burned me on my first try: the exchange asked for nothing. Email and go. But the moment I clicked "Buy with Card," a Simplex popup appeared asking for my passport photo. The exchange was no-KYC. The payment processor was not. Simplex, MoonPay, and Transak each follow their own compliance rules. Even if MEXC never asks for your ID, the payment gateway might. You could get halfway through a purchase and hit an ID verification wall from the processor, not the exchange.

Prepaid cards plus no-KYC platforms

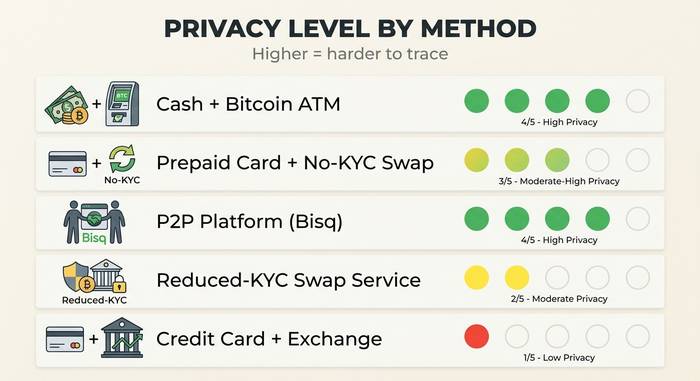

Buy a prepaid Visa or Mastercard with cash at a convenience store. Use it on a reduced-KYC platform. The card is not linked to your bank account or your name. This is the closest a credit or debit card method gets to anonymity.

Limitations: prepaid cards typically cap at $200 to $500. Many crypto platforms reject prepaid cards. Transaction fees stack (the card fee plus the platform fee). And if the prepaid card requires activation with personal information, the anonymity benefit disappears.

This method works for small amounts. It is slow, expensive, and tedious for anything larger than a few hundred dollars.

P2P platforms for privacy-focused buyers

Peer-to-peer marketplaces connect you directly with a seller. The platform holds the bitcoin in escrow until both sides confirm the transaction. Most P2P platforms do not accept credit cards directly, but some sellers accept PayPal, Revolut, or bank transfers initiated from a card.

| Platform | KYC | Payment methods | Fees | Status |

|---|---|---|---|---|

| Bisq | None | Bank transfer, Zelle, Revolut, cash | 1.3% split | Active, decentralized |

| Hodl Hodl | Email only | 100+ currencies, SEPA, PayPal | Max 0.6% split | Active (not in US) |

| Peach Bitcoin | None | Revolut, PayPal | 0% | Active |

| RoboSats | None | Lightning Network P2P | 0.2% split | Active |

| NoOnes | Varies | 250+ payment methods | Varies | Active (Paxful successor) |

LocalBitcoins shut down in February 2023. Paxful shut down on November 1, 2025, after FinCEN fined them $3.5 million for facilitating $500 million in illicit activity. The P2P space is smaller than it was two years ago. Bisq remains the gold standard for decentralized, no-KYC bitcoin buying, but it does not support credit card purchases directly.

Bitcoin ATMs with minimal verification

Nearly 39,000 Bitcoin ATMs exist worldwide, with 77.7% of them in the United States. Most accept cash, not credit cards. A few operators like CoinFlip accept debit cards at select locations, but credit card acceptance at ATMs is rare.

For small transactions (under $250 to $900 depending on the operator), many ATMs require only a phone number. Larger amounts trigger government ID requirements, selfie verification, or facial recognition.

The fees are brutal. Bitcoin ATM operators typically charge 8% to 20% above market price. And the scam statistics are alarming: Bitcoin ATM scams cost Americans $333 million in 2025 according to FBI data. If someone tells you to deposit cash into a Bitcoin ATM to pay a bill, settle a debt, or "protect your account," it is a scam. Always.

What the regulations say in 2026

I want to be blunt about what the law looks like right now.

| Region | What changed | What it means for you |

|---|---|---|

| EU | MiCA + Transfer of Funds Regulation | Every crypto platform must ID you. Zero exceptions. Privacy coins banned. |

| US | FinCEN BSA + IRS Form 1099-DA | Exchanges report your trades to the IRS starting 2026. Travel Rule at $3,000. |

| UK | FCA crypto regime (2026) | Travel Rule active. All crypto ads need FCA approval. |

| Global | FATF Travel Rule | 85 out of 117 countries are passing this into law. The net is getting wider. |

The EU hit hardest. MiCA Phase 2 went live December 30, 2024. Every crypto service provider in Europe must now collect your name, address, and ID for every transaction. Not just big ones. Every one. Send BTC from an exchange to your own wallet? If the amount exceeds EUR 1,000, the exchange must verify that you actually own that wallet. Monero and Zcash? Banned from exchange accounts entirely. By July 1, 2027, anonymous wallets through any regulated provider will be illegal across the EU.

In the US, the IRS decided crypto is property. Taxable property. The new Form 1099-DA means Coinbase, Kraken, and every other US exchange will send your trading data straight to the IRS starting this year. Buy bitcoin anonymously on a P2P platform, then move it to Coinbase to sell? The IRS sees the sale. The "anonymous" part only delayed the paper trail. It did not prevent it.

Privacy wallets and what happened to them

So you bought bitcoin with reduced verification. Where do you put it?

Electrum. Sparrow. BlueWallet. All non-custodial. All free. None of them ask for your name. You download the software, it generates a wallet address, and you hold your own keys. Nobody between you and your coins.

The privacy wallet space used to go further. Wasabi Wallet mixed your transactions with other users through CoinJoin, scrambling the trail. Samourai Wallet did something similar with extra features on top. Both sounded like exactly what a privacy-focused buyer would want.

Then the government showed up. November 2025: Samourai Wallet's developers got 4 to 5 years in federal prison. Money laundering conspiracy. Unlicensed money transmission. Done. Wasabi saw what happened and blocked all US users. March 2026, the US Treasury said something surprising: mixers have "legitimate uses." But by that point two developers were already in prison, so the signal was mixed at best.

What works today without legal risk: a simple non-custodial wallet. No mixing. No CoinJoin. Just hold your keys, use Tor or a VPN when you connect, and never reuse a wallet address. These boring steps do more for your privacy than any fancy tool that might put you on a regulator's radar.

Risks and scam warnings you need to read

Buying bitcoin anonymously carries real risks beyond legal exposure.

No recovery options. If someone scams you on a P2P platform, steals your prepaid card details, or sends you fake bitcoin, there is no customer support line that will get your money back. Anonymous transactions mean anonymous counterparties. That cuts both ways.

Scam scale in 2025 was massive. Chainalysis data shows $17 billion stolen in crypto scams. Bitcoin ATM scams alone hit $333 million. AI-enabled scams, where scammers use deepfakes to impersonate customer support or trusted contacts, are now 4.5 times more profitable than traditional methods.

Regulatory risk. Even if you buy bitcoin anonymously today, regulations can change tomorrow. Several jurisdictions are implementing retroactive reporting requirements through DAC8 and CARF. Your anonymous purchase may not stay anonymous if the platform you used eventually complies with information requests.

Price volatility still applies. Whether you buy through Coinbase with full KYC or through Bisq with none, Bitcoin's price moves the same. Paying a 15% premium at a Bitcoin ATM for "anonymous" access means you start 15% in the hole before price movement even matters.

My honest advice: for most people, the privacy gains of anonymous purchase methods do not justify the higher fees, lower liquidity, increased scam risk, and legal uncertainty. If your concern is data breach risk from KYC, use a reputable exchange with strong security, enable 2FA, and accept that the exchange has your identity. If your concern is genuine, the prepaid card plus reduced-KYC swap service route works for small amounts. For anything above a few hundred dollars, the trade-offs get ugly fast.