Meaning of Recession and Its Economic Impact

A recession is a phase in the business cycle marked by a significant decline in economic activity spread across the economy. Economists typically identify a recession when gross domestic product (GDP) or real income falls, industrial production slows, and the unemployment rate rises notably. Historically, downturns are followed by recovery, and the U.S. economy has emerged from every recession since the Great Depression of the 1930s. According to 2025 Bureau of Economic Analysis estimates, U.S. GDP growth averaged 2.1% in 2024 before slowing to 1.2% annualized in Q1 2025 amid tightening financial conditions and elevated interest rates.

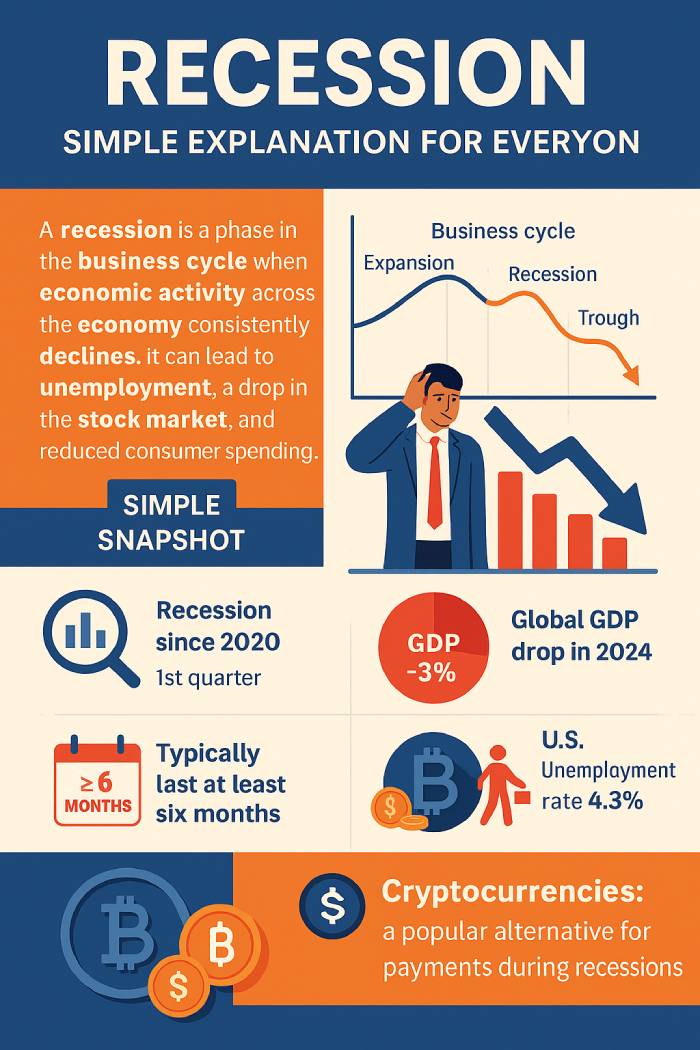

Recession Definition and Economic Activity

In economic terms, a recession is a significant contraction that affects demand for goods and services, hiring, production, and household spending. In the U.S., the National Bureau of Economic Research (NBER) - specifically its Business Cycle Dating Committee - is responsible for determining when a recession starts and ends. While many refer to two consecutive quarters of negative GDP growth as the standard recession definition, the NBER looks beyond GDP alone. It considers:

- Real income level shifts

- Job losses and unemployment trends

- Industrial production data

- Wholesale and retail sales

- Inflation-adjusted consumption behavior

This broader approach exists because the economy was not in recession every time GDP dipped, nor did every GDP dip translate into lasting contraction.

Recession vs. Depression Across the Business Cycle

A depression is not just a recession - it is a severe recession lasting months or even years, often spreading across multiple advanced economies. The Great Depression stands as the most notable example, with unemployment soaring and economic output collapsing globally. By contrast, the COVID‑19 pandemic resulted in a two‑month recession(February to April 2020) despite steep, sudden declines in GDP growth. The 2025 NBER update notes that real GDP fell 31% at peak lockdown contraction, marking the sharpest quarterly drop in recorded U.S. economic history, even though recovery was swift by comparison.

Indicators of an Impending Recession

Visual Snapshot: Core Signals 2023-2025

- GDP growth: 2.1% → 1.2%

- Unemployment: 3.7% → 4.6%

- Consumer confidence index: down 14% since late 2023

- Yield curve inversion: longest stretch since 2007

- Equity volatility: +22% YoY increase in VIX

These indicators collectively illustrate cooling demand, tightening credit conditions, and rising recession expectations.

Economists track several economic indicators to forecast a potential recession. In 2025, analysts at the Federal Reserve Bank of St. Louis highlighted that:

- the unemployment rate rose from 3.7% in late 2023 to 4.6% in early 2025

- core inflation remains above target at 3.4%, despite aggressive rate policy

- yield curve inversion has persisted for 19 months, the longest since the Great Recession

- household consumer spending slowed by 1.9% year‑over‑year, marking the steepest decline since 2009

Key warning indicators include:

- Decline in stock prices and investor confidence

- Rise in unemployment and reduced hiring

- Drop in real income and household buying power

- Lower industrial production of goods and services

- Yield curve inversion suggesting expected downturn

- Inflation or deflation pressure, impacting consumer spending and borrowing

Periods of marked slippage in economic activity often reflect tightening of credit, slowing trade, and weaker financial conditions across the economy.

What Can Lead to a Recession

Global Comparison (2023-2025)

- EU: inflation pressure persists; ECB slower to cut rates

- UK: wage growth cooling but energy‑driven inflation remains

- Japan: moderate price growth but weak yen squeezes imports

- Canada: housing‑linked sensitivity raises downside risk

Different monetary tools and structural markets explain why recessions hit national economies unevenly.

Recessions can be triggered by multiple forces, including:

- Raising interest rates to control inflation

- Money supply contraction driven by central banks

- Unexpected shocks such as war, energy crises, or a pandemic

- Asset bubbles fueled by speculative investment

- A decline in consumer demand for essentials and durable goods

In the early 1980s, rapidly increasing oil prices and restrictive credit conditions led to a downturn, while the Great Recession (2007-2009) emerged from housing market failure and weakened global banking structures.

Effects of a Recession on the Country's Economy

Labor Market & Cost‑of‑Living Tensions

- underemployment grew by 2.4% in 2024-2025

- wage growth slowed from 5.2% → 2.9%

- job switch premium dropped by 37%

Post‑pandemic labor dynamics remain fragile, especially in logistics, retail, and corporate services.

As economic output slows and companies adjust, common effects include:

- Higher unemployment rate and hiring freezes

- Lower consumer spending and wage stagnation

- Drop in corporate earnings and investment

- Tighter access to credit and higher borrowing stress

- Contraction in trade and industrial activity

A prolonged downturn can lead to a recession turning into a depression, though such events remain rare since the Great Depression. As of 2025, the IMF notes that only 2 out of 21 advanced economies show conditions aligning with what could become a severe recession, emphasizing that structural safeguards have reduced depression‑level risk.

How to Prepare for a Recession

Consumer Behavior Shifts 2024-2025

- 54% paused big‑ticket purchases

- 66% switched to discount goods providers

- subscription cancellations up 31%

Myth‑to‑Fact Clarifications

- Myth: all sectors collapse → Fact: utilities and healthcare remain resilient

- Myth: recessions equal depressions → Fact: downturns typically last months, not years

- Myth: the stock market = the economy → Fact: markets recover earlier than GDP does

To manage financial risk during downturns, individuals often adjust based on current data. In 2025, Bank of America reported that 72% of U.S. households are actively building savings buffers and 54% reduced discretionary spending in anticipation of continued tightening.

- Build savings to last at least six months

- Pay down debt to reduce vulnerability

- Diversify income and investments

- Avoid reacting emotionally to bear markets

- Study the broader economic life cycle to stay informed

A practical rule of thumb is maintaining liquidity, reducing spending, and strengthening professional networks to endure job losses or wage reductions.

Business Cycle Patterns and the Last Recession

Human‑Level Case Examples

- Tech: hiring freezes & slower venture capital deals

- Luxury: resilient demand among upper‑income cohorts

- Auto: price normalization post‑chip shortage bubble

Different sectors absorb contraction at different speeds, explaining why recessions feel uneven to households.

The business cycle features recurring stages:

- Expansion: demand for goods and services accelerates

- Peak: the economy reaches a peak before cooling

- Contraction: economic activity slows, leading to decline

- Trough: the lowest point before growth returns

Recovery typically lasts longer than decline, which explains why recessions have occurred less frequently than expansions in most 21 advanced economies.

Beyond 2020: Why the Cycle Didn’t Reset

- hybrid work reshaped office demand

- de‑globalization redrew supply chains

- service inflation proved more persistent than goods inflation

The post‑COVID‑19 recession era diverged from pre‑2019 norms, underscoring a slower path back to low‑inflation equilibrium.

Every recession since formal economic tracking began has eventually given way to renewed growth. While downturns may lead to lower spending, rising costs, and shrinking employment, they also correct imbalances and reset financial systems. Staying informed about recession indicators, policy responses from central banks, and historical patterns can help you prepare for a recession with clarity rather than fear.