Lithium Price Prediction 2026-2030

The global lithium market update in late 2025 reflects a sector that has matured rapidly yet still carries the nascency of the lithium market in its volatility. Lithium is no longer just a raw material; lithium has become a strategic resource powering an unprecedented surge in EV, energy storage, battery technologies and electrification programs worldwide. Analysts said lithium will remain central to the energy transition as lithium supply, lithium demand and global lithium production scale to meet forecasts that project at least 20 million units in 2025 of EV sales. Lithium prices remain under pressure amid oversupply, but strong long-term lithium growth forecasts endure, and demand expected to accelerate beyond 2030 and new supply projects continue to reshape expectations.

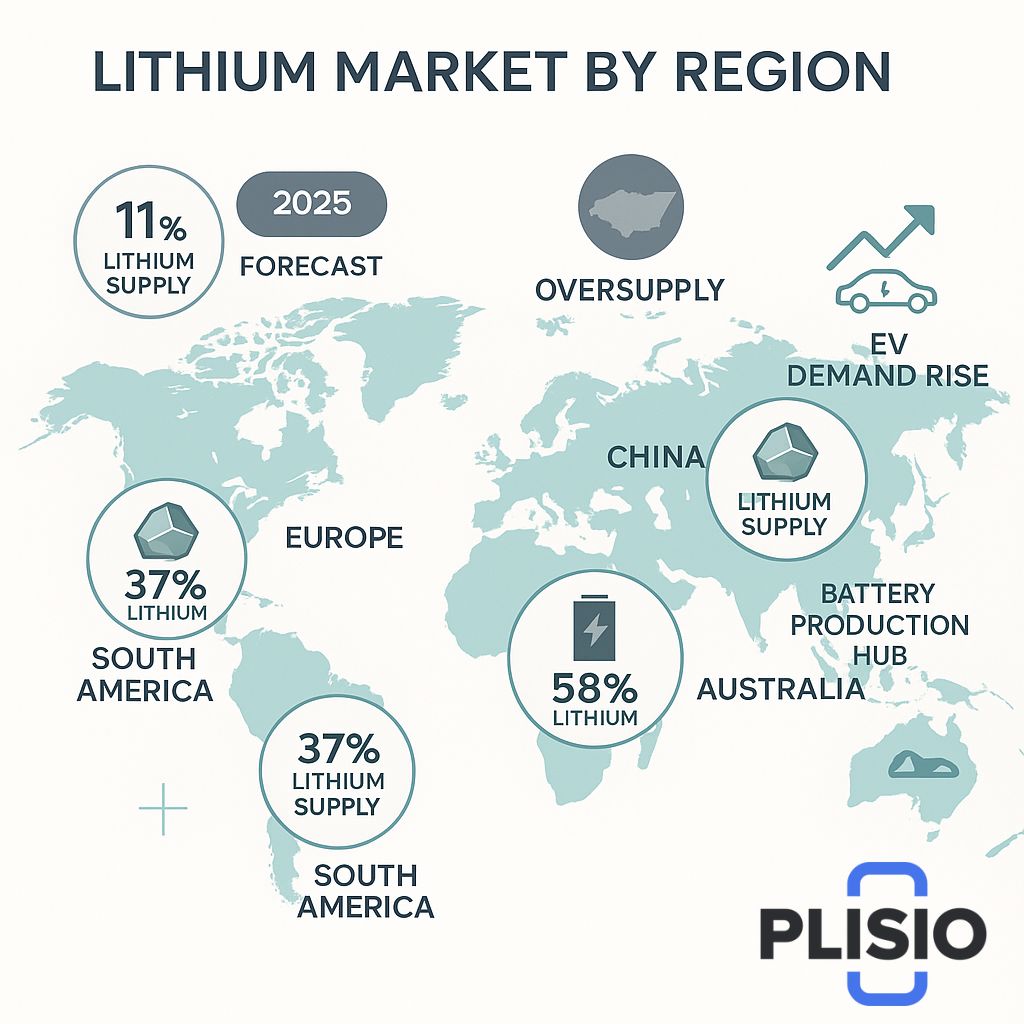

Where lithium stands in late 2025

In 2025, lithium pricing stabilized after historic price spikes and subsequent declines. The price of lithium in battery-grade lithium carbonate hovered near USD 11,600 per metric ton (per metric ton and per metric), while lithium hydroxide traded with narrower spreads. The lithium market means fluctuating norms rather than long-term tranquility, and despite oversupply phases, demand for the battery remains consistently elevated.

Battery supply chain adjustments, delayed lithium project expansions and improved recycling capacity slightly balanced supply and demand, though lithium supply overhang stems from accelerated mine expansions of 2021–2024. Lithium supply chain diversity is a core industrial goal as Western economies work to reduce reliance on Chinese lithium refining and rival emerging refining hubs.

Key Drivers: Demand, Supply & Lithium Supply Chain Shifts

Some of the forces shaping the lithium market are structural:

- demand for lithium driven by electric vehicle and energy storage build-out

- lithium supply expansion tied to mining access, regulatory approvals and capital intensity

- undercurrent for the lithium market from policy incentives and national security framing

- reliance on Chinese lithium refining and rival development of lithium source in the Western hemisphere

The largest undercurrent for the lithium market remains balancing lithium supply with lithium demand. Lithium market is excessive supply in the near term, but EV demand expected to accelerate beyond 2030 and beyond 2030 and new supply projects could rebalance price outlook frameworks.

Recent Data 2024–2025

|

Segment |

Value / Status |

|

battery-grade lithium carbonate |

~ USD 11,600 per tonne |

|

lithium carbonate futures |

moderately volatile but stable in Q4 2025 |

|

lithium carbonate prices rebound |

driven by infrastructure energy storage orders |

|

lithium Amercias & Ganfeng lithium |

continue to expand production capacity |

|

per cent of global lithium capacity |

now concentrated in refining nations |

2024 and are projected to transition into gradual tightening by 2026 as lithium suppliers reassess cost, battery supply and recycling integration.

Forecast & Price Outlook 2026–2030

Lithium price forecast modeling shows multiple variables:

- lithium could reach USD 14,000–17,000 per tonne in 2026 (per tonne in 2026) if EV demand and grid energy storage investments scale

- price spikes remain possible from activity that can catalyse short-term price movements and push volatility

- new mining entrants could become the largest lithium source and lithium source in the western markets

Long-term lithium predictions emphasize least 2030 before true supply equilibrium. Strong electrification policies fueled strong long-term lithium growth as EV demand expected to accelerate, battery supply scales and supply chain localization reduces reliance on Chinese lithium refining.

Battery, EV and Electric Vehicle Dynamics

EV sales may hit 20 million units in 2025, confirming demand for the battery core metals. Demand for lithium is reinforced by battery technologies, energy storage and hybrid powertrains. EV demand expected to accelerate beyond 2030 and new storage formats maintain upward pressure.

Key battery trends include:

- high-nickel cathode revival

- sodium-lithium hybrid architectures

- improved fast-charge retention materials

The battery supply chain and lithium supply chain must handle both recycling scale-up and raw materials replenishment. Raw materials scarcity no longer defines lithium alone but rather processing, conversion and refining throughput.

Mining & Global Supply Dynamics

Lithium producers are shifting investment to reduce reliance on Chinese lithium refining and rival capacity. Mining nations in Latin America aim to become the world’s largest lithium basin and potentially the world’s largest lithium refining ecosystem.

Lithium refining and rival major expansions are strategic. Western states want to reduce reliance on Chinese lithium, domestic permitting aims to accelerate beyond 2030 and new processing hubs are expected to emerge.

Lithium Growth vs Supply Pressure (2024–2030)

|

Year |

Demand Growth |

Supply Expansion |

Notable Shift |

|

2024 |

12 per cent annually |

rapid oversupply |

inventory absorption |

|

2026 |

mid-cycle tightening |

slower approvals |

mining consolidation |

|

2030 |

demand expected |

beyond 2030 and new supply |

recycling dominance |

Market Volatility and Price Movement

Short-term activity can catalyse short-term price movements, pushing prices above equilibrium when investors anticipate deficits or government stockpiling. Price instability in the near regime persists amid geopolitical pressure, lithium supply expansion and energy storage growth.

Long-Term Stability & Industry Transformation

The lithium industry has maintained expansion discipline to avoid uncontrolled oversupply. Metals strategy suggests lithium prices may stabilize as recycling output offsets fresh mining.

Lithium market update sentiment remains optimistic. Lithium prices remain under pressure but sentiment suggests post-2026 normalization.

Conclusion & Lithium Investment Reflection

Lithium stocks show cyclical recovery patterns, while lithium Americas and Ganfeng lithium exercise project discipline for extraction and lithium carbonate and lithium hydroxide balancing.

Supply and demand convergence is the next defining feature. Demand for the battery remains strong. Lithium project maturity improves investment timelines. The global shift to electric vehicle manufacturing remains non-negotiable.

The future suggests:

- lithium prices remain under pressure near-term

- strong long-term stabilization

- world’s largest lithium ambitions will shift Western power

Price outlook consensus: lithium a strategic resource that commands attention and structure. Investors should observe lithium carbonate trading, lithium carbonate equivalent projections and per cent of global consumption alignments.